Ralf Hahn/iStock via Getty Images

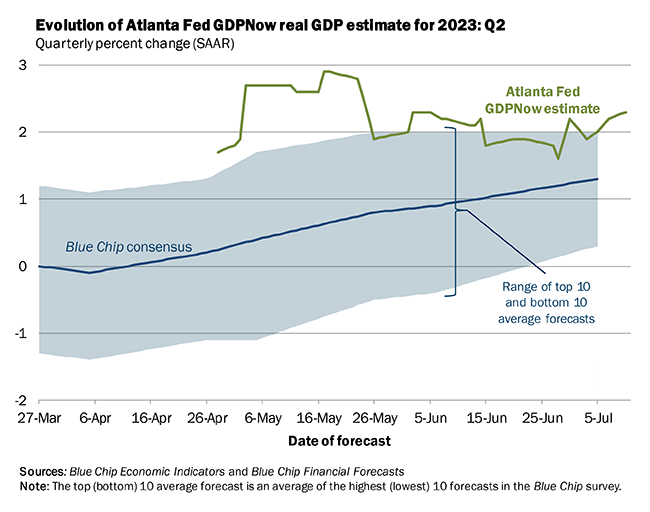

Everything seems to be coming up roses for the "non-recession" bulls. Not only is a soft economic landing now firmly likely, but a “no landing” scenario of continued US real GDP growth could be in the works. As of July 18, 2023, the Atlanta Fed’s GDP now figures for the second quarter show that the domestic economy likely expanded at a real rate of 2.3% (quarter-on-quarter, seasonally adjusted annual rate).

Q2 2023 Real GDP Growth Expected to Have Printed 2.3%

Atlanta Fed

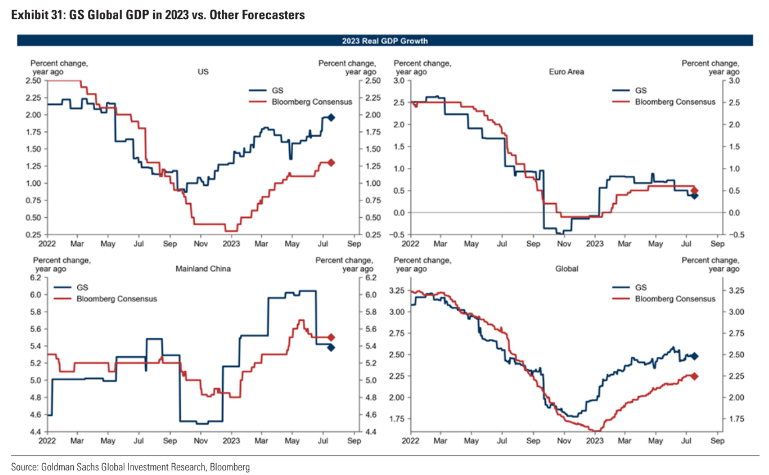

Still, the consensus outlook currently suggests that the Q3 sequential rate of growth may be a goose egg before activity picks back up in Q4 and beyond. But, according to Goldman Sachs, full-year 2023 economic growth net of inflation should verify above 1% on a Q4/Q4 basis.

US Real GDP Growth Rate Seen North of 1% in 2023

Goldman Sachs

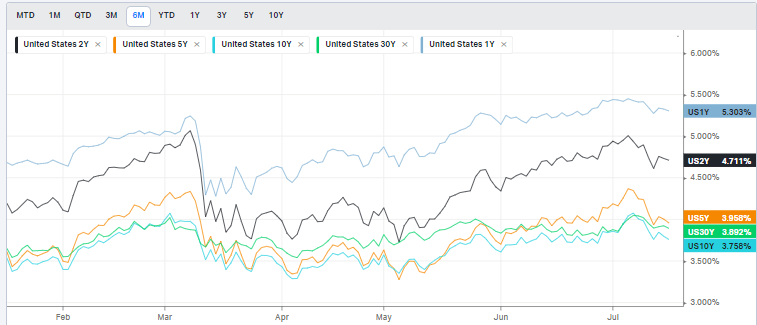

Of course, the big macro news last week was a better-than-expected CPI report. Both the headline and core rates were on the soft side, and stocks and bonds consequently rallied. Interest rates, particularly those on the short end of the curve, plunged. The 2-year yield had climbed to near cycle highs, peaking just shy of the March 2023 peak above 5%.

