Thomas Bullock

Pool Corp (NASDAQ:POOL) is a great company, but current valuation and a 2023 headwinds keep me on the sidelines for now.

Company Profile

POOL is a wholesale distributor of swimming pool equipment, supplies, and related products. It also distributes landscape and irrigation products as well.

At the end of 2022, it had 420 sales centers in North America, Europe, and Australia. It operates under the Superior, Horizon, SCP, National Pool Tile (NPT), Pinch A Penny, and Sun Wholesale names.

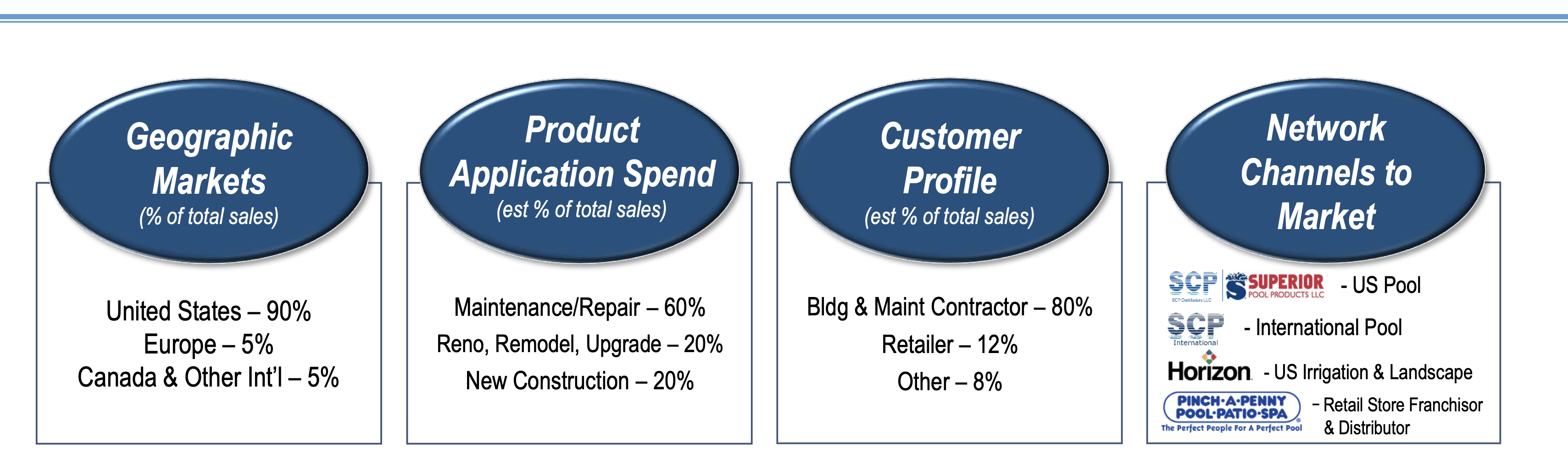

POOL primarily serves the contractor market, with about 80% of its sales going to that customer base. It offers over 200,000 third-party and POOL-branded products, including chemicals, equipment, pool supplies, and replacement parts .

Approximately 90% of its business comes from the U.S. and 96% from North America. California, Texas, Florida and Arizona together accounted for over 50% of its sales in 2022.

The company says that 60% of its sales are related to maintenance and service, 20% from replacement and refurbishment, and 20% from new pool construction.

Company Presentation

Opportunities and Risks

The growth in new pools is both an opportunity and risk for POOL. Every new pool installed helps create a potential new recurring customer for the company. However, new pool installations peaked during the pandemic as more people opted to stay at home, and has since been on a decline. As such, POOL's business associated with new installations does face a headwind.

According to the company, there were 117,000 pool installations in 2021, which declined by -16% to around 98,000 in 2022. POOL expects a further decline in installations in 2023, down another -15% to 20% to approximately 80,000 pools.

Given higher interest rates (as pools often will get financed), the current macro environment, and coming out of a strong demand period because of Covid, the slowdown in new pool installations in not all that surprising.

