metamorworks/iStock via Getty Images

Investment Thesis

Planet Labs PBC (NYSE:PL) designs, produces and deploys constellations of satellites to provide high-frequency geospatial data to customers globally via an internet platform. Over the last year, the Company's shares have plummeted by about 19%. This can be a result of the share dilution witnessed in the Company over the last three years; its outstanding shares have grown by 3.6%.

The low profitability of the corporation is also a factor in poor stock performance. Constant losses might be attributed to the Company's high operating costs. This occurs when I expect prices to remain high due to the massive inflations plaguing the global economy.

Notwithstanding these challenges, I have a positive outlook on the Company because its revenue has increased as its client base expands. Also, no debt is on the books, making this a healthy financial position. It has good financial leverage, and its cash runway, based on its cash flows, is currently more than three years long. The Company's future success will be secured as it strengthens its cooperation with Arizona State University to address climate change.

Company Overview

Planet Labs PBC, which used to be called dMY Technology Group, Inc. IV, is a company that offers geospatial solutions and daily satellite images worldwide. The corporation develops, manufactures, and operates the fleet of imaging satellites used for Earth observation, which take and process approximately three million images daily.

The business handles its data catalog and information extraction with an automated, cloud-based platform. Companies, governments, and communities worldwide may use the platform's images, insights, and machine learning to adapt better to an ever-changing environment.

Planet's platform and analytics products include Planet APIs, Planet Apps, Planet Basemaps, Planet Fusion, and Planet Analytics Feeds. To extract satellite imagery, the Company provides mission-critical data, sophisticated insights, and software solutions to customers in the agriculture, forestry, intelligence, education, and finance industries and government organizations.

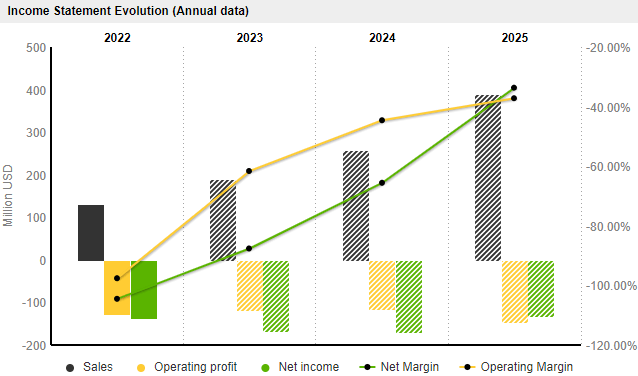

The Company's revenue summary is provided below.

Market Screener

Financials

PL's revenue streak has been quite consistent. Revenues started rising in 2022 and are expected to continue until 2025. According to the Q3 2022 transcript of the Company's earnings call, the increased sales are due to the increasing demand for the Company's products and services and its expanding clientele. As projections show that the Company's revenues will grow through 2025, I am very convinced as the Company is achieving some major milestones to see its revenues grow. For instance, during the third quarter of 2022, they finalized a renewal and expansion contract with a Ministry of Defense customer worth over $10 million over the next 12 months. I believe this will significantly boost their revenues alongside a growing client base.

Will Marshall, "we closed the renewal and expansion contract worth more than $10 million over the next 12 months with an international Ministry of Defense customer."

Market Screener

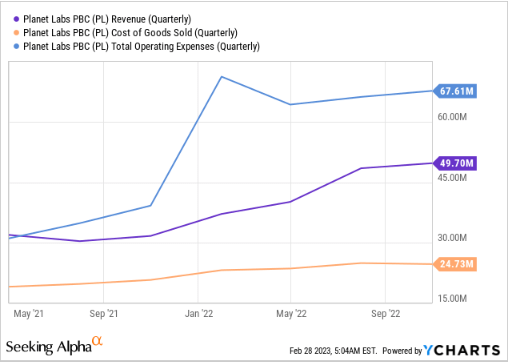

To put the revenue growth in context, sales for the fiscal quarter ending October 31st, FY23, were $49.7m, up 57% year-over-year. In particular, option renewal revenue from a European customer interested in climate and environmental monitoring accounted for $1.5 million of the quarter's upside. The Company is pleased to maintain its commitment to this collaboration, especially with how its global teams have been working together to achieve tangible outcomes for its clients.

Its end-of-period customer count increased to 864, a 16% year-over-year increase that reflects the increasing popularity of its platform. Throughout the past three years, each successive quarter has seen a customer increase at the end of the period. In my perspective, this bodes well for continued revenue growth in the future.

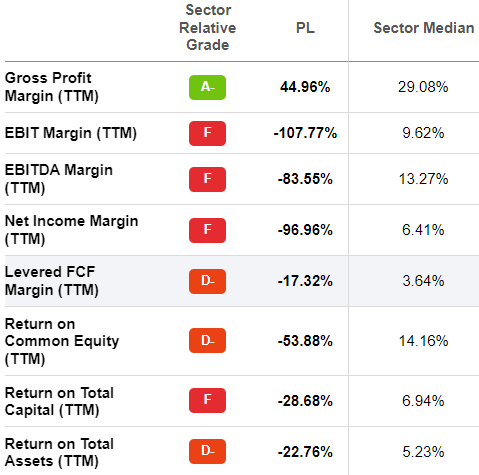

Although its revenues are appealing, PL's profitability is a different story. In absolute and comparative terms, PL profitability is relatively low. The Company's gross profit margin is positive. Still, all of its other vital metrics margins are negative and well below industry medians, indicating uncompetitive in profitability.

