mbbirdy

As a general rule, when you make an investment, you should expect that investment to take a while to pay off. Unless it's a special situation, like a merger arbitrage opportunity or something like that, you should expect to own the stock for at least a year and, very possibly, longer than that. But sometimes, the stars align and an opportunity generates upside rather quickly. Such has been the case regarding boat company Marine Products Corporation (NYSE:MPX). Over the past couple of months now, shares have moved significantly higher. This has been on the back of strong financial performance. Given how much upside we have seen, investors would be wise to take a step back and reevaluate the picture. Even a quality company that's performing well only has so much upside potential to it. Fortunately for shareholders, I would make the case that some additional upside is probably still on the table. But I also believe that the easy money has most certainly been made and I can understand why some investors might look elsewhere for opportunities.

Great performance begets great upside

It seems just like yesterday that I wrote a bullish article detailing my investment thesis for Marine Products. It wasn't quite yesterday, but it was fairly recent. The date of publication for the article was March 5th of this year. In it, I acknowledged that the company had experienced a fantastic run over the past several months. In fact, since I previously had written about the company in August of 2022, rating it a 'buy', units had appreciated by 20.1% at a time when the S&P 500 declined 7.2%.

In my article earlier this year, I stated that the company was showing little to no real weakness at that point in time. Relative to similar firms, the stock was lofty. But they did still seem to offer some upside for investors from that point. This led me to reaffirm the 'buy' rating I had on the stock previously. And so far, the results have been fantastic. Shares are up 22% at a time when the S&P 500 is up only 7.7%. In fact, since I first rated the company a 'buy' back in September of 2021, shares have generated upside of 46.4% compared to the 0.2% experienced by the broader market.

