Nyaaka Photo/iStock via Getty Images

Dear readers/followers,

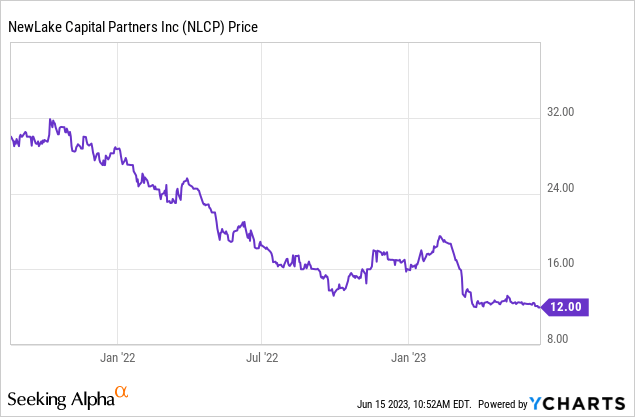

Today I want to have a look at an interesting REIT that doesn't get much coverage - NewLake Capital Partners (OTCQX:NLCP). NLCP is a cannabis REIT which means that it owns properties that are mission critical to the production of cannabis and cannabis products. The company IPOed very recently (in 2021) and the stock price has been on a decline ever since, falling all the way from a high of $32 per share to $12 per share. There were several reasons for this steep decline:

- a broader market and REIT selloff driven by high interest rates

- the IPO price was too "hyped up" and the IPO was poorly timed

- the cannabis industry has fallen out of favor as financing conditions have tightened significantly and margins have declined

- the company made headlines as one of its largest tenants stopped paying rent in 2023

These are all good reasons for the price to fall, but as always the market has a tendency to overreact and I think NLCP might have been a victim of such overreaction, because there's actually a lot to like here as the industry is expected to see double digit growth over the next five years.

