mfto

Written by Sam Kovacs

Introduction

I was initially against writing this article. I told myself "no Sam, you should keep the good stuff for members of your paid service."

The value of what we offer doesn't lie (only) in our stock picks, but in the community, the tech, the model portfolios and timely updates and coverage of our investment universe.

So I decided: To heck with it. Let's give everyone a few of our top 10 picks. Today I'll present two.

As dividend investors, our primary goal is to maximize our long-term income potential. Note that this is different from maximizing income today, which can be achieved with very high yielding stocks. There's a combination of yield and growth, which must lay on a strong foundation of dividend safety, which maximizes income potential.

Future dividend growth is out of our control: It's constrained by any given company's ability to grow, take market share, expand payout ratios, or buy back shares.

On the other hand, the current yield is in our control. We can chose to buy or not to buy.

The two stocks I'm presenting today not only have excellent dividend safety and capital downside protection, they're trading at yields which are really attractive relative to their dividend growth potential.

Our Strategy

Our strategy is a dividend growth investing strategy which can be summarized as:

- Buy low

- Sell high

- Get paid to wait

Sounds simple, but there's a lot that goes into these principles.

Buying low suggests buying at a price which offers a yield which is satisfactory given our assessment of dividend growth potential.

To know what yield is satisfactory for any level of projected dividend growth, we run simulations which make us able to answer the question: Is a 3% yielding stock growing at 8% per year better than a 2% stock growing at 12% per year?

We've formalized this for members of the Dividend Freedom Tribe to make it easy.

We also use our DFT charts to figure out good times to buy and sell stocks.

DFT Charts calculate the minimum, maximum, median yields over the past 10 years (along with the 25th and 75th percentiles), to chart theoretical "fair values" for a stock.

For example in this chart of Pfizer (PFE) which we entered below $36 during the pandemic and exited in late 2021/early 2022.

PFE DFT Chart (Dividend Freedom Tribe)

It's quite clear that as the stock went up following all vaccine excitement, the stock was yielding a lot less than it historically had.

We didn't believe the vaccine numbers would change long term growth rates, and therefore decided to sell. Today PFE is back below its pre-pandemic levels.

The pendulum always swings back from overvaluation to undervaluation.

Of course this is an example which shows success in timing tops and bottoms.

Of course, when we suggest selling we get pushback from shareholders who don't want to accept the reality that their favorite stocks might be overvalued.

For example, in an article in April, I suggested selling Exxon Mobil (XOM). These are the type of comments we got:

Sell XOM... LOL... only sitting on the best offshore field of the past several decades at an ultra low royalty deal...in Guyana...

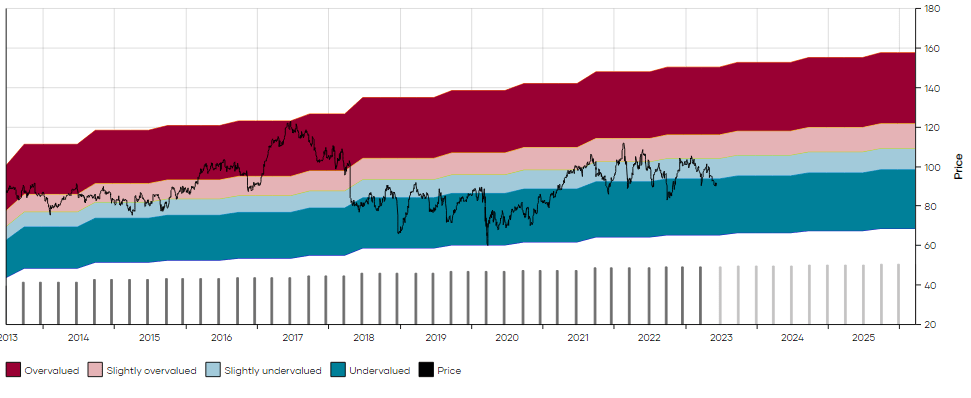

We accumulated our position in XOM in between March and August 2021, at prices between $53 and $58, when it was clearly historically undervalued relative to its dividend, as you can see on the DFT chart below.

XOM DFT Chart (Dividend Freedom Tribe)

We then sold in four increments in between March 2022 and January 2023, at $80, $99, $112 and $110.

We didn't know, and still don't know, how high Exxon will go. All we know is that if we sell high, we can lock in the gains and redeploy them into stocks with better dividend profiles, as measured by the combination of yield and growth rates.

For those wondering, yield on cost is irrelevant here, because it fails to capture opportunity cost.

