Alex_533/iStock via Getty Images

Investment Thesis

United Rentals, Inc.’s (NYSE:URI) revenue should benefit from secular demand tailwinds arising from reshoring trends, increased investments in the energy sector, U.S. infrastructure spending, and an ongoing shift in preference from ownership to renting equipment. The larger players are gaining market share in the equipment rental industry due to scale advantage and URI is well-positioned to benefit from this with ~17% market share in the industry. In addition, the company’s focus on product line expansion and cross-selling of specialty products and services should support revenue growth in the medium to long term.

On the margin front, the company should benefit from cost synergies from Ahern integration, operating leverage, increased efficiencies, and improved revenue mix from a shift towards higher margin specialty business. The current valuation is lower than historical averages. This, combined with good growth prospects makes URI stock a buy.

Revenue Analysis and Outlook

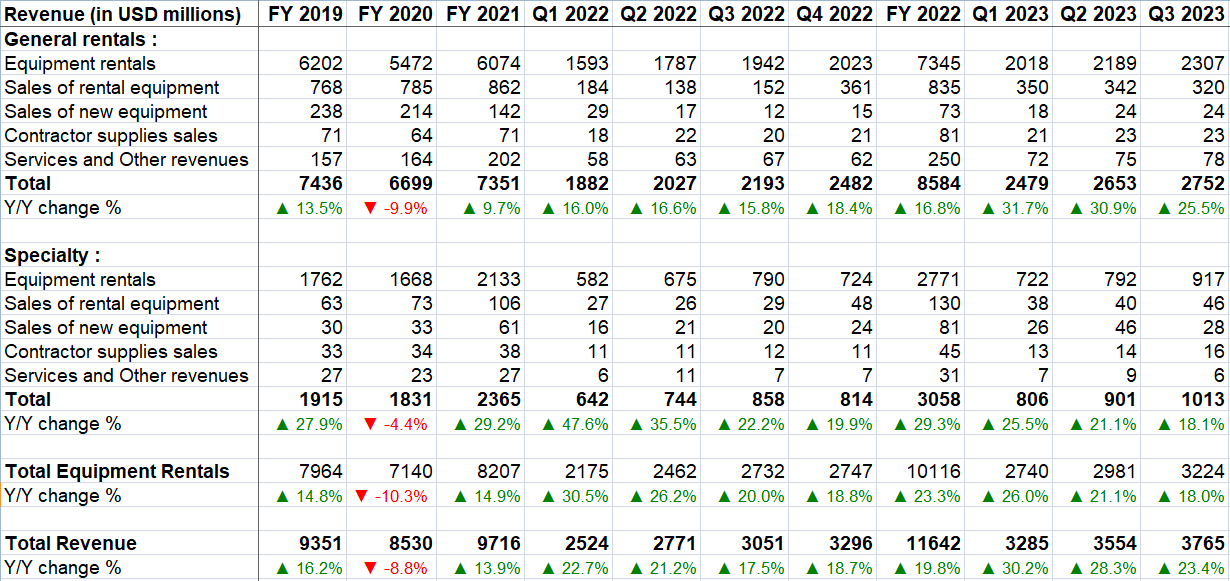

The company’s revenue has benefited from strong end-market demand in recent years. In the third quarter of 2023, URI reported an 18% Y/Y increase in equipment rental revenues to $3.224 billion supported by broad-based demand growth across its end markets and a 22.2% Y/Y increase in average original equipment at cost (OEC). The increase in average OEC includes the impact of the Ahern Rentals acquisition.

While, the fleet productivity was down 2.2% in the quarter, on a pro forma basis (including the pre-acquisition results of Ahern Rentals) the fleet productivity was up 1.5%. On a pro-forma basis, equipment rentals grew 9.8% Y/Y.

Segment Wise, the General Rentals segment’s rental revenue grew 18.8% Y/Y to $2.307 billion, and the Specialty segment’s rental revenue increased 16.1% Y/Y to $917 million.