Treasury Rates Retreat Post-CPI

Koyfin Charts

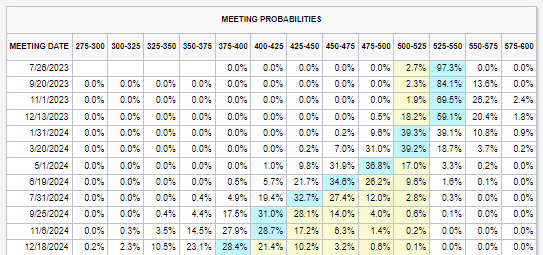

All eyes are now on the July 26 Fed rate decision. I will do a full FOMC preview next week, but as it stands, the market has priced in a virtual certainty about the prospects for an additional quarter-point rate hike with a terminal rate about 4 months away, according to the CME FedWatch Tool.

One and Done? Fed Funds Futures.

CME FedWatch Tool

What does it mean for investors? T-bills are increasingly attractive these days, particularly as stock market valuations march higher and higher. I reiterate my buy rating on the iShares Short Treasury Bond ETF (NASDAQ:SHV) given that the product will soon yield north of 5.25% based on my calculations (assuming the outlook for a peak Fed rate occurs later this year).

For background, SHV seeks to track the investment results of an index composed of U.S. Treasury bonds with remaining maturities of one year or less offering investors access to a specific segment of the U.S. Treasury market, according to iShares. It is a very straightforward product as it does nothing more than hold a basket of ultra-short-dated Treasury securities. Given that inflation is now running at just 3%, and with stunningly low inflation expectations—under 2%--simply stashing cash in SHV is an inflation-adjusted winning strategy. Call it a “real” value.

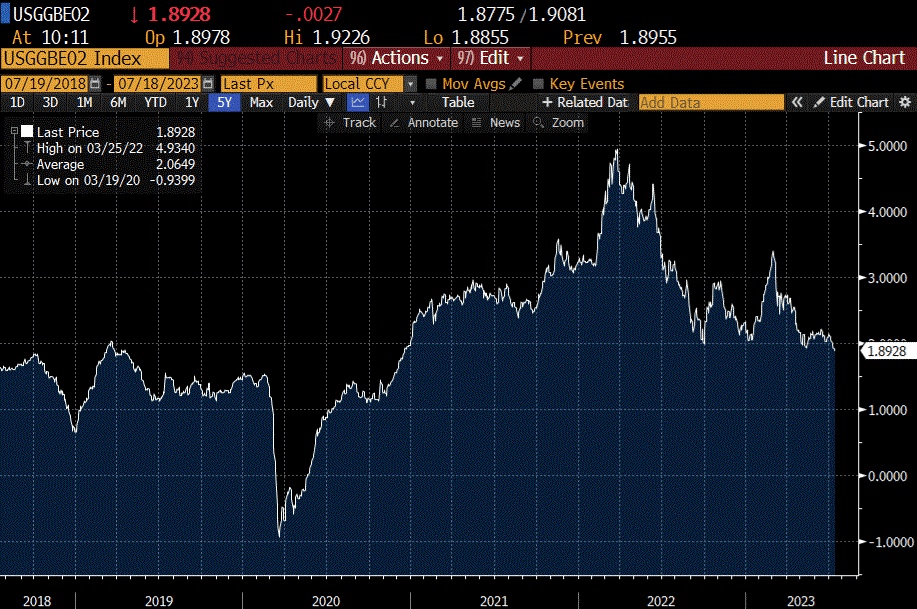

2-Year Inflation Breakevens: 1.9%

Bloomberg

SHV has more than $20 billion in assets under management and is currently priced very close to its net asset value per share. With a 30-day median bid/ask spread of just a single basis point as of July 17, 2023, the fund’s tradeability is strong. That assertion is evidenced further by its high typical trading volume that sums to more than three million shares daily.