Author - SEC EDGAR Data

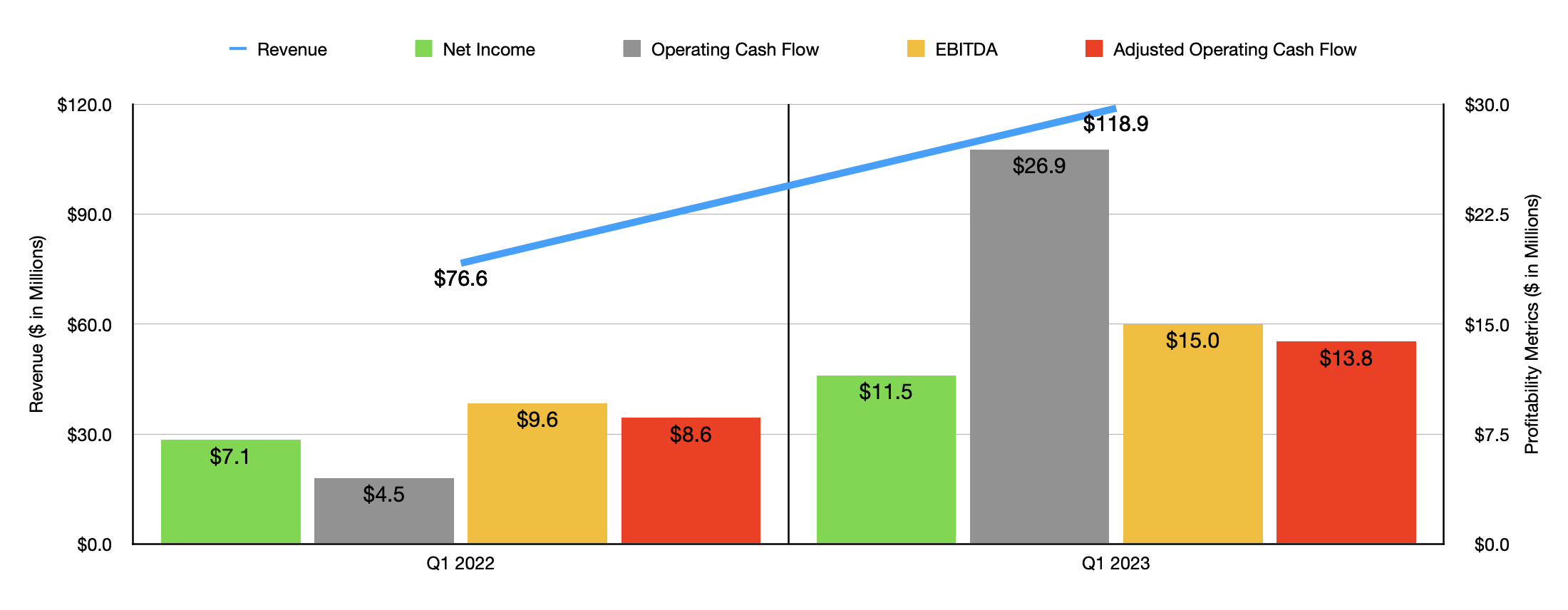

Given just how much upside we have seen in the stock, a reasonable person might assume that I believe further upside from here is limited. I definitely don't think we are going to see the same kind of returns that we saw previously. But based on the most recent data available, I remain bullish on the company. The data in question covers the first quarter of the company's 2023 fiscal year. During that time, revenue came in at $118.9 million. That's 55.2% above the $76.6 million the company reported one year earlier. There were two key drivers behind this surge in revenue. First and foremost, the number of boats the company sold grew from 916 to 1,278 over this window of time. On top of this, the average gross selling price per boat jumped from $73,500 to $82,400.

This strong showing helped the company's profitability to improve as well. Net income, for instance, spiked from $7.1 million in the first quarter of 2022 to $11.5 million the same time this year. Operating cash flow skyrocketed from $4.5 million to $26.9 million. Though if we adjust for changes in working capital, we would have seen this growth come in quite a bit lower, with a metric still climbing from $8.6 million to $13.8 million. And finally, EBITDA for the enterprise grew from $9.6 million to $15 million.

Those who disagree with my assessment of the company can rightfully argue that economic conditions are changing. Persistent inflation, combined with high interest rates aimed at combating that inflation, are not exactly conditions that would be bullish for the boating industry. But management remains adamant that strong conditions are here to stay for at least the rest of 2023. In their quarterly report, for instance, they stated that while revenue growth might moderate as retail demand becomes satisfied and as consumers return to more normal lifestyles following COVID-19 and because of economic concerns, they don't see these factors having a materially negative impact throughout this year.

