Ales_Utovko/iStock via Getty Images

Electrovaya Inc. (NASDAQ:ELVA) has delivered two consecutive quarters of positive EBITDA; it has reached profitability ahead of schedule thanks to a 100% growth in revenue and a 3% increase in gross margins. Electrovaya has had the best year in its history, extending and improving the contract with its biggest customer, Raymond Toyota, adding a second large OEM customer on the same improved terms and releasing a new High Voltage battery product that may add another high-margin product line to its existing market-leading materials handling product.

Electrovaya has just completed the best quarter in its 20-year history. Still, its share price has not tracked the improvement in the company, and a recent drop of more than 50% following Electrovaya's uplisting to the Nasdaq makes Electrovaya a potential multi-bagger with price targets from separate sources expecting returns in the hundreds of percent.

Electrovaya is now a profitable company with a technological moat providing a significant and sustainable competitive advantage. Electrovaya's lead product is the Infinity Battery Platform, which uses a proprietary patent-protected ceramic separator that increases the safety profile of lithium-ion batteries while providing a dramatically improved lifetime. The infinity system works with different Anode and Cathode chemistry and has been in the field for more than five years, and the batteries have shown almost zero degradation. I discussed the technology in detail in my first Electrovaya article in May 2022. That article covered the technical details of the batteries and the deal with Raymond Toyota. For a full technical explanation or to read the published white paper comparing the battery to its competition, please refer to the earlier article.

In my second article on Electrovaya, I discussed in detail the mathematical model I built for Electrovaya that forecast sales of $42 million in 2023, a massive 100% increase in revenue. The model predicted a net profit in 2024 and gave a more than 400% valuation above the current share price.

Electrovaya is not a complicated business to model; it makes batteries and sells them to large OEM customers; those customers have minimum order quantities on their contracts and receive exclusivity as an incentive to meet the minimums. The image below shows some key line items from the model; the inputs to the model were covered in the earlier article.

Line Items (Author Model)

In this article, I will look at Electrovaya's progress this year measured against my model and consider what we can expect over the next two years.

The progress: It's all about profits

The fundamental forecast was the massive growth in revenue from 2022 to 2023. The actual 2023 revenue figures (although still unaudited) have come in at $42.2 million. It's almost exactly as forecast.

The big change was that Electrovaya has brought this revenue in at a profit, twelve months ahead of my target; they have delivered positive EBITDA in two consecutive quarters, and the CEO said they never intend to return to a loss-making situation.

The model expected a positive EBITDA next year for the first time; however, the Q3 results showed EBITDA was +$1.1 million in Q3 2023, up from -$0.6million in Q3 2022, and this resulted in a net profit of $0.1 million in the nine months to June (-$3.2 2022). Electrovaya guided to continued net profits and positive EBITDA in Q4. The recent press release of preliminary Q4 unaudited accounts confirmed the sales volume for the year. Still, we must await the audited statements to confirm the profit figure.

On the cost side, R&D has fallen more than 25%, and finance costs are lower than expected, 17% less than in 2022. (Q3 2023)

The early profitability is due to increased margins ( 28%, up from 25%) and decreased costs.

Management will provide updated 2024 guidance when they publish their audited results for 2023 but have said they expect strong growth to continue. For now, I will stick with my forecast of $67 million in revenue and a positive EBITDA of $4 million. The recent increase in OEM customers (see below), improved profit margins, and reduced costs mean that I will likely have to increase both of these forecasts when we get the audited accounts. It is more than likely that Electrovaya will continue its 100% CAGR for the next year or two.

Revenue

The Electrovaya business is a high margin, high profit, and fast-growing.

In a nutshell, Electrovaya sells lithium-ion batteries to forklift truck operators. Its technical advantages make it a premium high-margin product. The product offers increased safety and lower total cost of ownership due to its increased life cycle and improved degradation.

Electric Forklifts are a mature market and have operated for many years. Buyers are aware of the problems around battery safety, longevity, and total cost of ownership. As such, it was a relatively easy sell for Electrovaya; they have the safest battery, offering an increased life cycle and a lower total cost of ownership. As they keep saying, the life of a battery improves by a factor of 5.

Electrovaya Batteries have been in this field for 5 years and are showing almost zero loss in performance (CEO Fireside Chat Water Tower). It is a unique system that will make Electrovaya very difficult to displace from the heavy-duty use markets. The materials handling business at Electrovaya goes from strength to strength with an additional large OEM customer.

Toyota signed again

The original Raymond Toyota, the basis of my initial bullish call, has been renewed until 2026 with higher minimum purchase requirements and higher prices.