A simple example. You buy a stock at $100 when it yields 4%. You get $4 of dividends per year.

The stock doubles. It now trades at $200, and yields 2%, but you still get $4 per year.

You can keep your stock, or you can sell and redeploy the funds into another share, which let's say costs $100 and yields 4%.

You now own two shares which are worth a combined $200, and pay out $8 per year.

You've doubled your income.

Yes you might need to factor in tax.

Yes this will change the arithmetic of a replacement yield.

But the principle holds.

If the goal is to maximize long-term dividend income (and as dividend investors, this is a very good goal to have), then selling high makes just as much sense as buying low.

In a nutshell this is our strategy.

Without further ado, let's move on to our two first picks on our Top 10 list.

Pick Number 10: CAG

In April, Conagra (CAG) was the topic of our buy list.

I wrote a note, highlighting its strong results.

The company increased its EPS by 31% on a top line growth of 6%, reflecting a lag between increase in costs due to inflation and their pricing measures.

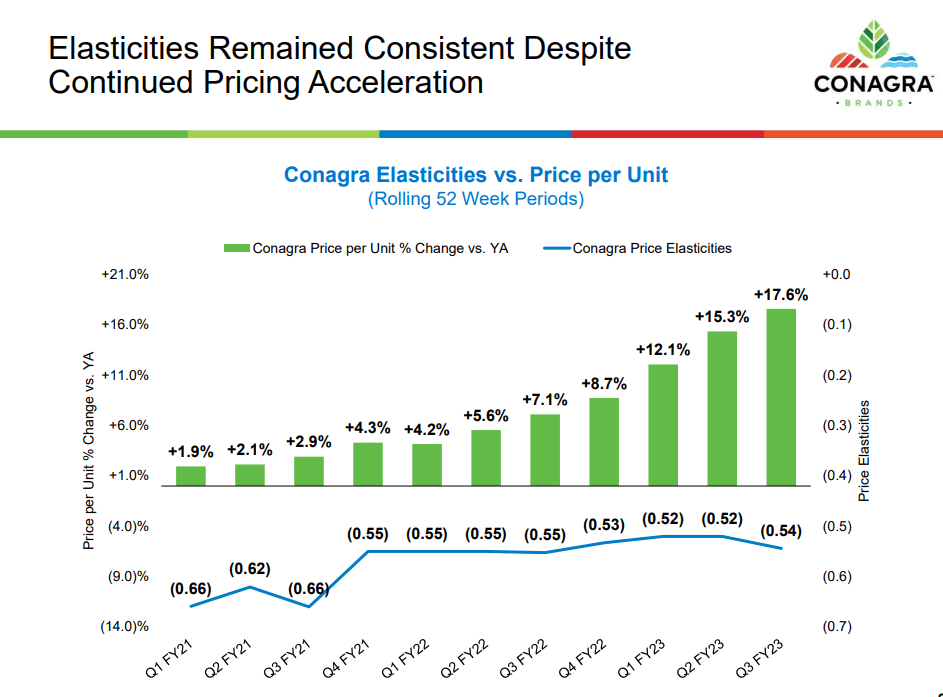

CAG Investor Presentation

The slide above from their earnings presentation shows how the company has aggressively increased its prices, yet seen price elasticities remain near constant.

This reflects some degree of pricing power, which the company justifies as reflecting strong investments in their brands, which consumers are willing to pay more for.

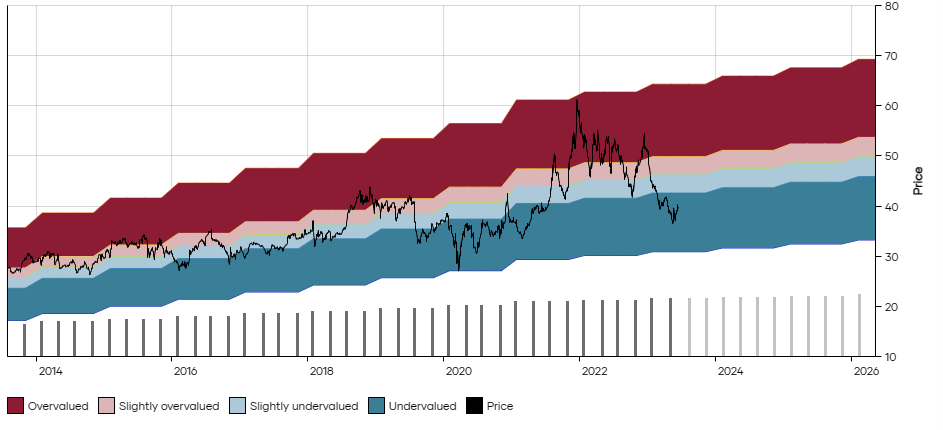

The stock has come down somewhat since April and now trades at $34 and yields 3.8% going forward. The true yield is in fact higher, as CAG will without doubt increase its dividend next quarter too.

