Michael Vi

Insider transactions are an important and potentially deciding factor for investors deciding whether to buy or sell a particular stock.

Executives who purchase their company's stock are seen as showing confidence in their company's prospects and valuation, whereas executives who sell stock can send negative signals to market observers.

Palantir Technologies Inc. (NYSE:PLTR) is one example. The company reported stock sales made by its CEO, Alexander Karp, at a time when the stock is struggling to break out of its down channel and is on the verge of falling to new 52-week lows.

With Palantir's business growth slowing and a key insider selling, investors may wonder why they should buy Palantir stock.

Insiders Are Still Selling - Why Are Retail Investors Buying?

Insider transaction trackers and Form 4 securities filings are useful tools for determining how company insiders truly feel about the direction of the business to which they have been entrusted.

Palantir's CEO Alexander Karp sold 1.62 million Palantir Class A shares in two transactions on Tuesday, December 6th and Wednesday, December 7th, according to a recent Form 4 filing available on Palantir's website.

Alexander Karp received $11.44 million in proceeds from the Class A stock sales this week. As shown in the transaction overview from Yahoo Finance below, Alexander Karp has consistently sold Palantir stock over the last year.

While the majority of transactions were completed at significantly higher prices than the previous two, the transaction record shows that Palantir's CEO has been a net seller of Palantir's stock.

With Alexander Karp executing his most recent trades at prices ranging from $7.00 to $7.13 per Class A stock, the question of why retail investors should be buying Palantir arises, especially given that the company is racking up loss after loss (due in part to sky-high stock-based compensation ("SBC") expenses) and has done so consistently over its 20-year operating history.

Insider And Restricted Shareholder Transactions (Yahoo Finance)

Palantir's Business Is Challenged

There are a few issues with Palantir's business that are related to the commercial slowdown. Palantir's commercial growth slowed from 46% in 2Q-22 to 17% in 3Q-22, and a continued slowdown in 2023 could pose a significant problem for the company's overvalued valuation.

Furthermore, Palantir's SBC expenses continue to be a major business and perception issue for the company, particularly because losses average around $100 million per quarter, and profitability has improved very little in the last year.

Why Pay A Premium?

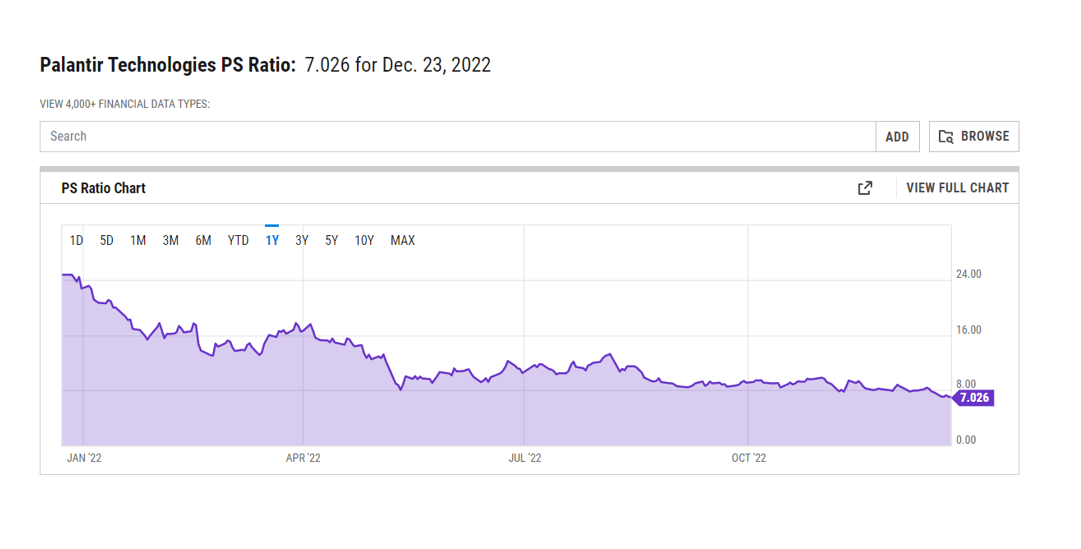

I've been wondering for a while why retail investors are willing to pay 7x sales for a company that helps its insiders get rich while producing no profits for shareholders.

The answer likely lies in the fact that many investors have heard wild and exaggerated stories about Palantir's potential for (commercial) sales growth as well as the potential for multiple expansion, considering that the company is active in a glamorous field such as "software analytics."

As I stated in "Palantir: Don't Get Fooled Again," Palantir has an accumulated deficit of $5.89 billion (as of September 30, 2022), indicating that the company has a frightening history of not earning profits for shareholders.

Despite a history of operating losses, a massive accumulated account deficit, slowing sales growth (Palantir lowered its sales growth target from 30% to 23% in August 2022), and the presence of a CEO who has been busy selling his shares while (retail) investors have been buying, Palantir is selling at an unjustifiably high sales multiple.

PS Ratio (YCharts)

Why Palantir Could See A Higher Valuation

Taking a negative stance on a company like Palantir puts me at risk of missing out on an upside rally. However, given my serious concerns about Palantir's business model, slowing sales growth, inflated SBC expenses, and now stock sales, I believe the risk of missing out on a (year-end) rally is low.

Palantir's valuation could rise if the company signs lucrative contracts with the U.S. government or decides to reduce its SBC expenses.

My Conclusion

The least investors should expect from Palantir Technologies Inc. is that management not sell Palantir stock after investor confidence in the company's growth prospects has plummeted by 65%.

Psychologically, I believe that the recent insider sales are very bad. It is never a good look when the CEO sells a company's stock in a company he is paid to run, especially when the company has failed to make a profit for such a long time.

Nonetheless, retail investors can take away a valuable lesson from this: don't invest in a company whose CEO is selling stock. In other words, avoid being Karped.