Liubomyr Vorona/iStock via Getty Images

Despite the recent rebound, equities had been hammered in 2022. The S&P is still down nearly 10%, with the tech-heavy NASDAQ still down over 16%. Workiva (NYSE:WK) hasn't been exempt from the carnage. The stock has fallen dramatically from its 52-week highs, as it's currently down over 40% year-to-date. Workiva did deliver some good news in their second quarter results as revenue figures topped estimates and the number of large contract customers increased. New XBRL requirements and possible requirements in the future could continue to drive future growth for the company. Let's dig deeper into the Q2 results and find out if continued growth can be expected.

XBRL Usage

In prior articles, I have mentioned the various situations in which additional XBRL usages may come into play such as environmental, social, and government (ESG) investment practices, cybersecurity, insider training and SPACs.

The SEC has recently provided guidance on a new iXBRL requirement, the tagging of Form 11-K documents. Form 11-K filings contain information about an entity's employee stock purchase, savings, and other similar plans (A 401K plan is a common example). Filers of 11-K forms will have a three-year transition period after the effective date of the amendments to comply with the Inline XBRL requirements.

Also, early in the summer, the Financial Transparency Act (FTA) was introduced in the Senate. This goal of this bill is to have the eight regulatory agencies of the U.S. Financial Oversight Council (FSOC) adopt and apply uniform data standards for information collected from regulated entities. These eight regulatory agencies would include: the Securities and Exchange Commission (SEC), the Federal Deposit Insurance Corporation (FDIC), the Office of the Comptroller of the Currency (OCC), the Consumer Financial Protection Bureau (CFPB), the Federal Reserve, the Federal Housing Finance Agency, the National Credit Union Administration (NCUA), and the Commodity Futures Trading Commission (CFTC).

Given the more pressing Senate items such as inflation, healthcare, and climate change, to name a few, I don't foresee the Senate moving on the FTA anytime soon. However, the possibility of the FTA becoming a reality would certainly benefit XBRL providers.

As stated on the conference call by management, likely ESG reporting will likely be the next significant driver of long-term growth for XBRL providers.

Now, I'd like to further discuss the status of XBRL quality for Workiva, Toppan Merrill and DFIN and the industry as a whole.

