katrinaelena

Investment Overview

Moderna (NASDAQ:MRNA) and BioNTech (NASDAQ:BNTX) are two companies which may forever be compared thanks to their focus on messenger-RNA focused drug discovery, and the critical role each played in the mass vaccination campaign that helped end the COVID pandemic.

Moderna and BioNTech launched their initial public offerings ("IPOs") within one year of each other, with Modena raising $604m at $23 per share in December 2018, and BioNTech raising $150m at $15 per share in October 2019.

Although both companies were primarily focused on research as opposed to near-term product development, both quickly became household names thanks to their development of successful COVID vaccines, which both won Emergency Use Authorization ("EUA") in the same month - December 2020.

Moderna's Spikevax, and BioNTech and partner Pfizer's (PFE) Comirnaty, went on to become the dominant selling COVID vaccines in the US and Europe, and helped both companies realize astonishing revenue and income figures in 2021 and 2022. Moderna earned $18.5bn in 2021 and $19.3bn in 2020, driving net income of $12.2bn and $8.3bn, respectively, while BioNTech earned $21.6bn and $18.5bn in 2021 and 2022, and net income, respectively, of $11.7bn, and $10.1bn.

This unexpected source of revenues led to both companies' stock prices soaring, reaching highs in 2021 that neither company's management would likely have ever dreamed of.

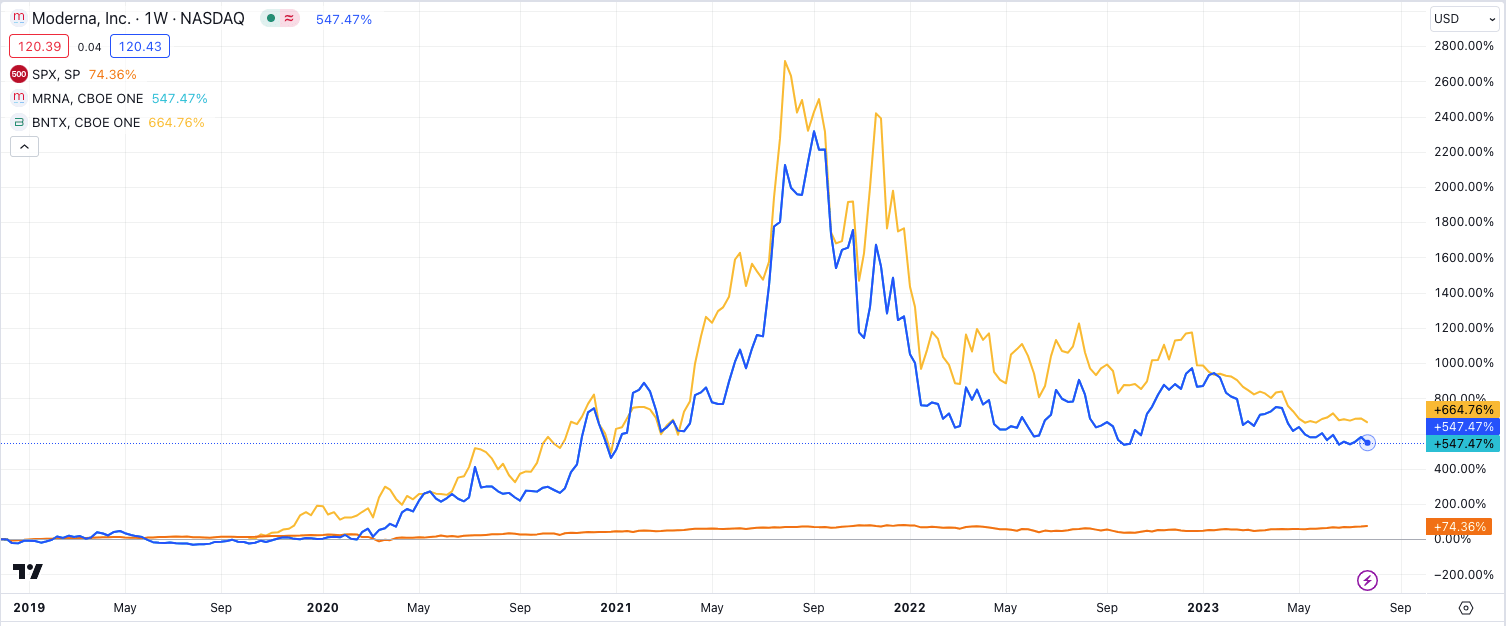

Moderna & BioNTech share price performance - past 5 years (TradingView)

As we can see above, at their peak in August 2021, both companies' shares were up over 2,000% since IPO, with Moderna's market cap valuation almost reaching $190bn, and BioNTech's close to $100bn.

