jetcityimage

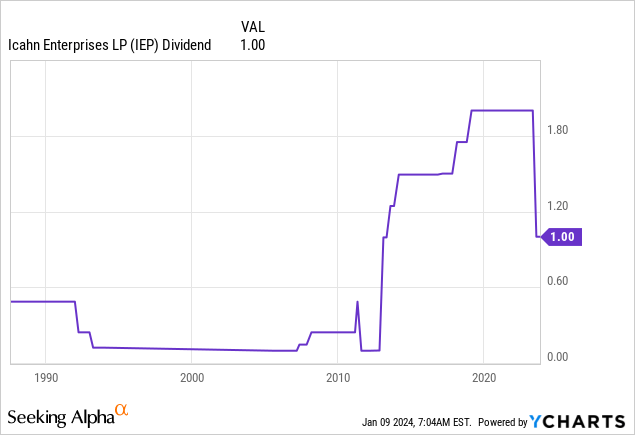

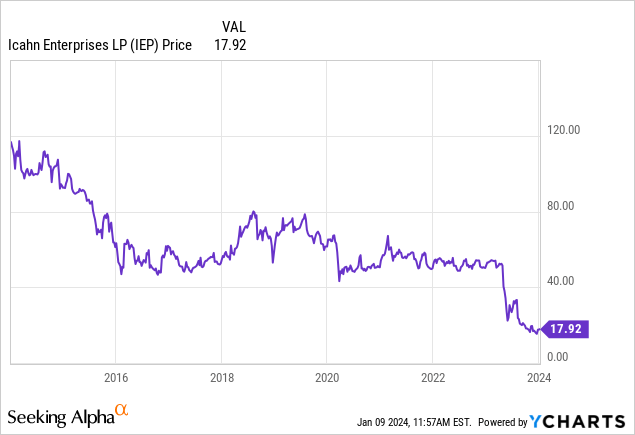

Icahn Enterprises (NASDAQ:IEP) is a shadow of its former self; the quarterly distribution has been halved with no clear pathway to recovery, its market cap is down 66% from a year ago, and a public stock portfolio broadly tilted towards hydrocarbon is in the middle of a comedown from the 2022 surge induced by Russia's invasion of Ukraine. The outlook seems bleak with IEP's units currently trading with no general direction and failing to participate in the broad market rally sparked by the Fed's dovish December meeting. However, there's now significant temptation to take a position here with a view of locking in a lower cost basis that's set within a substantial distribution rate. IEP last declared a quarterly distribution of $1 per unit. This meant a 22.1% yield. The units are down since I last covered them to discuss the aftermath of the bearish report. IEP was rated as a hold and sentiment has remained low since then. There is a need to assess whether this sentiment can recover.