Author - SEC EDGAR Data

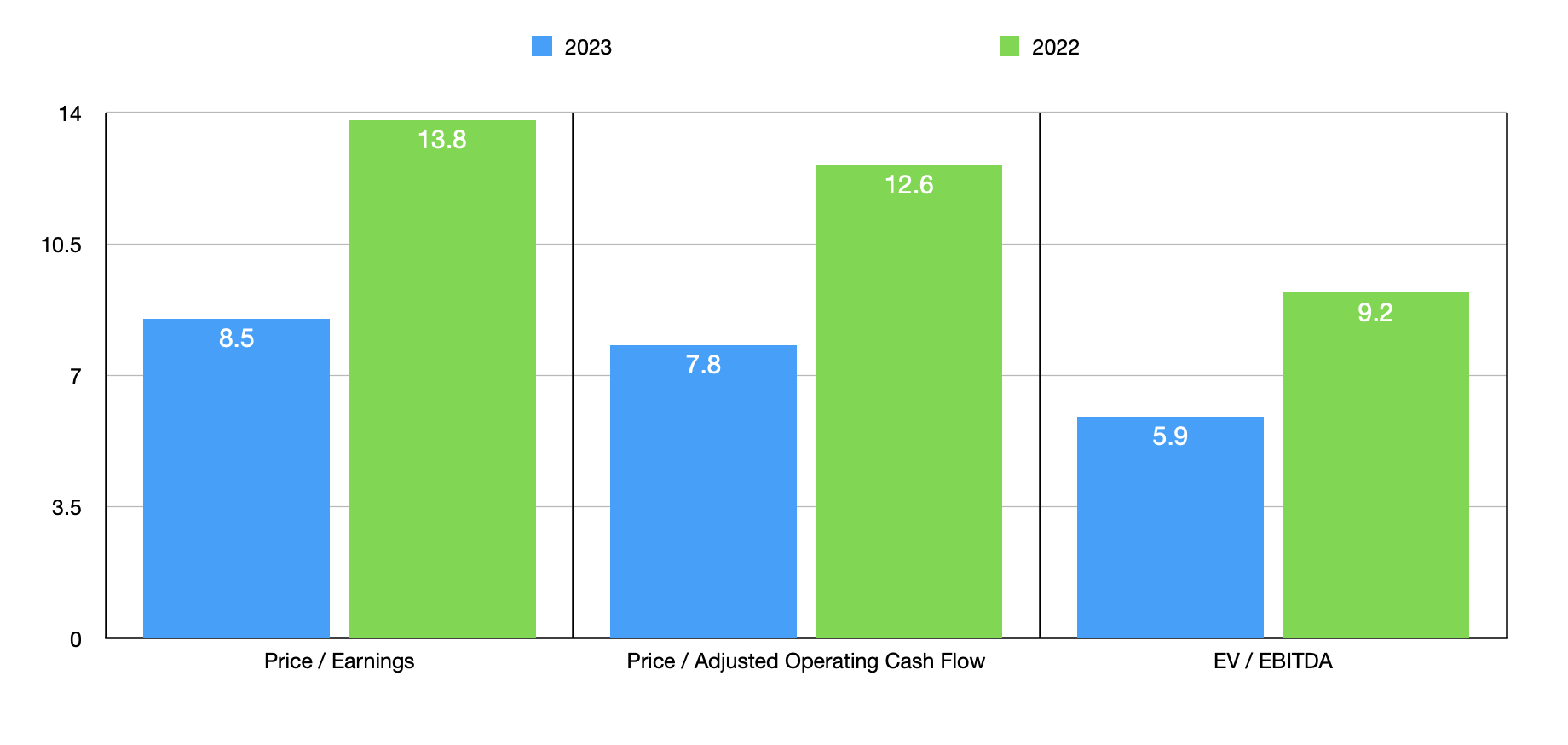

Unfortunately, management has not provided any guidance for the current fiscal year. But if we annualize the results experienced during the first quarter, we could expect net income of $65.3 million. Adjusted operating cash flow would be $71.1 million, while EBITDA would be around $83.9 million. Using these estimates, the company seems to be trading at a forward price to earnings multiple of 8.5. This is quite low, especially compared to the 13.8 reading that we get using data from 2022. The price to adjusted operating cash flow multiple should drop from 12.6 using last year's data to 7.8 this year. And over that same window of time, the EV to EBITDA multiple should decline from 9.2 to 5.9.

While it might be tempting to utilize these forward estimates, investors would be wise, given how early we are in the year and lacking guidance from management, to use the results achieved in 2022 instead. Using these figures, I then compared the company to five similar firms in the table below. On a price to earnings basis, two of the five companies ended up being cheaper than Marine Products. Using the price to operating cash flow approach, two were cheaper, while another was tied with it. And finally, when it comes to the EV to EBITDA approach, three of the companies ended up being cheaper than our target.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Marine Products Corporation | 13.8 | 12.6 | 9.2 |

| Malibu Boats (MBUU) | 7.0 | 7.8 | 4.6 |

| Brunswick (BC) | 10.1 | 8.7 | 6.8 |

| MarineMax (HZO) | 4.4 | 9.1 | 5.3 |

| MasterCraft Boat Holdings (MCFT) | 9.1 | 3.7 | 4.3 |

| BRP Inc. (BRP) | 9.7 | 6.8 | 6.7 |

Takeaway

Relative to similar firms, shares of Marine Products are looking more or less fairly valued. On an absolute basis, they do look close to that as well, though they may offer a bit of upside. If the first quarter is any indication of how the rest of the year will be, shares could experience even more upside than what I anticipate. After all, such strong results would make the firm very affordable. We also need to keep in mind that, at some point, there probably will be some material weakness in this space. It may not come until next year, but it is likely to come all the same. Fortunately, Marine Products is healthy enough to handle such a downturn. I say this because it has no debt on its books and it enjoys cash and cash equivalents of $62.6 million. That's an excellent position to be in for a company with a market capitalization of less than $560 million. With all this said, I believe that shares probably do warrant a bit more upside. Enough to make it still classified as a 'buy' to me, but just barely.

Crude Value Insights offers you an investing service and community focused on oil and natural gas. We focus on cash flow and the companies that generate it, leading to value and growth prospects with real potential.

Subscribers get to use a 50+ stock model account, in-depth cash flow analyses of E&P firms, and live chat discussion of the sector.

Sign up today for your two-week free trial and get a new lease on oil & gas!