Looking back, these valuations were based on both companies providing a similar level of vaccines to the US, European and other key markets for another 5-10 years - ~800m per annum in Moderna's case, and 1bn in Pfizer / BioNTech's case - and we now know that's no longer necessary, as the pandemic has been declared over, and governments are no longer sponsoring vaccine purchases.

In that context, how should we think about the valuations of these two companies today, and how should we forecast their sales and profitability going forward, to help make the picture clearer for investors? In this post I will try to answer some of these questions by discussing the shift from a pandemic, government sponsored market to an endemic, private market in COVID vaccination, the company's other products in development, and some approaches to calculating a "fair value" target share price.

Moderna & BioNTech - Recent Performance and FY 2023 Forecasting

Neither Moderna nor BioNTech has reported Q2 2023 earnings so far. Moderna is set to report on Aug. 3, and BioNTech on Aug. 7. Even the company's reporting dates can barely be separated!

In Q1 2023, Moderna earned $1.83bn of revenues - all from COVID vaccine sales - down 69% year-on-year, while operating expenses increased by 21%, to $2.2bn, leaving net income as just $79m, or $0.19 per share, vs. $8.58 per share in Q1 2022. The company was still able to report a cash position of $16.4bn, however, even after completing $526m of share repurchases at an average price of $145 per share.

In Q1 2023, BioNTech earned revenues of ~$1.43bn - all from Comirnaty sales revenues, which are split 50/50 with partner Pfizer, delivering earnings per share of $2.25, and reporting a cash position of ~$14bn. Revenues fell ~80% year-on-year.

While Moderna has provided full year 2023 guidance for revenues of $5bn - again, all from sales of COVID vaccines, BioNTech is forecasting for €5bn of revenues, which translates to ~$5.5bn dollars of revenues, and a profit after tax of ~$1bn, or ~$4.2 per share, for a forward PE of ~25.5x. For Moderna's part, the company forecasts it will spend ~$4.5bn on R&D, and ~$1.5bn on SG&A, resulting in a probable loss of ~$1bn, or $(2.6) per share.

Assessing The Likely Private / Endemic COVID Vaccine Market

Looking at the above, and considering the respective market caps of Moderna and BioNTech - Moderna is currently valued at ~$45bn, and BioNTech at $25.4bn, it might seem logical that investors would opt to back BioNTech - neither company pays a dividend at this time.

With that said, however, Moderna owns its COVID franchise in its entirety, unlike BioNTech, which must rely on its continuing collaboration with Pfizer, and although Moderna made negligible vaccine sales to the US in Q1 2023 - its sales were shared between Europe - $0.6bn, and RoW - $1.3bn - the company has been doing its homework into the emergence of a private COVID market in the US.

In a Fireside Chat at the Goldman Sachs Healthcare Conference in June this year, Moderna's Chief Financial Officer ("CFO") Jamey Mock suggested that Moderna's research revealed a ~100m patient per annum market in the US, and reiterated that Moderna planned to price its vaccine at $129 per dose - up from the ~$25 per dose fee it charged governments - implying an overall market of ~$13bn.

On its Q123 earnings call, BioNTech did not offer any market research of its own, although Chief Strategy Officer ("CSO") Ryan Richardson sounded a bullish note:

In the midterm, we see multiple potential growth drivers for our COVID-19 vaccine franchise. These include the potential for volume growth as the seasonal market is established, particularly in high-risk population segments.

In addition, we believe continued innovation from variant adapted vaccines, next-generation vaccines and possible respiratory combination vaccines have the potential to support future franchise growth. The transition to private markets in certain regions is likely to take several years. We believe the shift to commercial pricing will provide further midterm growth potential.

We and our partner, Pfizer, believe in the value that our COVID-19 vaccines provide both to individuals and health systems, and we will continue to invest to maintain our leadership position in the market.