CAG DFT Chart (Dividend Freedom Tribe)

Last year the company increased by 5.6%, and over time this is where CAG's dividend growth has converged.

The most likely dividend hike I see is to $0.35 per share per quarter, which would represent a 6% hike from the current level.

This would give the stock an effective 4% yield.

During the past 10 years, CAG has yielded a median 2.8%. If the shares were to return to their historical median yield, they would rise back to $50, which would represent 45% appreciation from current levels.

The dividend is projected to keep going at a healthy 5%-7% growth rate, which is largely sufficient given the stock's yield.

CAG is a much better pick than other names in the consumer staples space.

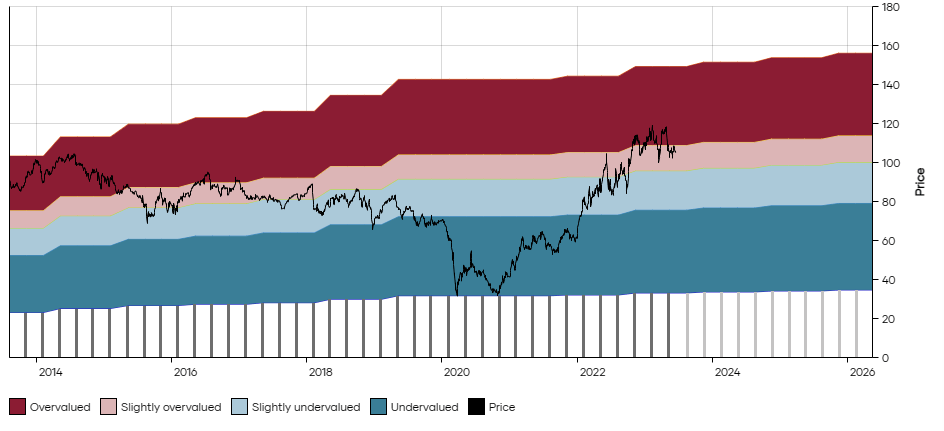

Walmart (WMT) is often brought up as a good defensive dividend growth stock. But when I look at it, it's only two of those things: A stock, certainly, and undoubtedly defensive.

But it barely pays a dividend: 1.45% yield. And that dividend barely grows: Growth has been sub 2% per year for the past decade.

WMT DFT Chart (Dividend Freedom Tribe)

And even if you're a long time investor of WMT, never considered selling, and bought the shares back in the 90s at $17 per share, and are sitting on a capital gain of $140 per share, and would have to pay tax, there would still be a case for selling a portion of your position and allocating it to CAG.

Say you have to pay 30% capital gains tax.

After tax, you'd have $115 left for each share you sold, which was previously paying you $2.28 in dividends per year. You could now buy 3.3 shares of CAG, which would pay $4.35 in annual dividends, which equates to an instant 91% income increase. You'd also be shifting to value, which in the long run protects your capital.

As defensive as a stock is, valuation is still a key factor. Had you bought WMT in 2003 at $56, it would have taken you 10 years before seeing substantial gains.

Why not sell when it's overvalued and come back at a later date when the market offers a better price?

In the meantime, we believe that CAG remains a really good play in the consumer staples space as it has been gaining market share, got good momentum from its brands, and trades at levels which are historically well below where they have been.

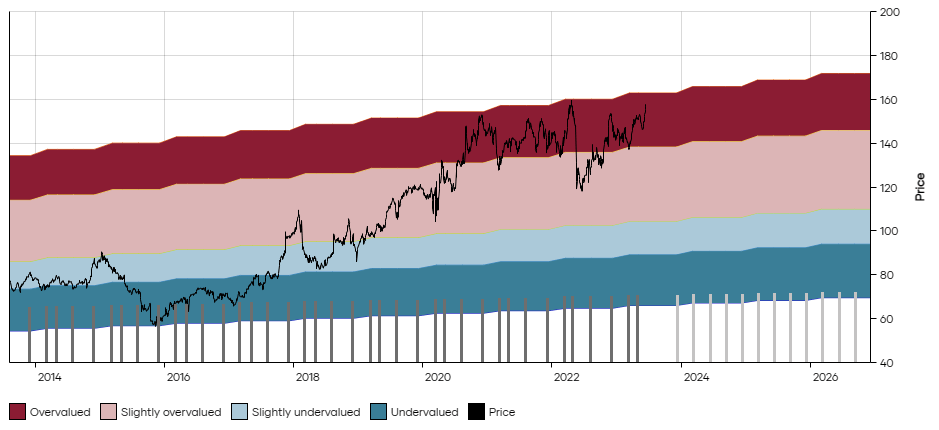

Pick Number 9: PM

The market has not shown Philip Morris (PM) any love since 2017.