On its Q4 conference call, CEO Peter Arvan said:

"While the industry was down about 16%, we believe that our new pool construction in units was down somewhere between -12% and -13%. So we think we actually picked up share from that perspective, and that's supported by the growth numbers that we have.

I can tell you that an average pool now is probably in the $70,000 range. But if you pick a different geography, I'll probably give you a different number. And then based on the number of pool builds, as we mentioned, the business in the seasonal markets was much slower than it was in the Sunbelt. So the Sunbelt markets held up much better. So the new pool construction numbers in the Sunbelt are not nearly off as much as they are in the seasonal markets."

The company's base maintenance business had a strong 2022, and sales will benefit from inflation and new pools installed the prior year. However, like many industries, there appears to have been some over-ordering due to previous supply chain issues. At the same time, the weaker macro environment is expected to lead to some deferred repairs and replacements as well. As such, POOL is expected to see a decline in revenue and earnings this year, particularly in the first half.

On the call, CFO Melanie Hart said:

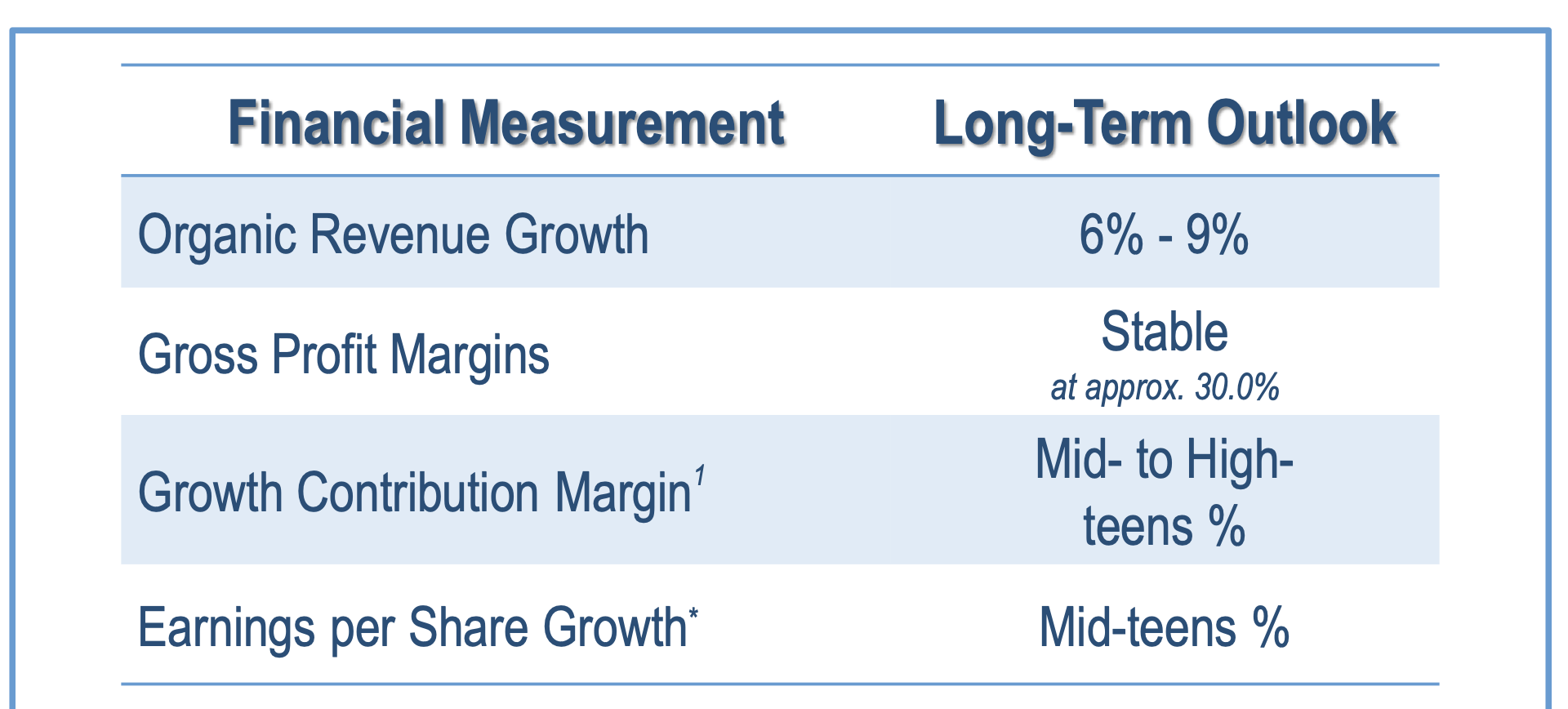

"Comparing expected 2023 sales cadence to 2022, we will have tougher comps at the beginning of the year due to the higher base business growth in 2022. We are likely to see low to mid-single-digit decreases in the first half with greater declines in Q1 and somewhat less in Q2 and then modest growth in the second half of the year. For 2023, there will be 1 less selling day in the third quarter and for the full year compared to 2022. Gross profit margin in 2023 is expected to be in line with our longer-term guidance of around 30% compared to the 31.3% gross margin we reported in 2022. We will realize some benefit on the existing inventory we carry into 2023 during the first half of the year. …

"In view of the potential for flat to slightly lower sales, gross margin compression and inflationary pressures on expenses, we would anticipate operating margin to decline as much as 100 to 150 basis points compared to 2022 full year results. We believe we can achieve a 15% operating margin even under these reduced sales expectations by continuing an intense focus on expense management and the crisp operating execution we have demonstrated consistently over time."

