Avid Photographer. Travel the world to capture moments and beautiful photos. Sony Alpha User

Investment Thesis

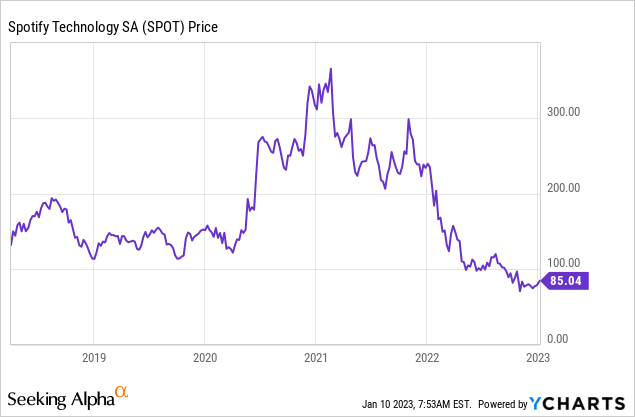

Spotify (NYSE:SPOT) was founded by Daniel Ek back in 2006. While Netflix pioneered the video streaming wave, Spotify made music streaming popular. It is now the world's most prominent music streaming company, with over 433 million users across 183 markets. Due to the broad market sell-off, the company's share price has been dropping significantly. It is currently down over 76% from its all-time high and 42% below its IPO price in 2018.

However, unlike its share price, the company has evolved a lot in the last few years and I believe it is now stronger than ever. It is transforming from a pure music company to an audio company, which will open up a lot of opportunities for growth. The company is seeing strong catalysts from podcasts, audiobooks, and its ad business. It is also one of the stickiest subscriptions product on the market. However, there may be some execution and integration risks as the company did a bunch of acquisitions in the past year. Valuation also isn't cheap despite seeing such a sharp drawdown, therefore I rate the company as a hold at the current price.

Huge Growth Opportunities

Spotify is transforming from a pure music company to an audio company and I believe this is pivotal as it opens up a lot more growth opportunities outside of the existing music business. The aggressive expansion into podcasts and audiobooks makes a lot of sense as the company is able to leverage its large existing customer base and distribution channels to scale and improve ARPU easily. It is able to diversify its revenue streams from subscriptions and further monetize from ads and one-off sales. This should also further increase the platform's appeal and stickiness to customers.

Podcasts have been seeing huge success, but it is still in its early innings in my opinion. According to Spotify, the number of podcasts on the platform was 185,000 in 2018 and grew exponentially to 4 million+ in 2022. The US annual ad spend on podcasts also increased significantly from $497 million in 2018 to $2.1 billion last year, and is forecasted to hit $4.2 billion in 2024. According to Grand View Research, the current TAM (total addressable market) for podcasts is around $14.3 billion, and it is forecasted to grow to $94.9 billion in 2028, representing a CAGR (compounded annual growth rate) of 31.1%.

Spotify

As for audiobooks, the TAM is currently $5.4 billion and is forecasted to grow to $35 billion in 2030 with a CAGR of 26.4%, according to Grand View Research. Audiobooks continue to gain popularity as it has unmatched convenience for consumers, while authors are also able to publish their work easier with much lower costs. Spotify made significant progress in the space through the acquisition of Findaway, a digital audiobook distributor, which allows authors to easily create and sell their work.