Icahn Enterprises November 2023 Investor Presentation

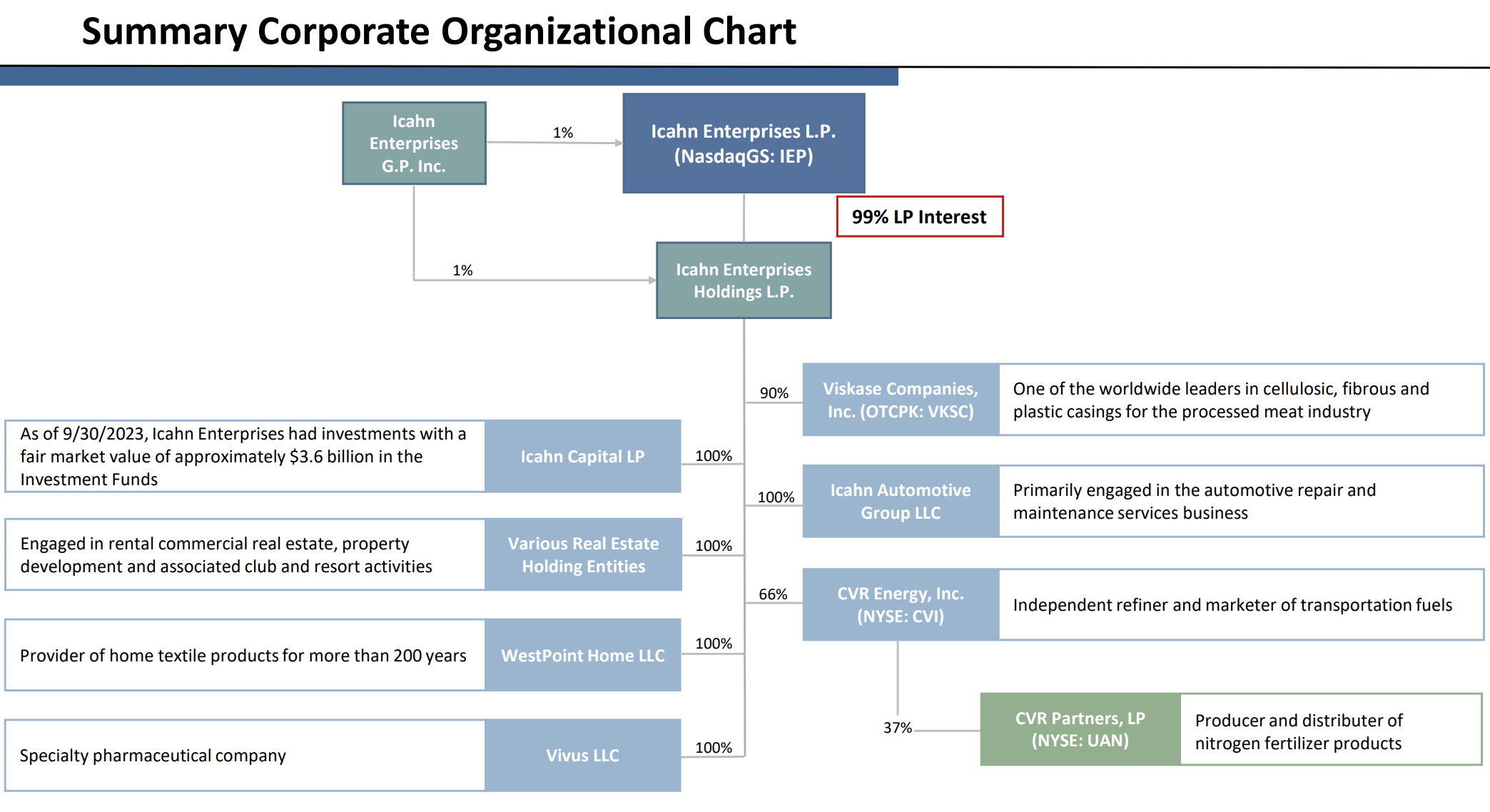

The master limited partnership ("MLP") is a diversified holding company with interests spanning Pharma, Real Estate, Energy, Food Packaging, Home Fashion, Investment, and Automotive. Broad diversification should mean lower earnings volatility but historical earnings have shown the opposite with swings in net income, free cash burn, and gains or losses on the sale of investments.

Icahn Enterprises November 2023 Investor Presentation

There is some value here against a fat double-digit yield that would mean it would take just 4.5 years to pay back an initial principal investment. The safety of the current distribution should form the core investment factor here and IEP has a history of net losses and free cash burn. Carl Icahn owns 85% of IEP's outstanding depositary units and serves as the Chairman of the Board so there's material alignment with unitholders.

How Safe Is The 22% Yield?

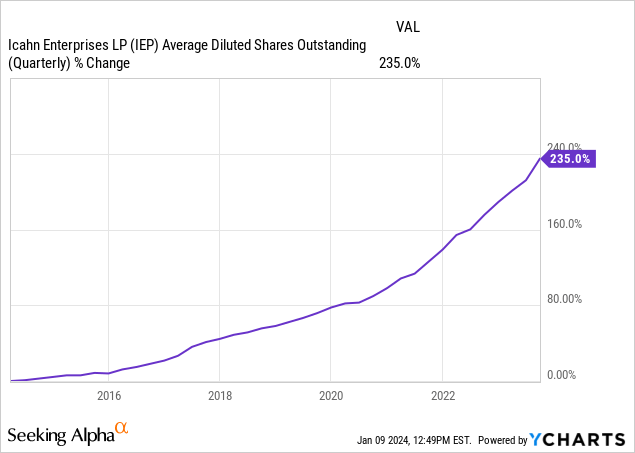

MLPs are essentially tax sheltered investment vehicles whose investors' primary focus is income. There is simply no other reason to own IEP apart from its quarterly distributions with the price returns of the units over the last decade a reflection of a policy to pay out unitholders from the issuance of new units. IEP's unit price even before the short-induced collapse had broadly been dipping on a sustained and perpetual basis. Why? Dilution.

The MLP has been issuing new units, with this ballooning materially over the last decade by 235% to 394,000,0000 units at the end of the third quarter of its fiscal 2023. This means a roughly 23.5% annual rate of dilution, a trend that was used to support the dividend payments. New LP units at the end of the third quarter were up 21.6% over their year-ago comp. Critically, a lower unit price reduces the efficacy of this strategy to support dividend payments.