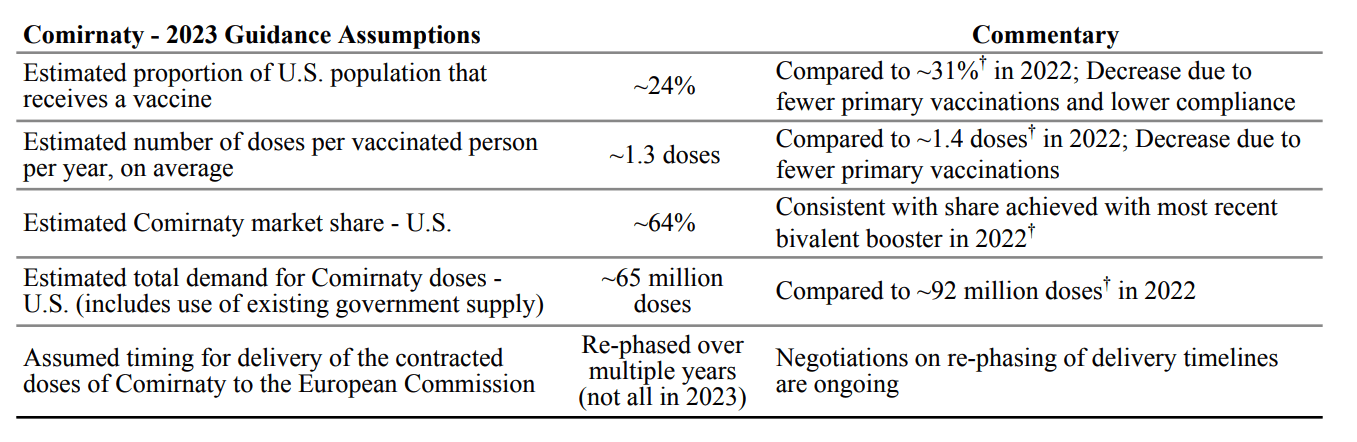

Additionally, partner Pfizer shared some expectations for the COVID market from 2023 and beyond in its Q4 2022 earnings press release as shown below:

Pfizer COVID market / revenues guidance (earnings release)

In summary, both Moderna and BioNTech have reasons to be optimistic around the emergence of a private COVID vaccine market and the two companies are likely to divide market share between them. Pfizer / BioNTech enjoyed the large market share in the US - ~64%, as per the above table, and if their prediction for a demand of ~65m doses per annum proves correct, based on a price per dose of $129, the two companies can expect to divide ~$8.4bn of revenues per annum between them. Moderna itself could drive ~$4.7bn revenue per annum based on a 36% share of its forecast $13bn market.

We should not forget, either, that a private market may well open up in Europe and other parts of the world also - which is where both companies have been making the majority of their sales recently.

Other Products and Pipelines - Moderna's Near-Term Market Opportunities More Tangible?

The emergence of a private COVID market is a phenomenon both Moderna and BioNTech are pinning their hopes on - and it's hard to argue that there will not be significant demand for such a vaccine. For context, the flu market is estimated to be ~169 doses in the US annually, and worth ~$7.2bn in FY22, with GSK (GSK), Sanofi (SNY), and AstraZeneca (AZN) significant players. 169m doses per annum would translate to a market of ~$21bn for COVID shots, which are currently priced higher than flu shots. The FDA's advisory committee has made its decision on which strain companies must target for a fall vaccination program, and both Moderna and Pfizer will be ready.

Both Moderna and BioNTech are targeting more vaccine approvals, however. Moderna is very close to securing an approval for an RSV vaccine, having made its global regulatory submissions this month, based on a vaccine efficacy of ~83% against RSV-LRTD as defined by two or more symptoms, and 82% as defined by three or more symptoms. An approval would likely pitch Moderna in a three-way fight for market share against GSK, whose RSV vaccine already is approved, and against Pfizer, whose vaccine also is likely to be approved soon.