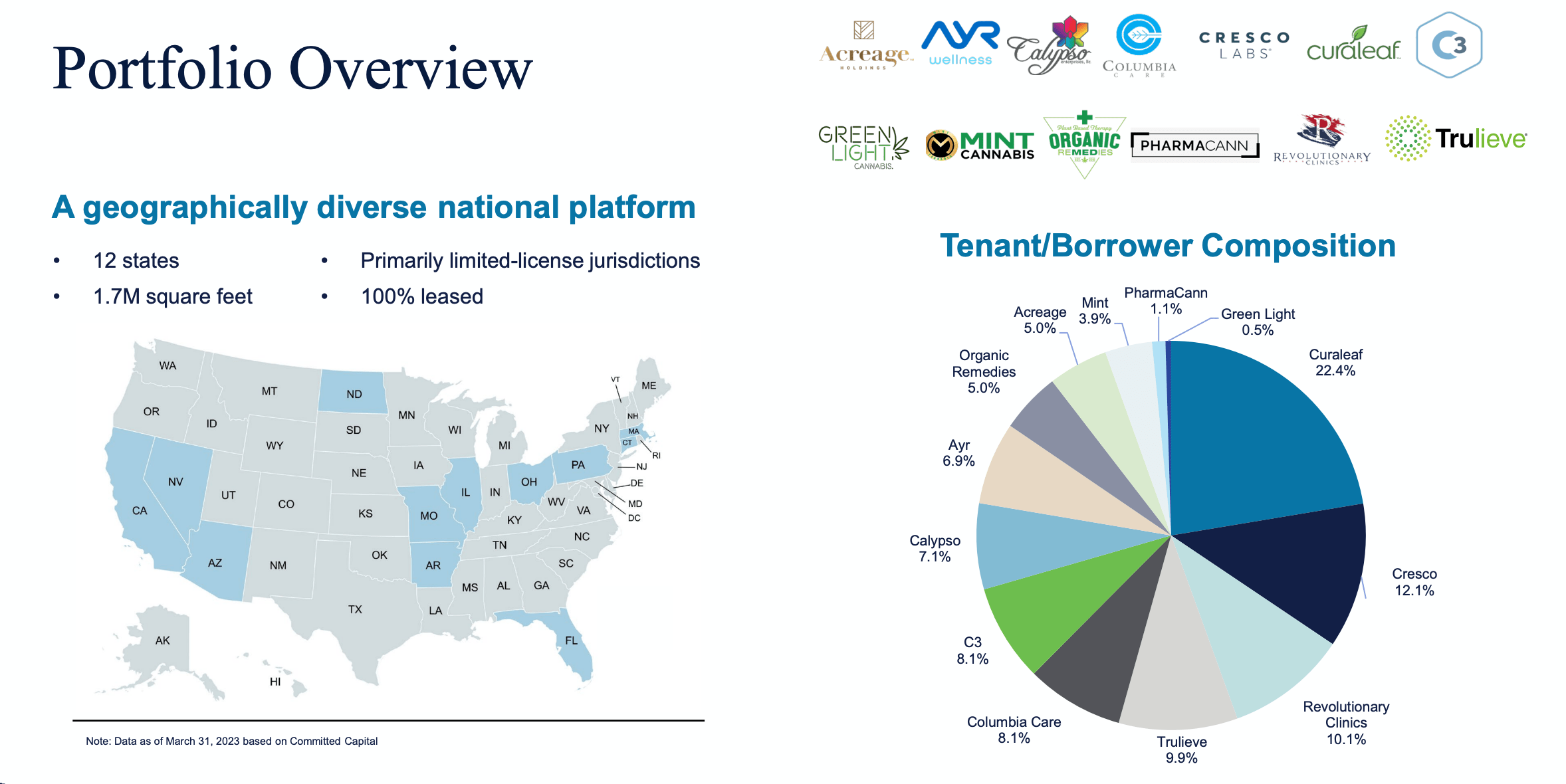

The REIT owns 17 dispensaries and 15 cultivation facilities located across 12 states. It leases these properties to only 13 tenants, which means that the exposure to any one of these tenants is relatively high. Curaleaf (OTCPK:CURLF) being the largest tenant accounts for 22% of all revenues, followed by Cresco (OTCPK:CEJOF) at 12% and Revolutionary Clinics at 10%. Such high tenant concentration can of course be risky (I'll touch on this later), but the good thing is that most of the tenants are large and well established players in the industry as 64% of rent comes from tenants that are publicly traded. Moreover all tenants are state-licensed.

NLCP Presentation

The company maintains a 100% occupancy so the risk here isn't vacancies, but rather rent collections. Indeed, the third largest tenant, Revolutionary Clinics, which accounts for about 10% of revenues, hasn't paid rent in 2023 for their property in Massachusetts. Management has confirmed on the earnings call that in the first quarter 25% of the security deposit ($315,00) has been applied to partially offset the unpaid rent. Although management sees a potential light at the end of the tunnel with Revolutionary Clinics, I am not quite as optimistic and expect the tenant to have to move out eventually. Management expects collections to reach 90-93% in the second quarter, assuming no payment from Revolutionary Clinics and a partial further offset on unpaid rent from the security deposit.

While a tenant default is clearly not great for NewLake as a landlord, it's also not a deal breaker. This is because the landlord is by definition well insulated from the operational struggles of tenants. If a tenant goes bankrupt, the company can easily re-lease the space to another company, especially since these are mission critical assets (or the picks and shovels of the industry as management refers to their properties). I also want to point out that in most states the license is tied directly to the property which gives the landlord a major advantage.

On a portfolio basis, the company recorded a Q1 FFO in line with expectations of $0.44 per share and declared a $0.39 per share dividend. Though the dividend yield stands at a whopping 13%, it remains covered despite mere 90% collections with a payout ratio of 88%. This suggests that the dividend is safe for now, though a dividend cut is certainly possible if the REIT cannot replace Revolutionary Clinics with another tenants, and/or another tenants struggles with their rent payment.

In the meantime, NewLake maintains the best balance sheet amongst all REITs as it has only $2 Million in debt. Along with $89 Million available under their revolving credit facility, this puts them in a great position to (1) absorb any negative shock such as a failure of one its large tenants, and (2) take advantage of low prices and expand their portfolio.

In addition to a very high dividend yield, there's also meaningful upside potential. The stock currently trades under 7x this year's FFO which is significantly below Innovative Industrial Properties (IIPR) which is a close peer and trades at 9.3x. At the $12 share price, the FFO yield stands above 15%, which means that beyond acquisitions the company can also drive value for shareholders via stock buybacks. During the first quarter they did buyback about 50,000 shares (0.2% of float) at an average price of $12.63, but I'd like to see them do more in the following quarters, especially with their high liquidity.

When interest rates stabilize and credit comes back, NewLake's capital partners will likely see their margins expand and will have a much easier time growing. Consequently, I expect the stock to increase to a more reasonable 10% FFO yield, which would imply upside of about 50-60% from here. In the meantime investors will continue to enjoy a dividend which now stands at 13% and continues to be covered even with no collections from the third largest tenants. For all these reasons I rate the stock a BUY here at $12 per share with a price target of $18 per share. If you're after a REIT that pays a dividend in excess of 10%, this is one of the best candidates.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

If you want full access to our Portfolio and all our current Top Picks, feel free to join us at High Yield Landlord for a 2-week free trial

We are the largest and best-rated real estate investor community on Seeking Alpha with 2,500+ members on board and a perfect 5/5 rating from 500+ reviews:

![]()

You won't be charged a penny during the free trial, so you have nothing to lose and everything to gain.

Start Your 2-Week Free Trial Today!