URI’s Historical Revenue Growth (Company Data, GS Analytics Research)

Looking forward, the company’s growth outlook remains solid with strong end-market demand, a shift in preference from ownership to renting equipment, continued growth in specialty business, and M&A opportunities.

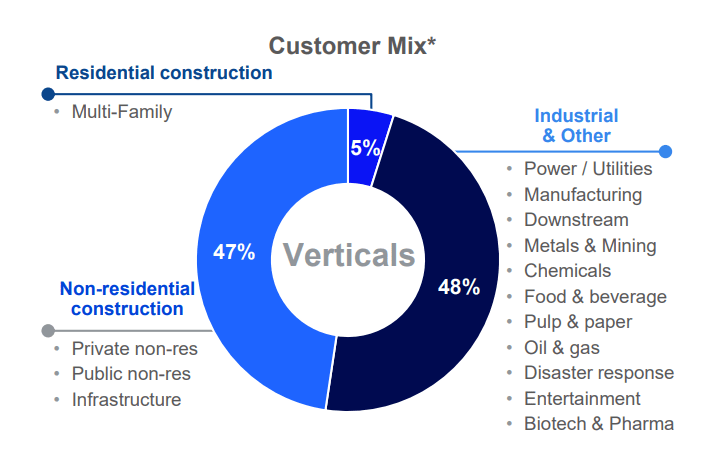

URI serves three principal end-markets for equipment rental - Industrial and other non-construction ( ~48% of rental revenue), non-residential construction (~47% of rental revenue), and residential construction (~5% of rental revenue).

URI’s End Market Mix (as per FY22 revenues) (Company’s Presentation)