This makes no sense to me, as PM has a lot going for it:

- It's the clear leader among tobacco stocks in transitioning to smokeless nicotine products (IQOS, ecigs, etc).

- It has access to many growth markets for cigarettes, which will continue to grow before large spread awareness of health issues comes forth.

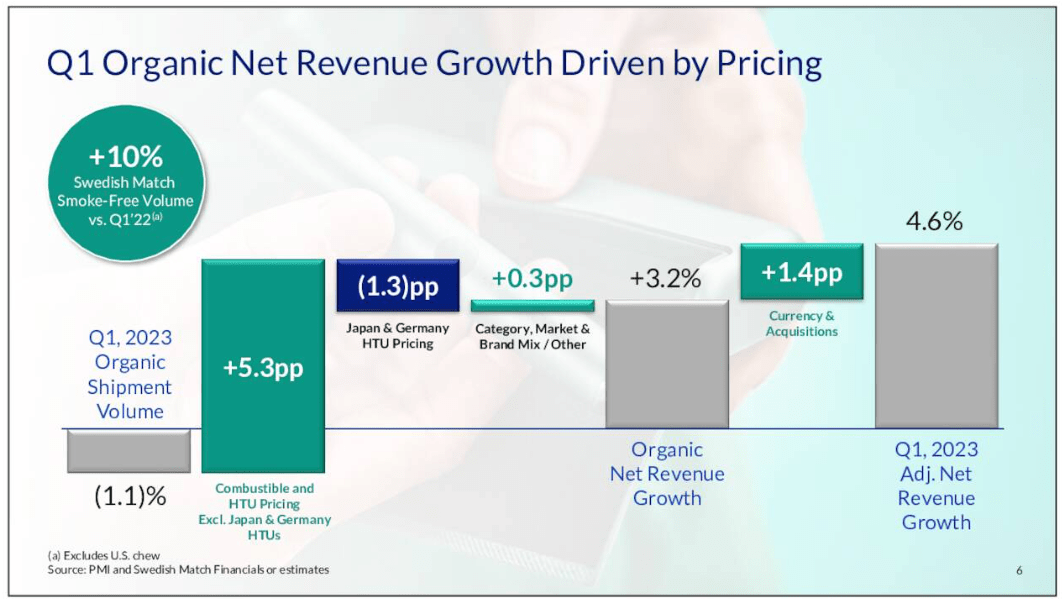

In the first quarter, PM generated 4.6% adjusted revenue growth, with its smokeless segment now representing 35% of overall revenue, and passing the 50% threshold in many key markets.