Flu is another target for Moderna - in April, the company announced it had not met the criteria for "early success" in its pivotal study, but nevertheless, the company expects an approved flu shot to be a revenue driver by 2024. Here's CFO Mock again, speaking at the GS Healthcare conference:

I'll just break down the overall TAM that we see right now. So we think COVID is, today, a $15 billion marketplace. And I think a range on that is $10 billion to $20 billion, but let's say, $15 billion. Flu is about a $6 billion marketplace. And then RSV, not including maternal and infants, is about an $8 billion marketplace right now. So that gets you to close to $30 billion, thereabouts. That will grow over time due to inflation as well as what we're targeting is older adults. And the percentage of older adults and the population in the globe is growing faster than the rest of the population. So we think that grows over time.

But if you take a $30 billion number, our $8 billion is about 25% share. $15 billion would obviously be 50% share. If it's at the high end, and you say it's $40 billion, maybe we're 40% share and if it's only $25 billion, we're a 33% share. So we feel comfortable in this 25% to 50% share range.

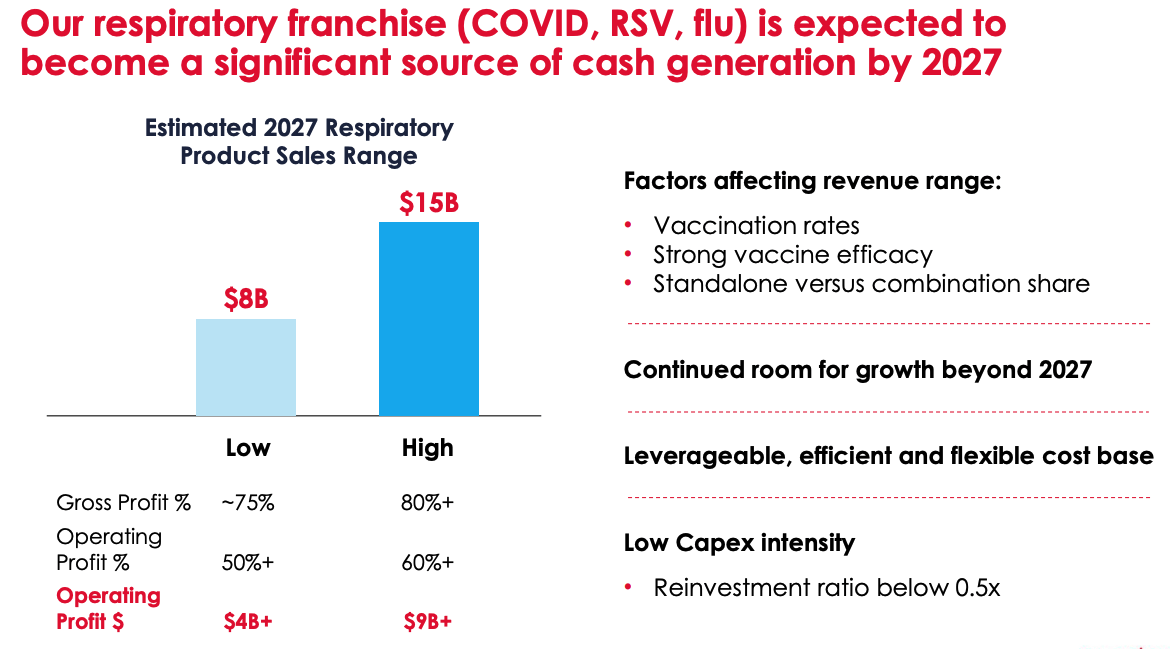

Moderna respiratory franchise forecast (earnings presentation)

As we can see above, Mock's estimates are backed up by Moderna's Q1 2023 earning presentation, and the company is promising a strong return to profitability, with an operating profit of $4 - $9bn promised by 2027. There are clearly many unknowns in play as there is a $5bn difference between the low number and the high, but even if we take the lower number, a posited forward price to earning ratio - at Moderna's current valuation - could be just over 10x, and if we use the higher number, it could be as low as ~5x, which is a strong buy signal.

Turning to BioNTech and its infectious disease programs, the company has some very intriguing vaccines in development, including against shingles - GSK's shingrix vaccine earned nearly $3bn of revenues in 2022 - malaria, and tuberculosis, but its programs are not nearly as far advanced as Moderna's, meaning there is little prospect of near-term revenues.