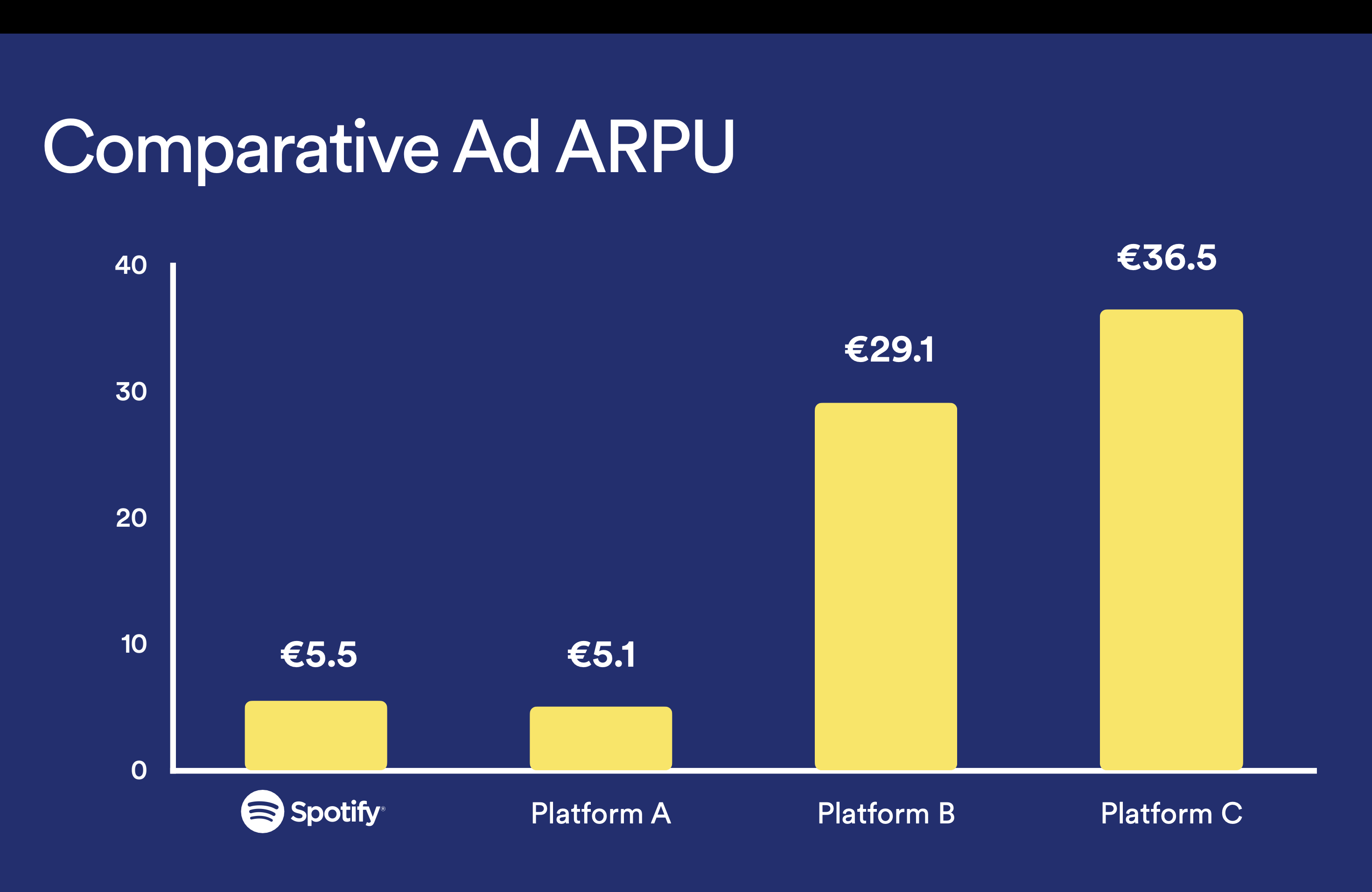

The company has also yet to fully monetize from its new verticals as they continue to make improvements to its ad monetization. For instance, their current advertising ARPU is around €5.5 compared to €36.5 from another platform. It is actively re-inventing the ad experience for both publishers and listeners through a better ad network and audience targeting, and I believe ARPU should see a meaningful increase in the next few years.