Dividend Freedom Tribe

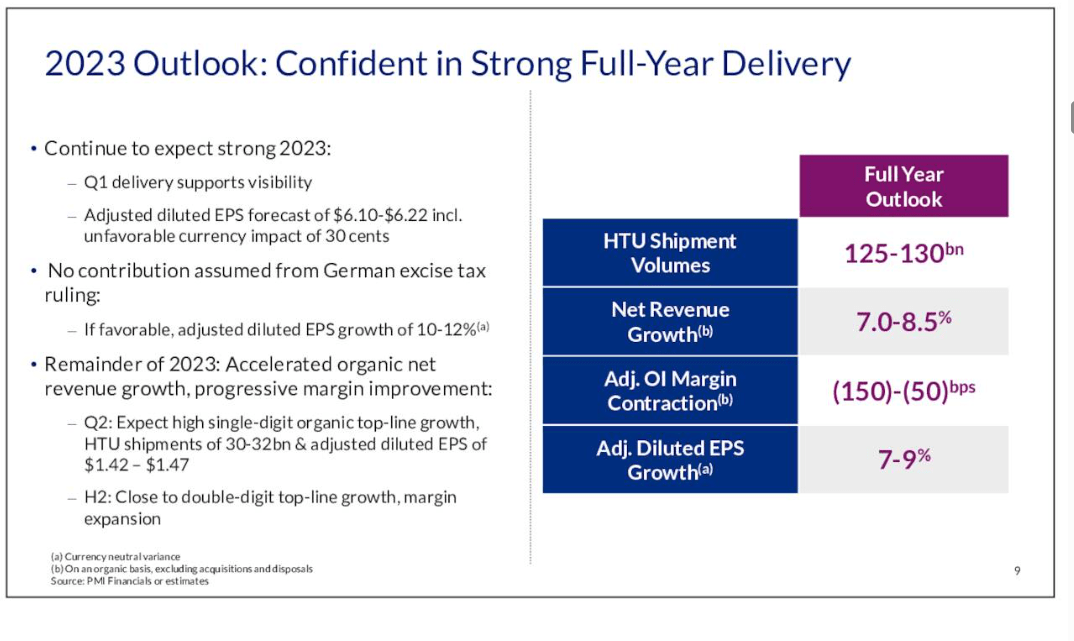

The acquisition of Swedish Match has helped give PM added smokeless exposure, and gives it US exposure in anticipation of its plan to market IQOS in the US, after having recouped the rights from Altria (MO).

PM Earnings Presentation

As a consequence, overall net revenues and net income will grow by at least 7% this year.

Last year, the dividend grew by only 1.6% in an environment in which most companies were increasing dividends below their long term trends.

At the very least I expect 3% dividend growth going forward. There's a strong case to say that PM could afford 4%-5% increases.

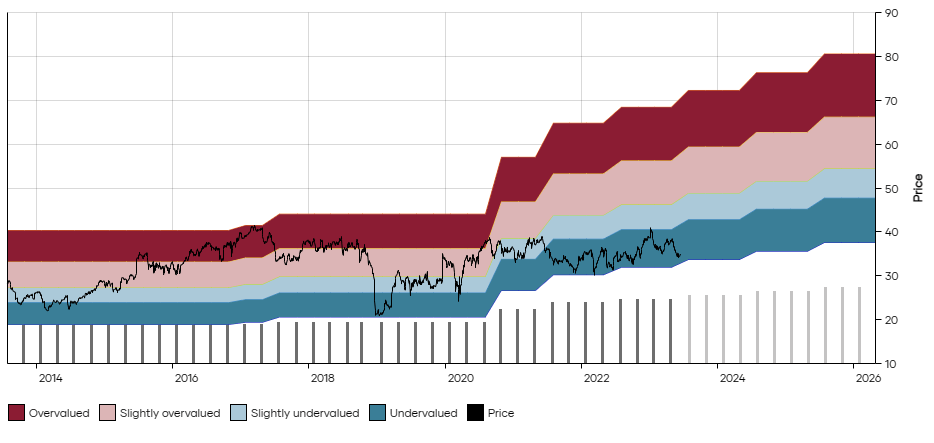

Either way, at the current price point of $94 per share, PM yields 5.35%.

PM DFT Chart (Dividend Freedom Tribe)

The dividend is super safe, supported by strong cash flows, and has clear upside over upcoming years.

I see it as a very safe investment. A couple of years of above trend dividend hikes could see the stocks yield rerated, and provide some nice capital appreciation too.

In the meantime, if we get 3% dividend growth, the income profile remains very attractive.

If you invested $10K in PM today, and reinvested at the current yield, then in year 10 you could expect $1,380 in annual income or 13.8% of your initial investment.

PM Dividend Projection (Dividend Freedom Tribe)

This is very attractive, and explains why you can comfortably buy PM, even though all the woke actors in the market are stepping away from tobacco. That means you get a "sin" discount. Just take it.

Conclusion

Buying stocks at the right price does a lot of the heavy lifting for you.

It is a well-known axiom in investing that says "you make money when you buy, not when you sell."

The point of the saying is to highlight that buying at favorable prices maximizes profit potential.

On the other hand, at least in stocks, you also make money when you sell.

You can make more money if you buy right, and sell right.

You'll never get it 100% right, and naysayers will always focus on the instances where stocks have gone lower when we buy and higher when we sell.

You never get the exact bottom or top, you just want to on average, be close enough to them so that the dividend stream you can expect from these investments is satisfactory for your long-term income goals.

We'll be sharing more of our top picks over the next few weeks

If you want to get our top 10 picks today...

We already shared all of them with members of the Dividend Freedom Tribe.

You'll also get access to our awesome tech, 3 model portfolios and weekly buy, watch, and sell lists.

Don't wait, join the Dividend Freedom Tribe! (2 Week FREE Trial)

Our model portfolios are ahead of the market since inception, and our community of nearly 900 members is always discussing latest developments in dividend stocks.

Our model portfolios are ahead of the market since inception, and our community of nearly 900 members is always discussing latest developments in dividend stocks.