XBRL Quality

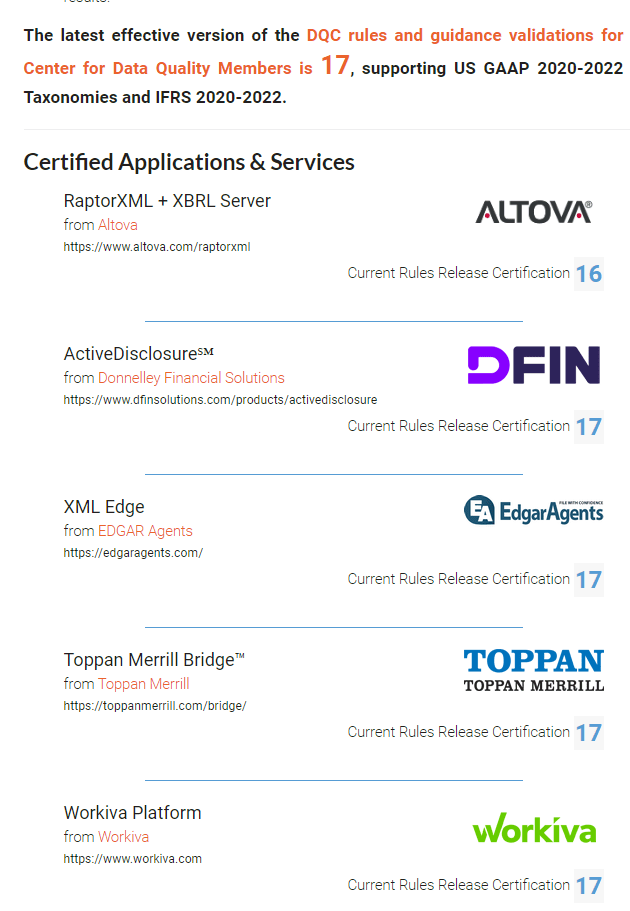

For this article, I'm not going to do a deep dive into the origins of XBRL (extensible Business Reporting Language) or the current process for creating new XBRL data quality rules. That information can be found in a few of my prior articles. Additionally, for the reasons mentioned in those past articles, despite the various XBRL providers, I focus on the companies I view as the industry leaders, Workiva, Donnelley Financial Solutions (DFIN) and Toppan Merrill (private company). Since my last article, no additional XBRL rules have been added and DFIN, Workiva, and Toppan Merrill continue to support the last XBRL ruleset, ruleset 17.

XBRL US website

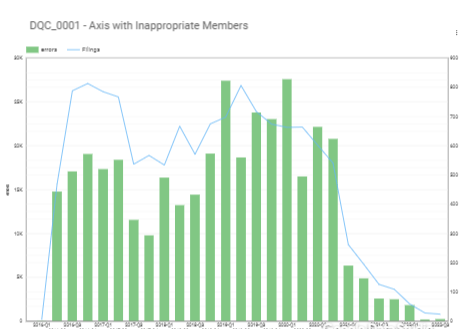

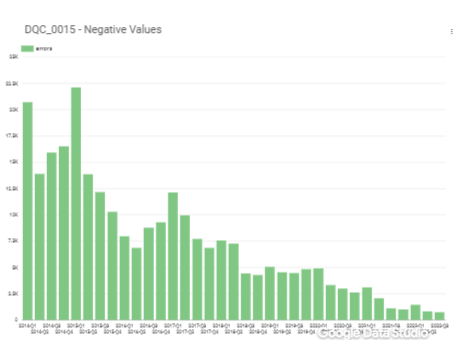

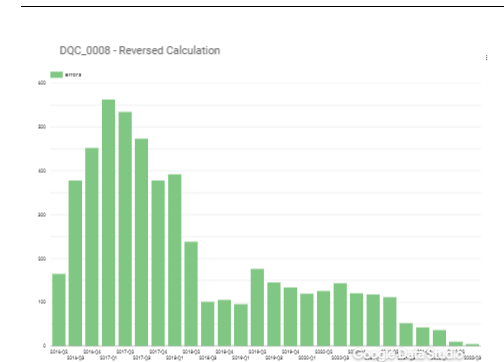

Now looking at the XBRL data quality results as a whole, the results of Q2 2022 were stellar. As the line graph excellently shows in the "Axis with Inappropriate Member" graph below, the number of filings with issues is substantially dropping. From my observations, most of the rules saw a decrease in the number of filings with errors from Q1 2022 to Q2 2022. Also, as noted previously the yearly trend is very positive, as the number of filings with errors has declined compared to prior years. I think the "Negative Values" graph is a good indication as the number of filings with errors has gone steadily downward over time. For XBRL providers and the data consumers, this is wonderful news as it shows the number of errors is decreasing which makes the data easier to consume and compare.

Axis with Inappropriate Members

XBRL US website

XBRL US website

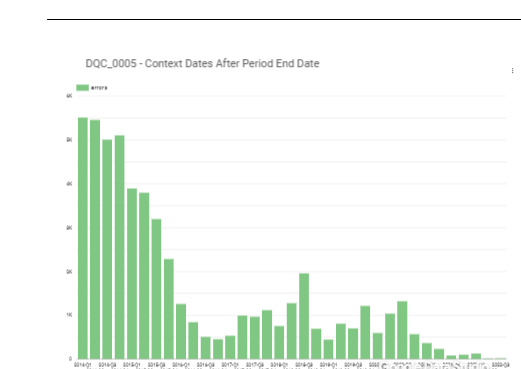

Context Dates After Period End Date

XBRL US website

XBRL US website

Over the past several quarters, I've been following the XBRL data quality results for several large companies. Toppan Merrill has consistently had the best quality among the three companies. However, both Workiva and DFIN had better results in Q2 compared to Q1 2022 filings. Let's hope this trend continues. The below provides additional information regarding the various large companies I have been following and their corresponding XBRL results.