Seeking Alpha

I attribute the Company's poor profitability to its high operational expenses. With quarterly sales of about $49.70 million, the Company has total operating costs of approximately $67.61 million, or about 136% of sales. To clarify, out of the $67.61M in total operational costs, $40.01M goes to SG&A costs, about 60% of the total operating expenses. Based on these numbers, the elephant in the room is total operating expenses, specifically SG&A expenses.

YCharts

The high cost of operation can be somewhat attributed to inflation. Still, for long-term success, the Company's leadership must devise a clear strategy for reducing expenses while expanding revenue streams.

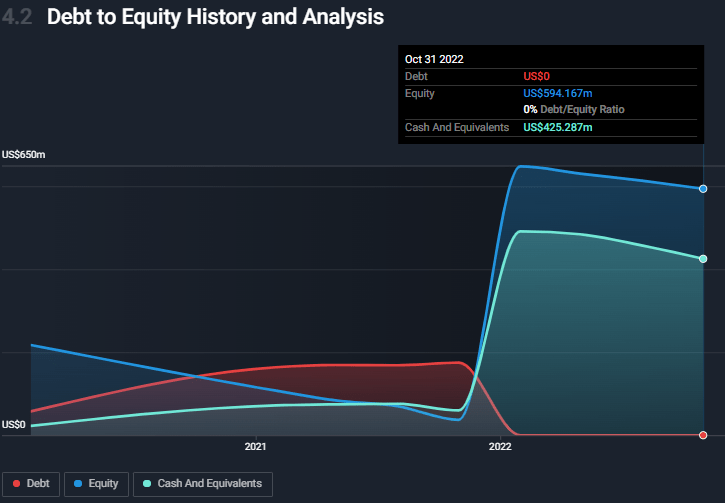

Lastly is the Company's solid balance sheet. As of the third quarter, the Company had no outstanding debt, and its liquidity was pleasing. They had cash and equivalents of about $425M, approximately 72% of its total equity of approximately $594M. The good liquidity is reassuring because the Company has a sufficient cash runway extending for over three years, according to its cash flows.

Wallstreet

Planet and ASU Expand Partnership: A Sustainable Long-term Revenue Generator?

About a week ago, Planet Labs PBC announced that they had agreed with Arizona State University to form a Strategic Partnership. This partnership aims to help people take action on climate change through education and research, workforce development, and an innovation process that puts science first. Through this collaboration, both organizations can focus on their mutual goals of developing and attracting top-tier talent and serving as an impetus for breakthroughs in science, technology, and the responsible application of space to improve the quality of life on Earth.

Why I Think This Collaboration Is Big Business

Today, people all across the world are worried about the effects of climate change. The governments of the world's major economies have spent billions of dollars combating climate change. For instance, in 2022, the United States passed the Inflation Reduction Act to help curb the effects of climate change. In 2022, According to the 2021-2025 World Bank Group Climate Change Action Plan, the Bank Group's new climate finance objective was 35%, which it surpassed in the fiscal year 2022 by lending 36%, or $31.7 billion, to climate-related activities. Based on the agreed upon common Multilateral Development Bank (MDB) approach, the $31.7 billion represents the overall share of finance directly related to climate action across all Bank Group projects—an increase of 19% from the previous fiscal year's record of $26.6 billion.

Statistical evidence like this makes it clear that addressing climate change is becoming increasingly essential, making this initiative to collaborate on the issue all the more persuasive. As a frame of reference, consider that in the third quarter, $1.5 million of the revenue increase came from a European customer who focuses on climate and environmental monitoring. Given these considerations and the growing investment in climate action projects, I am confident these actions will significantly bolster these companies' future profits.

Risks

Despite the company's allure as an investment, it's not without flaws. The company's financial leverage is one of the risks I see in making an investment in the business. Since the firm has no existing debt, it will need to rely on equity financing or cash flows to back its main investment plans.

This makes me concerned that, should the company decide to fund a sizable investment, it might lead to a period of rapid cash burn or possibly more share dilutions. This occurs after the corporation has steadily diluted its stockholders' position over the past three years, by an estimated 3.6%. It is evident from these numbers whether or not the company will likely issue new shares of stock to meet its financial obligations. Potential investors should exercise caution in light of this possibility.

Conclusion

Due to declining profits and increased dilution of shares, PL stock has fallen by around 19% in recent years. Although this may be the case, the Company's top line has been doing exceptionally well, growing 57% year over year in Q3 2022. This was due to the popularity of the business' offerings. Nonetheless, the high cost of conducting business is a huge roadblock to profitability, and the organization must deal with it.

The firm's high liquidity is supported by healthy cash flow, and has no debt on its balance sheet. The corporation has strengthened its collaboration with ASU to adapt more effectively to climate change. I do not doubt that this decision will be crucial in maintaining the present revenue growth rate. Based on this data, I have a positive outlook on PL stock but would recommend holding until profitability improves.