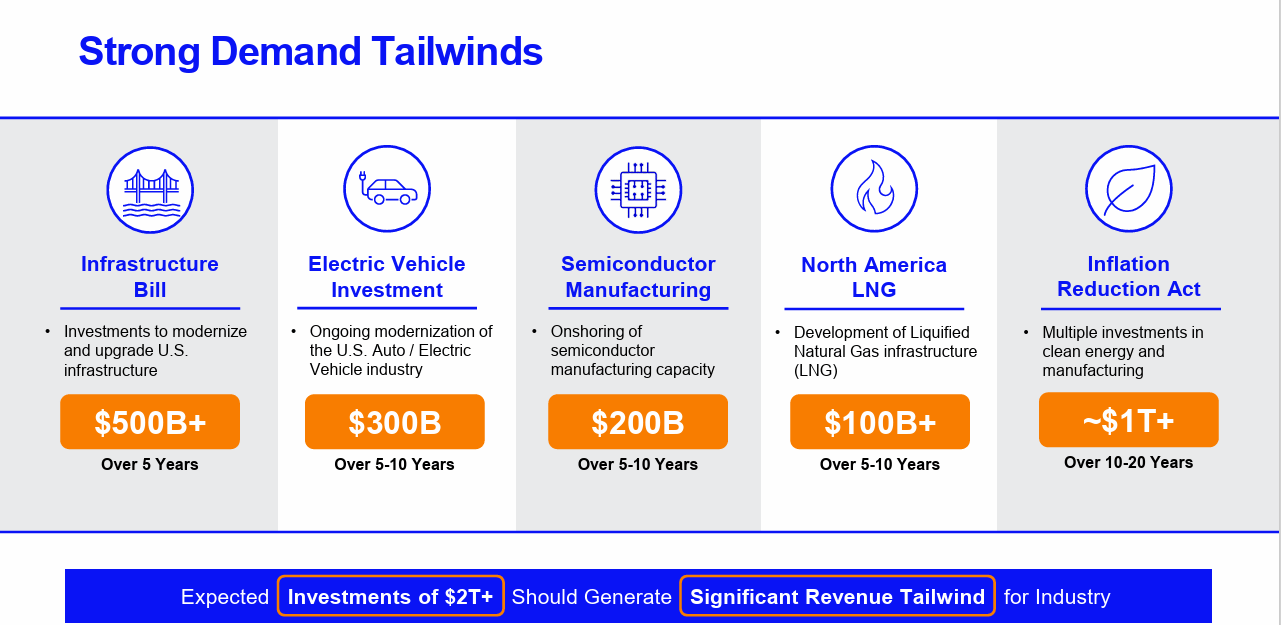

The company’s business is poised to benefit from strong U.S. construction as well as industrial manufacturing projects supported by funds allocated from the Infrastructure Investment and Jobs Act (IIJA), CHIPS and Science Act, and Inflation Reduction Act (IRA). These funds along with an increasing focus on supply chain resiliency and energy independence are driving demand for Infrastructure projects, EV investments, Semiconductor manufacturing, North American LNG infrastructure investments, and other investments in clean energy and manufacturing which are expected to drive good demand for the company’s rental fleet for the next several years.

URI’s Secular Demand Tailwinds (Company’s Presentation)

While some investors are worried about slowing office and commercial projects due to the macro slowdown, these two verticals account for ~20% of the company’s non-residential construction business. The company is seeing strong growth in other verticals including manufacturing, public road and highway, power, communication, transportation, and healthcare which account for ~55% of non-residential construction revenue. So, the strength in these other verticals should more than offset any slowdown in office and commercial projects in the near term.