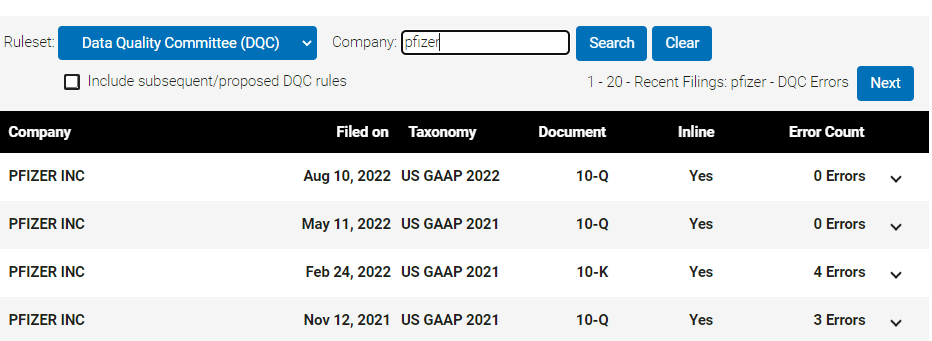

Pfizer (PFE)

Workiva has been providing the XBRL services for this company and you can see the following results from the XBRL US website:

XBRL US website

As you can see there were no issues present this quarter either.

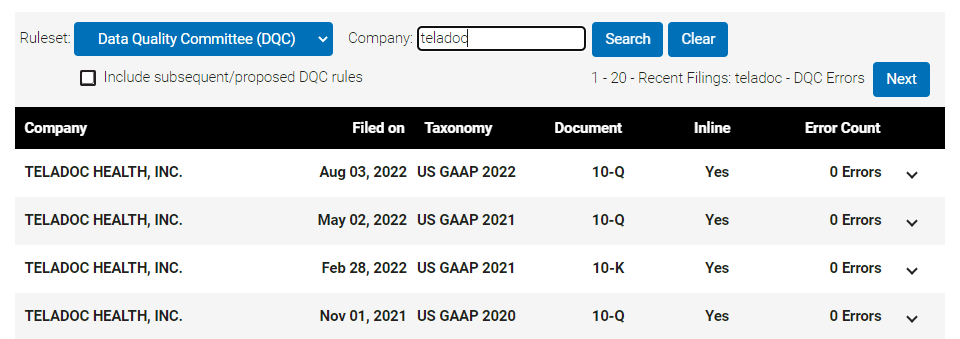

Similar to last quarter, I was unable to find any issues with Toppan Merrill filings. For example, here is one of their company's filing results:

Teladoc (TDOC)

Toppan Merrill has been providing the XBRL services for this company and you can see the following results from the XBRL US website:

XBRL US website

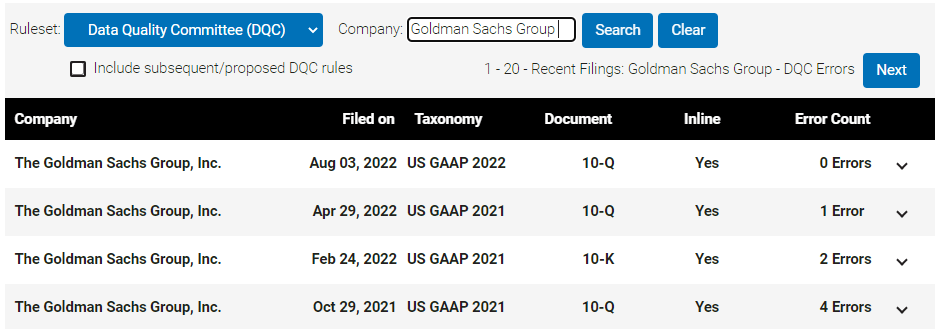

This quarter I did not see an issue with my reviewed DFIN filings. As an example, Goldman Sachs corrected their issues from the prior quarters.