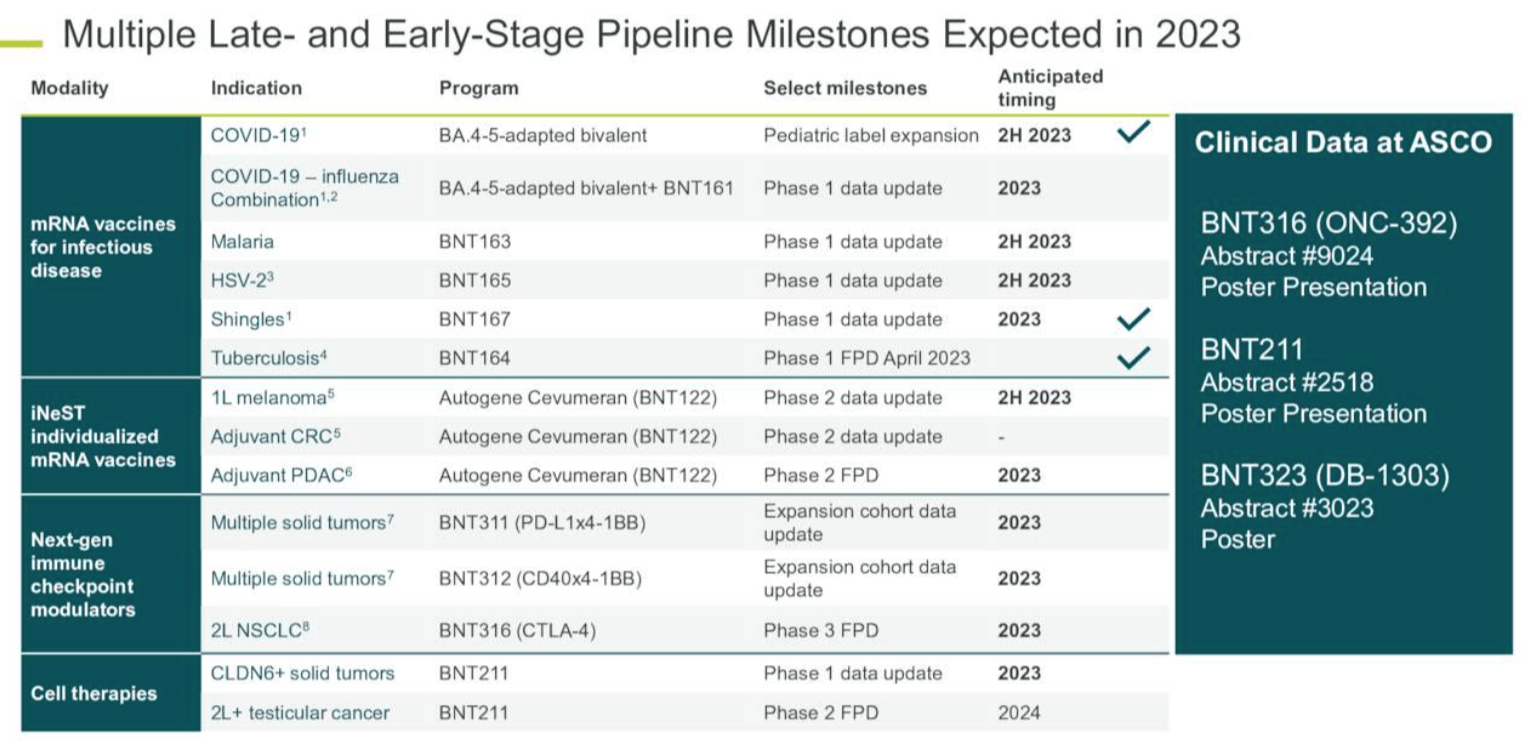

BNTX pipeline (BNTX Q1 2023 earnings presentation)

As we can see above, BioNTech has other important programs that are further advanced, including in oncology - although so does Moderna - which is our next area for analysis.