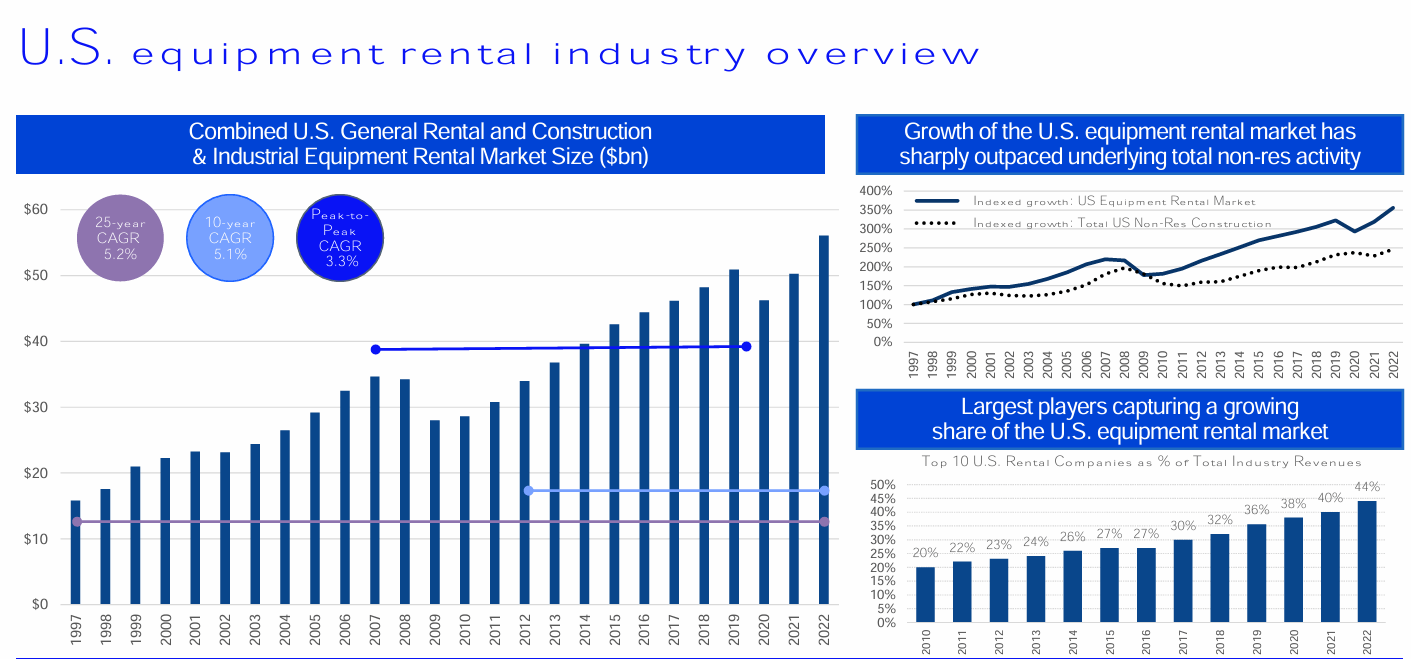

The company is also benefiting from a secular shift in preference towards renting equipment over ownership driven by factors like the high cost of equipment ownership, the need for specific machinery for short-term projects, and the flexibility and cost savings offered by rentals. The U.S. rental equipment industry has grown at a CAGR of 5.1% over the past 10 years, outperforming underlying non-residential activity. Further, there are good economies of scale in this business due to larger equipment rental companies having greater purchasing power with equipment manufacturers, more financial strength to do national advertising, and better resources to address the need for national accounts customers present across multiple states. The top 10 players have continued to gain market share in this industry due to these factors and URI, with a 17% market share of the North American equipment rental industry, is well positioned to gain further share.

U.S. Equipment Rental Industry Overview (Company’s Presentation)

The growth in the high-margin Specialty business is another driver for the company. This business has grown at a CAGR of 27.8% over the last 10 years and represented ~30% of its total revenues last year versus ~7% of total revenue in FY2012. The company is focused on the expansion in adjacent specialty product and service lines and cross-selling them to its existing clients which is driving this solid growth. The company opened 35 specialty branches in 2022 vs. 30 in 2021 and 15 in 2020, and is on track to open 40 plus branches in 2023. The continued expansion of the Specialty portfolio should help the company increase sales and position itself as a “one-stop” shop for its customers providing a complete offering of jobsite equipment rental solutions.

In addition to good organic growth prospects, I expect the company to continue doing M&As to strengthen its position in the rental equipment market and drive growth. The company’s net leverage as of the third quarter end was ~1.8x which is at an all-time low and below its 2x to 3x leverage target. So, the company is well-positioned to capitalize on any attractive acquisition opportunity that may present itself.

Overall, I am optimistic about the company’s near as well as long-term prospects.