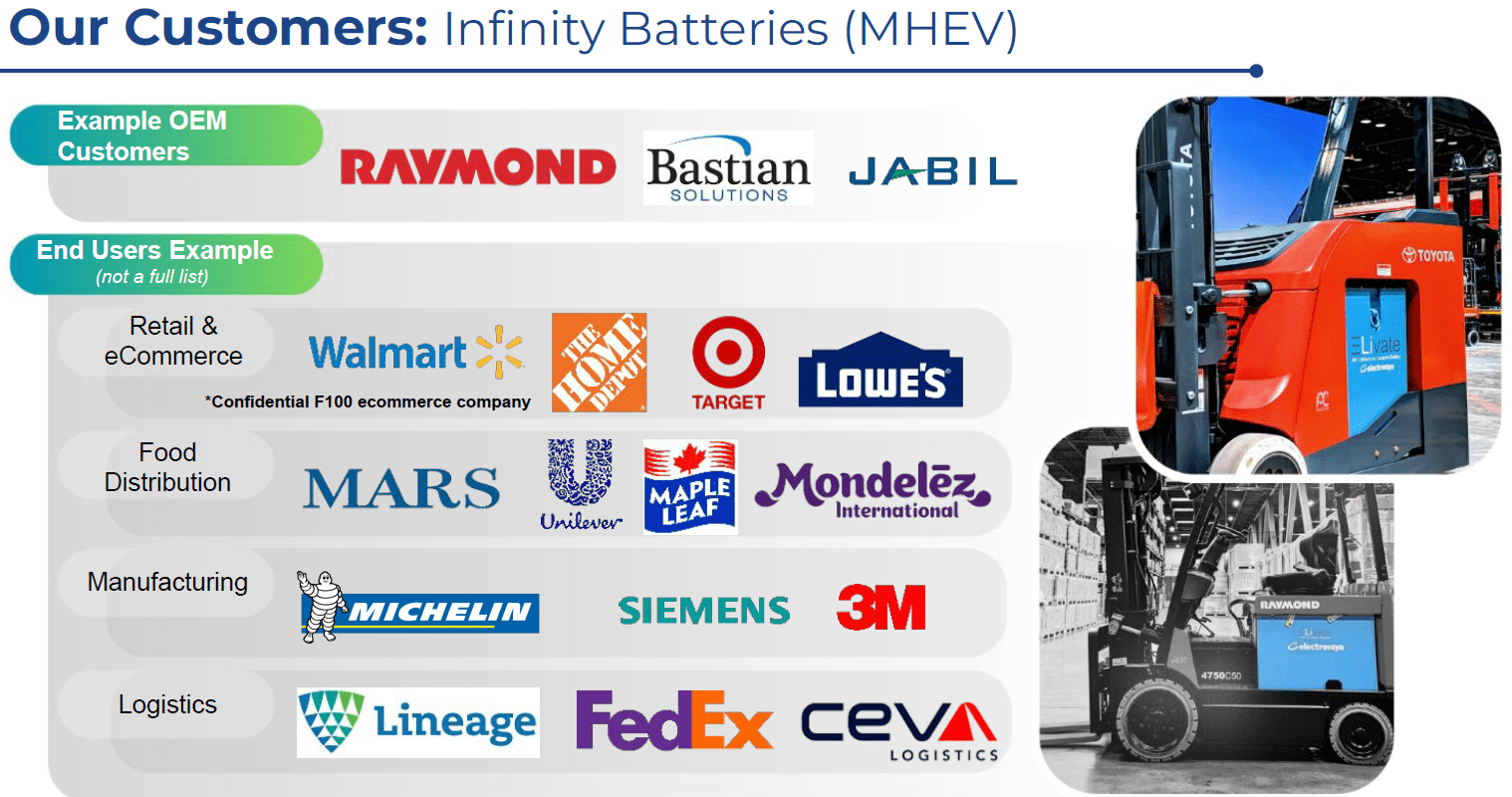

On November 2, a press release confirmed the new deal with Raymond Toyota and a new OEM partner. In the press release, the CEO stated that the battery was used in 170 warehouses owned by 12 Fortune 100 companies. In 2023, they delivered $36 million of products through their single OEM (out of the $42 million total). In 2024, they will have a second large OEM and are both signed up for three years.

I think the second OEM is likely Bastion, another Toyota-owned material handling supplier that serves some of the largest firms in Europe with highly automated stock handling systems. Electrovaya does have a third OEM, Jabil (JBL), the diverse American electronic equipment manufacturer with operations in 30 countries.

One of the concerns I had in my first article was that Raymond had one end user buying the batteries. Things have come a long way, Page 13 of the investor slide show (October 2023) shows a list of high-profile large users with huge material handling fleets that will be customers for many years as they transform each of their distribution sites to Electrovaya.