Spotify

Strong Stickiness

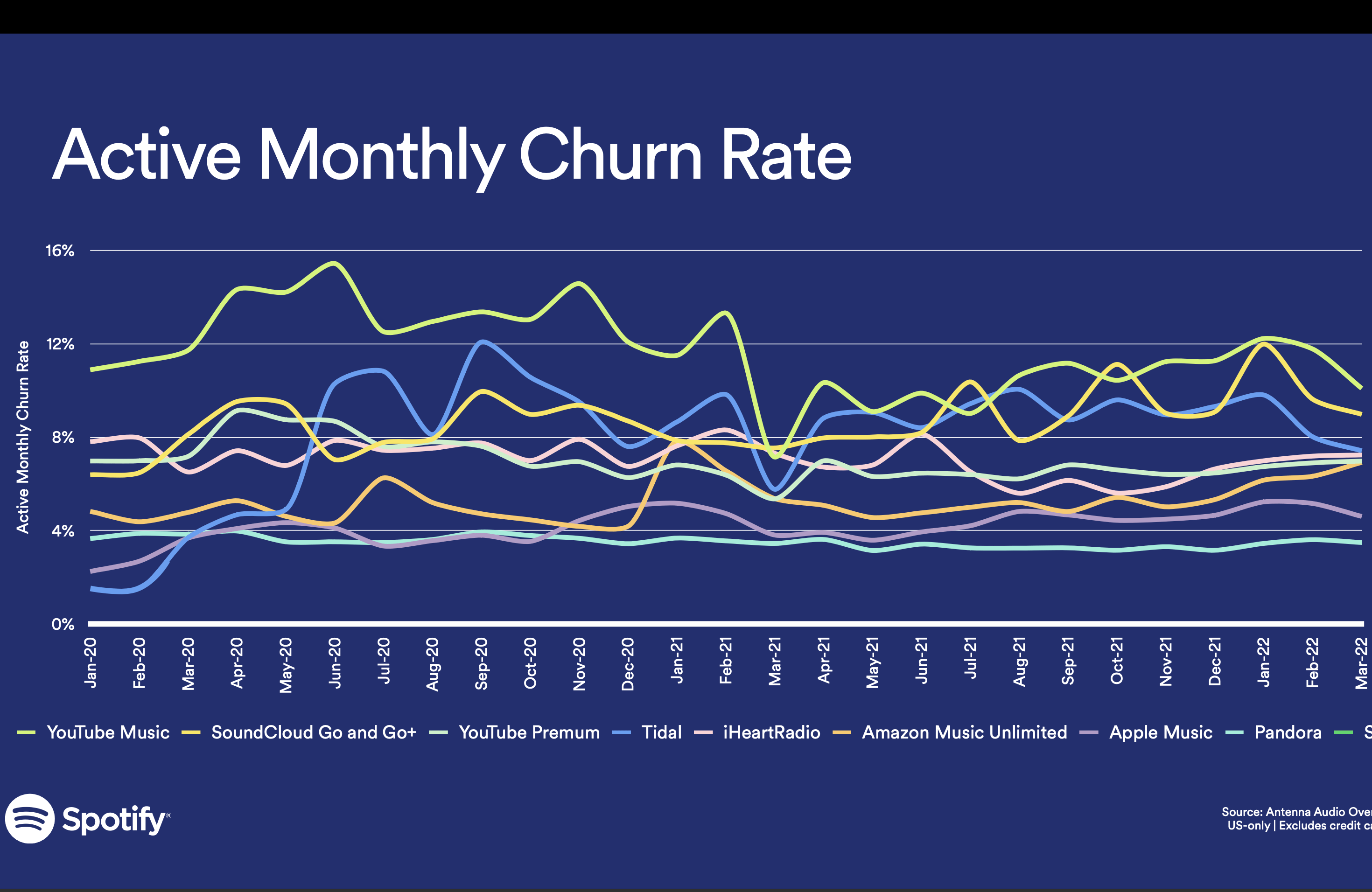

I believe stickiness is one of the most important virtues of a business as it significantly affects the company's pricing power and ability to handle weaker economic environments. While the streaming space is pretty crowded, Spotify is one of, if not the most sticky subscription products out there currently in my opinion. Many would rather cut their Netflix or Disney subscriptions before they cut Spotify. This results in them having one of the lowest churn rates in the industry. According to the management team, the churn rate for established markets in 2021 was 2.4%, down from 3.6% in 2018. From the chart below, you can see that a close competitor like Apple Music has a churn rate of 4%+, while the average is around 8% which is significantly higher than Spotify. This strong customer loyalty gives Spotify significant operating leverage in the long run through pricing power and should increase the company's margins over time.

Spotify

Final Thoughts

While I do like Spotify's prospects and growth opportunities, I do not think now is the time to buy yet. This is largely due to the near-term risks surrounding acquisition integrations, currency, and valuation.

I think execution and integration are currently the biggest risks. Throughout the past two years, the company has made a ton of acquisitions, such as Podz, Findaway, Podsights, and Chartable. It is also expanding its presence rapidly from music to essentially every audio medium. I certainly like the ambition, but I believe it will be very complex to integrate all these companies together perfectly due to lapsing sales & technician teams, different product structures, UX consistency, etc. Besides, music, podcasts, and audiobooks all have different product natures. How these segments come together coherently for users will also be very challenging.

Currency is another potential risk moving forward. Spotify is Europe-based, therefore, it is very exposed to the strong dollar, as it reports earnings in Euros which have been very weak. In the latest earnings, the company took a 9% revenue hit due to unfavorable currency rates (21% as reported vs 12% on constant currency). If the dollar continues to stay elevated, this will likely put further pressure on the company's financials.

Even though Spotify's share price has been falling off a cliff, its valuation remains stretched. It is hard to value the company using traditional metrics such as the PE ratio, as it is still struggling with profitability. On a price-to-FCF basis, the company is currently trading at 81.2x, which is quite expensive. On an EV to EBITDA basis, the ratio is even higher at 103.3x. The valuation should come down quite a bit if Spotify is able to show some operating leverage and improve its margins, but I believe that will take some time as the company is still spending heavily to grow. Therefore, I rate Spotify as a hold and will wait for a better entry price.