Margin Analysis and Outlook

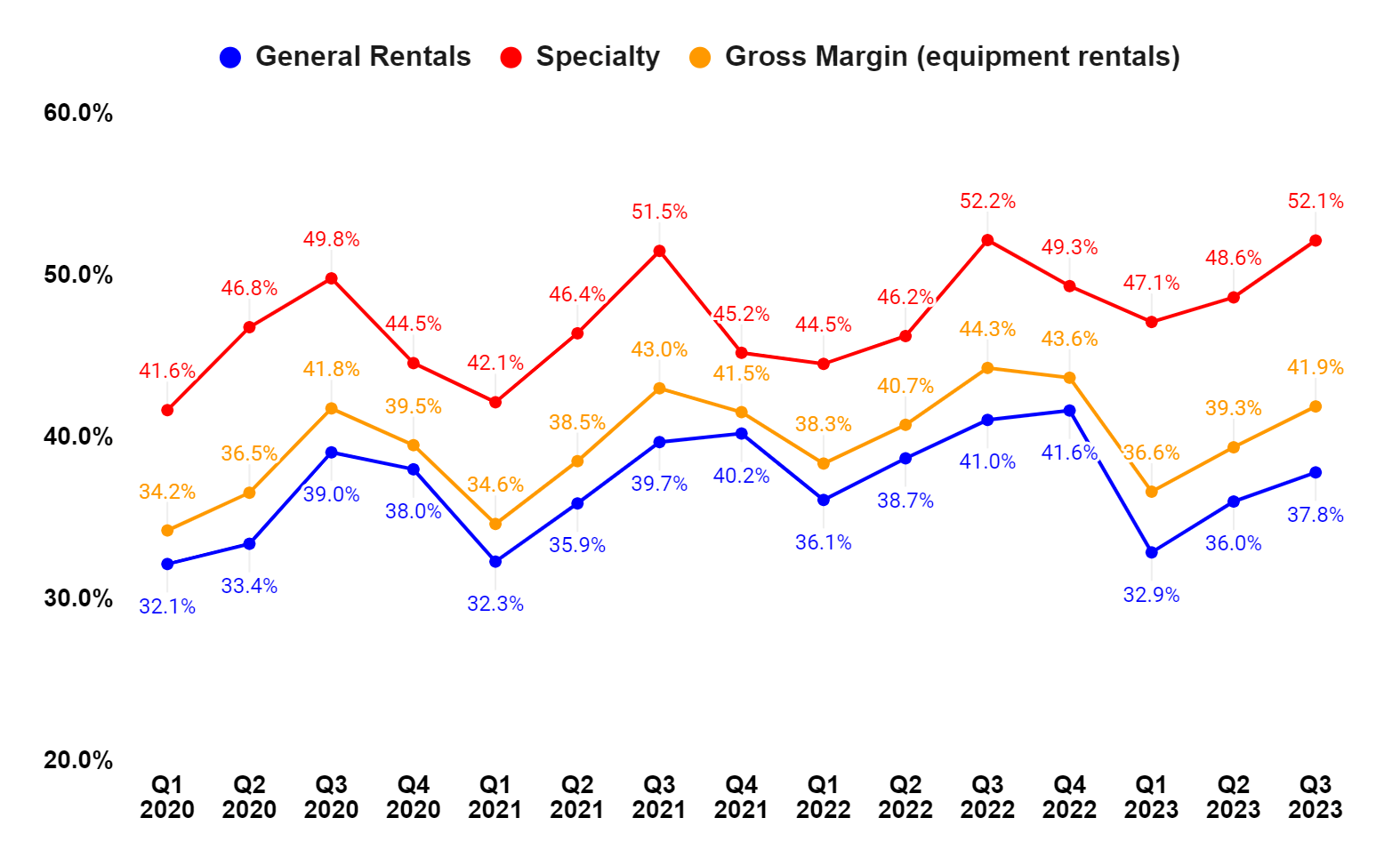

In Q3 2023, the general rentals segment’s gross margin (for equipment rentals) declined 320 bps Y/Y due to the impact of higher depreciation expense related to the Ahern Rentals acquisition while the specialty segment’s equipment rentals gross margin remained flat Y/Y. Total equipment rentals gross margin declined 240 bps Y/Y as the result of the impact of the Ahern Rentals acquisition.