Goldman Sachs Group (GS)

DFIN has been providing the XBRL services for this company and you can see the following results from the XBRL US website:

XBRL US website

This is perhaps the best quarter I have seen when it comes to XBRL data quality. It is very encouraging to see that the XBRL rules are working and that more companies are taking their XBRL seriously.

Financials

Despite the macroeconomic and global headwinds, Workiva delivered respectable results in Q2 2022. The company generated revenue of roughly $131 million in Q2 2022 which is an increase of nearly 24% compared to Q2 2021. Most of this revenue was generated from subscription and support revenue and revenue from professional services accounted for the rest. Subscription and support revenue was roughly $113 million, an increase of 24% compared to prior year's second quarter. New accounts and new solutions helped drive this growth. Professional services revenue was roughly $18 million for the quarter, an increase of 27% compared to prior-year second quarter. This was due to higher XBRL services revenue.

Additionally, the management team provided some updates on ParsePort, which Workiva acquired back in April of 2022. Workiva acquired 850 ESEF customers from the acquisition and ParsePort brought in $1.7 million in revenue for the quarter.

Management also noted that larger contracts have continued to grow. Workiva had 1,186 contracts valued over $100,000 per year, which is an increase of 25% compared to Q2 of 2021. The number of contracts valued at over $150,000 per year totaled 642, which is up 20% compared to the prior year. The number of contracts valued at over $300,000 per year totaled 194, which is up 22% compared to Q2 2021.

Retention remains outstanding as well, as the subscription and service revenue retention rate was roughly 98% for the quarter, which is up slightly from 96% compared to prior year's second quarter rate.

Client count continues to rise as well as Workiva finished Q2 2022 with 4,531 clients, a net increase of 582 compared to Q1 2021. Including ParsePort, the company gained a net 973 customers in Q2 which brings the total customer count to 5,381.

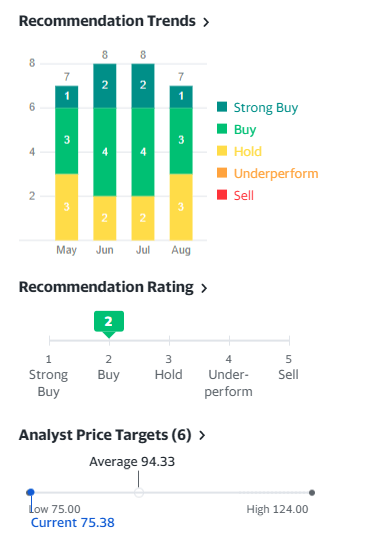

Valuation

Workiva still has yet to achieve profitability. Over the last three months, Workiva's stock price has increased by over 15% however, the company's stock is down significant year-to-date, and the price stock is much closer to its 52-week lows. Most analysts view Workiva either as a "Buy" or a "Hold" but none currently have a "Sell" rating. Also, based on many analysts' projections, the current stock price is well below analyst price targets. I don't predict a quick recovery for this stock given the current macroeconomic conditions, however, investors with a long-term time horizon may view this a good opportunity to accumulate shares.

Yahoo Finance

Conclusion

In my opinion, XBRL usage will only continue to expand over the next several years. The Form 11-K requirement will bring additional revenue to XBRL providers, and I continue to believe ESG reporting will be coming shortly. I don't believe this is an easy market for a competitor to enter, especially given the current economic and global climate. Considering Workiva's leadership position amongst this group I believe they will be an advantageous position to continue to grow revenue and perhaps market share as well.

Despite the rebound in the stock market, I'm inclined to believe the worst is not yet over. I think perhaps later this year, the market will go lower and give long-term investors an opportunity to purchase shares close to the 52-week low. However, I'm still bullish on the industry as a whole and believe XBRL usage will only continue to grow, both domestically and internationally.