While facing some near-term headwinds, the company does have some trends working in its favor. Newer pools are generally incorporating higher value products such as automation controls, variable speed pumps, and sanitizing systems - all of which is good for the company that distributes these products. Pools are also aging, with POOL saying the average installed base is 22 years old and that only 70% of existing pools have automation. This represents a good upsell opportunity as households look to repair, replace, and modernize their current pools with the latest technology.

Like other distribution companies, POOL is also looking to improve efficiencies and lower its costs to serve its customers through technology. I've talked about this trend when looking at Veritiv (VRTV) and Genuine Parts (GPC). On POOL's end, it has solutions such as POOL360, which allows contractors to place orders, search for parts, and pay their bills online, and BlueStreak, which allows customers to quickly buy bulk chemicals, bleach, and acid with just the scan of a card, never having to come inside the store. It will be launching POOL360 Water Solution later this year.

M&A is another common tool in the distributor toolbox. POOL can pick up local or regional distributors and improve their operators through scale buying power and technology, while taking out costs. These types of acquisitions are generally very accretive with distribution models.

Valuation

POOL stock trades at a 16x EV/EBITDA multiple based on the 2023 EBITDA consensus of $973.6 million. Based off of the 2024 EBITDA consensus of $1.04 billion, it trades at around 15x.

It trades at 21.6x forward EPS, with analysts projecting 2023 EPS of $16.37.

It's projected to see revenue fall -3% in 2023, returning to 4.5% growth in 2024.

Company Presentation

The stock trades at one the highest valuations among its distributor peers.

POOL Valuation Vs Peers (FinBox)

Conclusion

I like distributors, and POOL is a great company. It has a pretty steady pool maintenance business that it feeds into, and its riding some solid longer-term trends such as an aging pool population and more expensive gadgets going into pools.

That said, the company is one of the most expensive distributor stocks out there. It is also dealing with the after-effects of a post-COVID slowdown following a boom in pool demand, as well as a more difficult macro environment. As such, 2023 is more of a re-basing year for the company, with 2024 likely returning to a more normal pre-pandemic environment.

As such, I think the stock is more a "Hold" at this time. At $250, which is under a 12x multiple based on 2024 EBITDA, I become more interested.