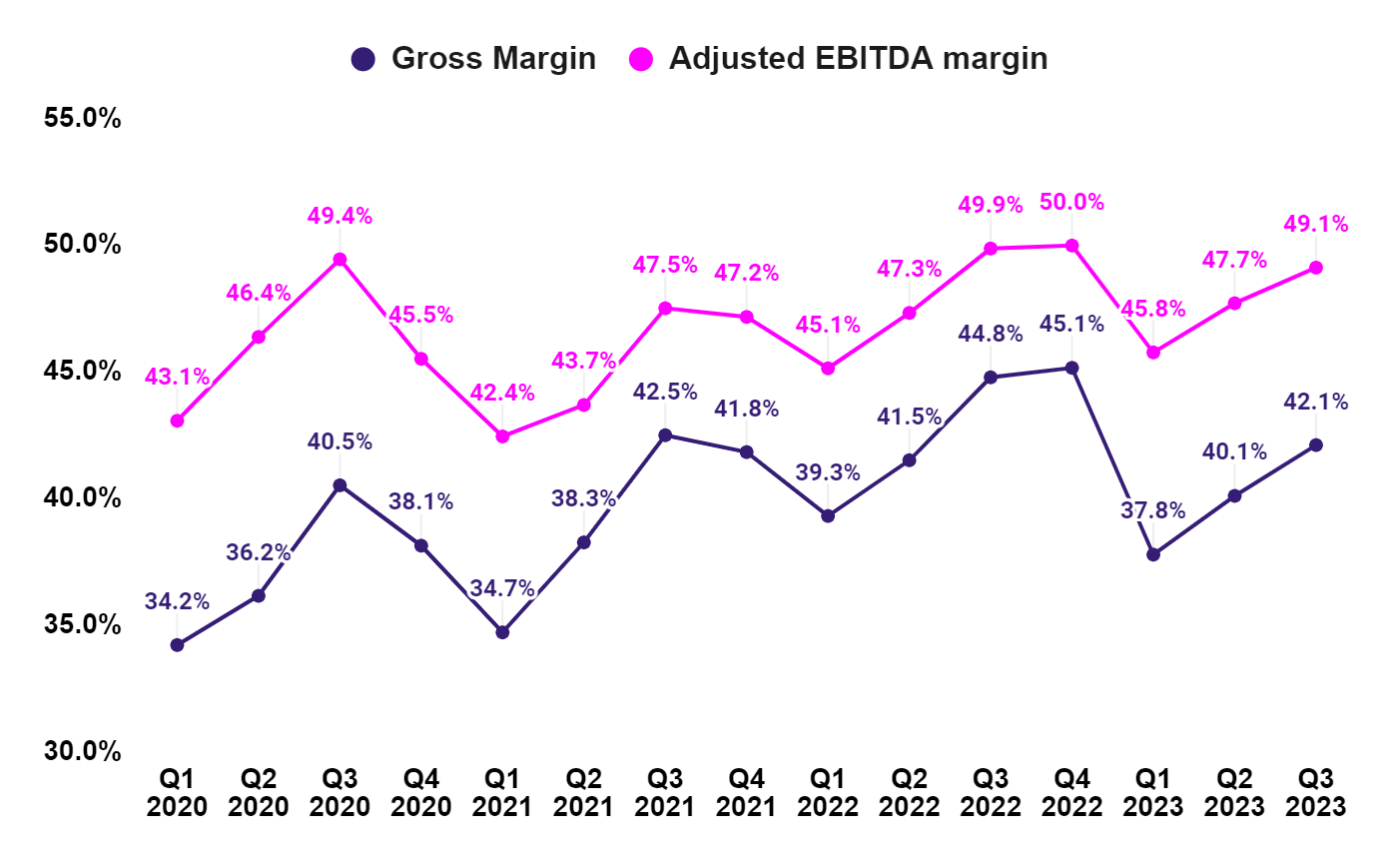

The adjusted EBITDA margin in the quarter decreased 80 bps Y/Y to 49.1% as the 270 bps Y/Y contraction in total gross margin more than offset the reduced SG&A expense as a percentage of revenue.

URI’s Segment Wise Gross margin (Equipment Rentals) (Company Data, GS Analytics Research)

URI’s Consolidated Gross margin and Adjusted EBITDA margin (Company Data, GS Analytics Research)

Looking forward, the company’s margins should improve as it progresses with Ahern integration and optimize the combined branch network and fleet, which is expected to be completed by the year-end. Further, the company should benefit from operating leverage as the sales outlook is positive. The company is also focused on driving operational efficiency through lean management techniques including Kaizen processes and technology investments such as telematics and Field Automation System & Technologies (FAST) which should help margins in the long run. Lastly, the company’s margin should also benefit from a mix shift toward higher-margin Specialty business which is growing at a faster pace than General Rental business.

Valuation and Conclusion

URI is currently trading at 9.68x FY23 consensus EPS estimates and 9.25x FY24 consensus EPS estimates, which is at a discount versus the company’s average forward P/E of 10.82x over the last 5 years.

The company has good near as well as long-term revenue growth prospects driven by secular growth prospects such as the return of manufacturing to North America, investments in the energy and power sector, U.S. infrastructure spending and other government stimulus, ongoing shift from ownership to renting equipment, sustained demand for specialty solutions and accretive M&As. The company’s margin should also benefit from synergy from the integration of Ahern Rentals, sales leverage, increased operating efficiencies, and mix improvement. These promising growth prospects coupled with lower-than-historical valuation make URI’s stock a buy.