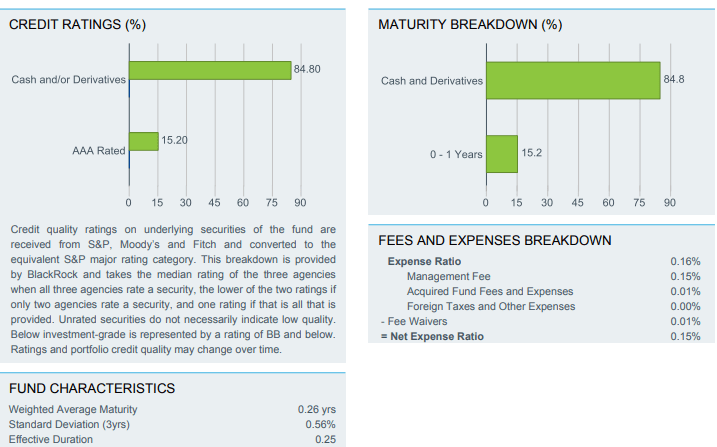

Holding 13 securities, per iShares, SHV’s 30-day SEC yield is now above 5% (5.04% to be precise) while its average yield to maturity is 5.17% - it is key to recognize that percentage has baked in market expectations for a higher effective Fed Funds rate come next week. As with most Treasury ETFs, comparing yields to maturities (or yields to worst) is a useful tactic (as opposed to the SEC yield or other trailing yield gauges). SHV has an annual expense ratio of 15 basis points, which is near what other comparable-duration Treasury ETFs cost.

SHV: 3-Month Duration, 0.15% Expense Ratio

iShares

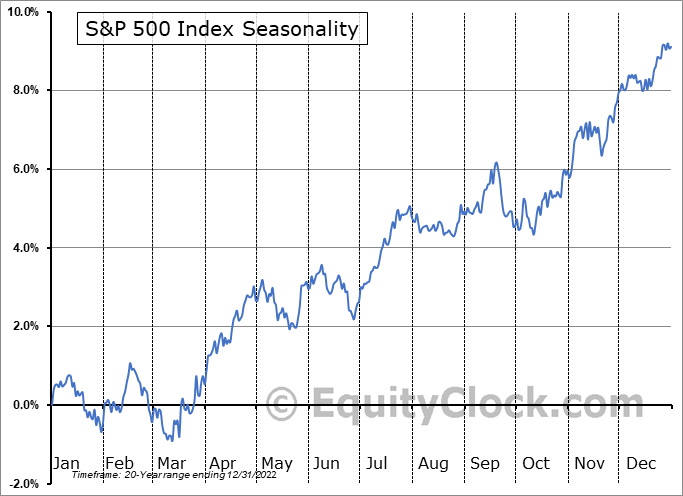

SHV could also be a decent parking spot right now considering we are, at long last, about to enter a historically bearish stretch of the calendar, according to data from Equity Clock. Late July through early October has tended to produce market corrections and a rise in equity volatility, making safe short-term Treasurys all the more appealing.

S&P 500 Volatility Ahead? Less Sanguine Seasonality Ensues.

Equity Clock

The Bottom Line

I reiterate my buy rating on SHV. I continue to like its low cost, high liquidity, strong yield (now sharply above the inflation rate), and it is particularly attractive today considering the possibility of seasonal headwinds in equity markets and as the Fed nears the end of its rate-hiking cycle.