Oncology - Both BioNTech and Moderna Are Developing Near-Term "Shots on Goal"

Our final point of comparison for this post is within the field of oncology. As we can see above, BioNTech has a Phase 3 stage asset in its Non-Small Cell Lung Cancer candidate BNT-316 (ONC-392), which targets CTLA-4 - a recognized target for cancer drugs - Bristol-Myers Squibb's (BMY) Yervoy targets this protein, earning >$2bn of revenues last year. BioNTech's CEO Ozlem Tureci told analysts on the company's Q1 2023 earnings call:

A total of about 600 patients are planned to be enrolled and randomized 1:1 to receive either on ONC-392 or docetaxel in this two-stage study. The primary endpoint is overall survival with objective response rate, PFS and safety as secondary endpoints. The study is planned to start enrolling patients within the next few weeks.

If ONC-392 were to establish a superior safety and efficacy profile to Yervoy, it would open up a substantial market opportunity for BioNTech, decreasing its reliance on Comirnaty. Final data may be at least 18 months away, however.

There are other highlights from this oncology pipeline - such as the objective response rate ("ORR") of 57% and Disease Control Rate ("DCR") of 85% generated by CAR-T cell therapy BNT211 in testicular cancer which was presented last year at ESMO - and like Moderna, BioNTech is in the process of developing "personalised cancer vaccines" ("PCVs"). Its candidate autogene cevumeran has shown promising progress in combo with Swiss Pharma giant Roche's (OTCQX:RHHBY) Tecentriq plus chemotherapy, although once again, it is Moderna that may be closer to a first approval for a PCV.

I have covered Moderna's partnership with New York based pharma giant Merck & Co. over neo-antigen MRNA-4157 in previous posts for Seeking Alpha, explaining that:

In the case of PCVs, samples of a patient's tumor are taken and used to create customized injections for each patient, targeting 34 separate mutations to enable T-cells to spot and attack these mutations and prevent cancer growth.

Moderna and Merck announced last year that in studies in patients with melanoma (skin cancer), Merck's Keytruda + MRNA-4157 reduced risk of recurrence or death by 44%. It's exciting news - albeit some observers suggested that melanoma is "low hanging fruit" compared to other types of cancer, and questioned some trial protocols - and the two companies recently announced that they have begun a Phase 3 study of this combination in ~1,000 patients. In fairness, it will take time to complete this Phase 3, but given there is strong data from the prior Phase 2 study, there is a good likelihood the Phase 3 will also be successful in this instance.

In summary, it's BioNTech that arguably has the wider, more diverse oncology pipeline, but Moderna that is driving toward the finish line with a "cancer vaccine" product that has never been approved before, and a powerful partner in Pharma giant Merck.

Concluding Thoughts - Should Investors Buy Moderna Or BioNTech? Both Are Strong Companies With Plenty To Offer, But I Make Moderna The Better Bet Over Next 12 Months

Hopefully this post has provided some color around two companies that, as I mentioned in my intro, will likely always be compared owing to their research based roots, COVID fame, ambitious and far-sighted leaders, similar levels of revenue and profitability growth - and now declines - and with their pipelines focused on similar goals.

How to separate the two for investors? At this stage, I make Moderna marginally the better buy. The company is currently more commercially focused, with its RSV vaccine on the verge of approval, and it has presented a clear route back to revenues of up to $15bn by 2027, and strong profitability, backed up by tangible approval shots in flu and potentially oncology.

BioNTech may be a little over-reliant on COVID vaccine revenues, and its partner Pfizer, although it's cheaper, with a much smaller market cap, flush with cash, and has a diverse pipeline replete with intriguing opportunities. It's by no means a bad company.

In time, BioNTech may emerge as the superior buy - it may depend on which company wins the race to develop the holy-grail triplet vaccine that can tackle flu, RSV, and COVID together - again, I put Moderna marginally ahead in that race, although I believe BioNTech has the more sophisticated oncology programs at present and is more focused on that market than any other, while Moderna is looking at heart failure and rare disease.

A final point to make - neither company expects to generate much in the way of revenue when they announce their Q2 2023 earnings early next month, and as such, the market may be reacting negatively to this perceived earnings miss, although both companies expect to outperform strongly in the second half of the year based on the emergence of the private COVID market.

As such, at the current price, both company's shares represent a tempting, and promising buy, in my view.

If you like what you have just read and want to receive at least 4 exclusive stock tips every week focused on Pharma, Biotech and Healthcare, then join me at my marketplace channel, Haggerston BioHealth. Invest alongside the model portfolio or simply access the investment bank-grade financial models and research. I hope to see you there.