The first end user is now using Electrovaya equipment in 15 of its facilities; the last time I wrote, it was only 4 facilities.

In his fireside chat with Water Tower Management, the CEO said that they now receive orders without any testing or presales discussion with this end user, dramatically shortening the sales cycle.

Electrovaya customers (Investor slide show)

Commercial markets

Electrovaya has long discussed adding additional vertical markets; it has just been talk for the last three years, but now we have movement.

In the fireside chat, the CEO spoke about commercial markets; he means heavy-duty electric vehicles. Electrovaya has targeted buses and mining trucks as a potentially high-margin additional market. In the fireside chat, the CEO said (fireside chat) that they had decided not to pursue the bus market previously due to the low prices demanded by the Bus manufacturer. He also mentioned the results of that decision and its impact on the battery companies that had decided to proceed.

Why electric buses

You do not have to search far to find many problems associated with the current electric bus fleets worldwide. Safety is a concern highlighted by the October fire in Europe and follows the incident in London last year. The Paris bus authority suspended the use of its fleet after a fire, and in Connecticut, the entire fleet was replaced with diesel engines after two fires.

Eelctrovaya's safety comes from its patented ceramic separator. Electrovaya has more than 6,000 forklift trucks using their batteries and has reported zero safety incidents in the five years they have been operational. An earlier iteration of the tech was installed in 20,000 Daimler smart cars without any reported fire incidents. (oct investor presentation slide 10)

The other concern is the battery's life; most electric buses currently have a scaled-up version of a passenger car battery. It is not the best way to do this; the CEO discussed this in his fireside chat, it is Electrovaya's view that scaling up a passenger car battery is not a safe and suitable way to provide heavy-duty electric vehicles.

The electric school bus initiative estimates that batteries will typically degrade by 20% over several years. Electrovaya batteries degrade 0% over the same period and may have a battery life of more than 25 years in this market.

Buyers of electric buses now have experience like the buyers of forklifts are aware of the issues, making them more open to the higher priced Electrovaya solution.

Why mining trucks

It is a smaller market, but the mining industry is also of particular interest; the enormous trucks used in this area will not work effectively on standard passenger car batteries; they would probably not last 6 months. These trucks burn through many diesel engines and vast amounts of diesel. They are often in remote areas, and the cost of shipping diesel to them is significant. Many mines have access to low-cost, abundant electricity, and the total cost of ownership of an electric truck could be a distinct selling point. The longevity and power of the Electrovaya product might offer a significant advantage here, and again, they would be difficult to displace as no other battery can currently provide Infinity's proven safety profile and lifecycle.

Product growth

The current Infinity batteries are not ideal for the identified commercial applications; a higher voltage version is required, and in June this year, Electrovaya released a high-voltage version of its Infinity platform.

Pre-production units will ship this year to the heavy-duty vehicle applications market. It is a new market with customers not used to buying electric vehicles, so the sales cycle will likely be extended. I would not expect to see any significant volume sales before 2025.

The new high-voltage product comes in two scalable variants that offer a 25-year lifespan for single-cycle per-day applications. They are 35kWh and 70 kWh available for 400v and 800v applications. The batteries are modular and designed to be scaled to fit different use cases. New production equipment has been installed in Canada to meet demand.

Manufacturing

Improved efficiency in the Canadian manufacturing site is mainly responsible for the improved margins. They have doubled output but are still running a single shift without overtime, and the CEO says they have the capacity at this facility to cover 2024 planned growth. In a recent press release, the CEO said the Canadian site can now produce $130 million of battery systems.

Further improvements are possible by introducing greater automation and adding additional equipment. Electrovaya has been, throughout its lifetime, excellent at gaining government help when it upgrades and expands, and it has applied to the Canadian government for funding to support future upgrades and improvements.

The expansion is not just in equipment; engineering staff will increase by 50% this year, with most of the positions already filled. The new team will help with Electrovaya's ambitious plans in the new markets.

US manufacturing

In April, Electrovaya confirmed plans to develop a 137,000 sq ft manufacturing site in Jamestown, New York.

The New York facility is not necessary to meet current demand or the projected demand through to 2025. The CEO implied (fireside chat) that they will not need production from it until 2026, being able to cover the increase with a second shift and overtime at the Canadian facility

The August 2023 press release stated that construction work had not begun. It has an estimated Capex of $48 million, and the CEO said (fireside chat) he expects to fund this with "friendly debt." This probably means using the US government IRA to source funds; the CEO had said that access to the IRA was a key reason for the New York site. A term sheet has been signed for 80% of the construction costs with a government-backed lender.

Electrovaya expects $45 million of funding for every 1GWh of plant output on top of the $10 million local jurisdictions have already awarded for the site's development. It does not expect to begin Cell production at the area until the second quarter of 2025.

Solid state batteries

The R&D continues in this area, and I covered the state of play in my first article. No significant news regarding its progress; the company is clearly focused on the infinity platform and the new HV versions.

But it is still a MicroCap

Electrovaya has made excellent progress, making the risk/reward equation attractive. However, that partly reflects the high potential reward should everything play out in the way I have suggested.

The risks associated with this company are still considerable; it has just become profitable and relies on the cash it generates to fund its business. If customers did not pay on time, Electrovaya would run out of money quickly; it has less than one month of operational cash on its balance sheet, which is far from ideal.

Operationally, two significant risks remain; the New York manufacturing site represents two years of ongoing capex in the region of $50 million. That will have to be funded by debts and grants as they do not currently generate enough cash; the grants and debts have been applied for, but it is not all finalized yet.

The new HV battery has not reached customers yet. It is an enormous opportunity, but it is very early days to access its commercial potential.

Finally, the technical moat, Raymond Toyota, is committed to this tech, as are the prominent end users they supply. The Infinity system has proven to be the best currently available, but we all understand the speed of technical innovation in this space. If a new, better tech arrived, it could undermine the company.

Finances

In my first article on Electrovaya in May 2022, they had negative equity of over $5 million and debts of $13 million. Today, they have positive equity of $6 million and debts of $16 million; this is an enormous turnaround from the equity low of -$16 million in 2020.

The balance sheet is much improved but remains under pressure, finance costs are down, and the astronomically high-interest rates paid on the debt highlighted in my first article appear to be a thing of the past. The working capital credit line is moving to a major bank, increasing in size but at a materially lower interest rate (fireside chat). The company is generating cash and expects to continue to do so; what seemed like a never-ending cash burn halted in 2023. At the beginning of the year, Electrovaya was losing money and had less than one month of cash on the balance sheet. For the first time in the three years I have been covering Electrovaya, they appear to have sufficient liquidity to cover the next quarter's activity (although this liquidity does depend on the $10 million of accounts receivable).

Price targets

Electrovaya is now listed on the Nasdaq and has Wall Street coverage. Wall street has three strong buys, and one buy with an average price target of $10.50. That's more than a 200% upside from current prices. (seeking alpha)

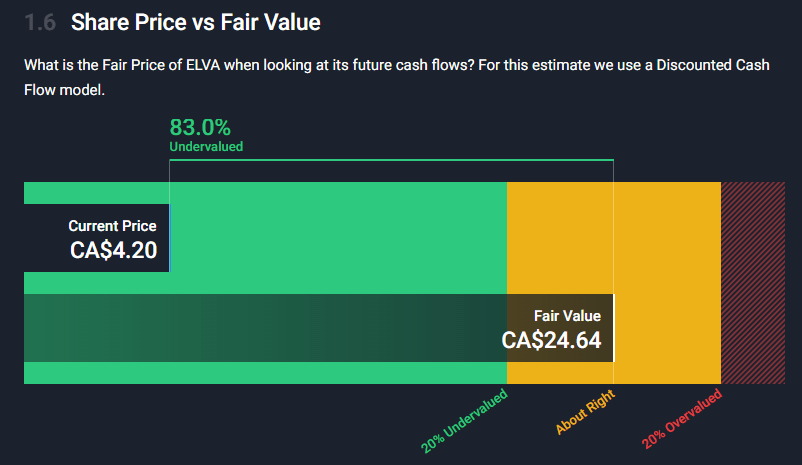

Taking account of the 5 for 1 share swap initiated before the Nasdaq uplifting, my model predicts between $16 and $26 per share.

Simplywall.st provides a $24.64 target using a similar discounted cash flow method to my model.

Fair value (Simplywall.st)

Conclusion

It has been a fantastic year for Electrovaya; it upgraded to the Nasdaq and picked up 4 Wall Street Analysts, all of whom are very positive.

Revenue increased by over 100%, and the company hit profitability a year earlier than expected.

Efficiency has improved enormously, and Electrovaya can now produce more than $130 million of battery products from its current manufacturing facility, allowing for a further 300% increase in revenue.

Its main customers, accounting for 90% of revenue, have signed new, more extended contracts with increased prices and minimum purchase amounts. One extra significant OEM has been added with the same terms, and as a result, we could be looking at another 100% revenue increase in 2024 rather than the 50% increase I forecasted earlier in the year.

A new High Voltage product was announced and will ship later this year. It is well suited to the heavy-duty mining and bus industries.

The price of Electrovaya shares is low and looks primed for a 100% increase in relatively short order.