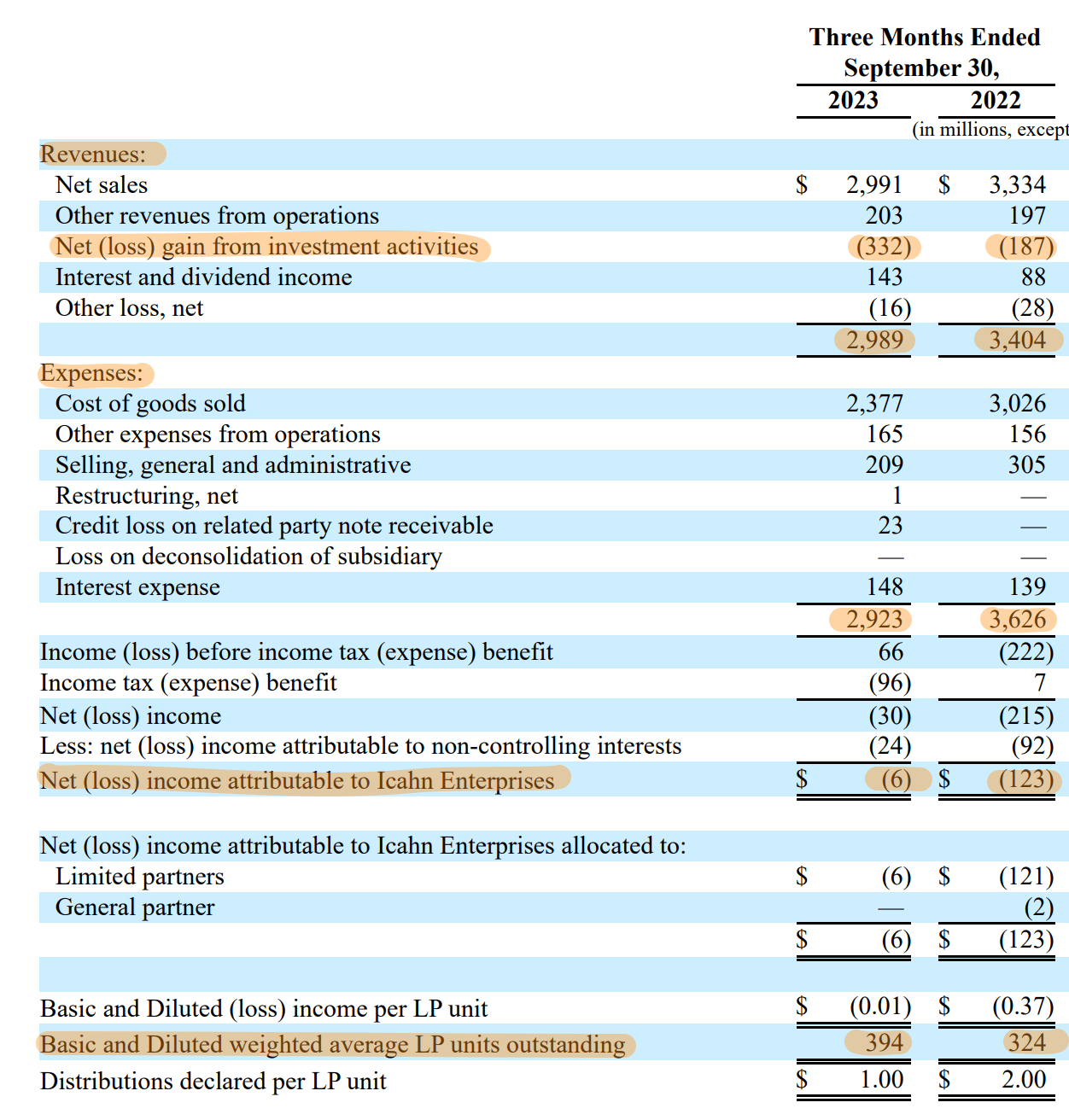

Hence, the outlook for a recovery of the dividend to the prior level is incredibly dark. The MLP recorded revenue of $3 billion for the third quarter, a dip of 10.3% year-over-year with a net loss of $6 million recorded. Net loss was a material improvement from a loss of $123 million in the year-ago period. Overall, the third quarter meant continued unprofitability with a dip in revenue and a net loss of $332 million from investment activities, up from a loss of $187 million in the year-ago period.

Icahn Enterprises L.P. Fiscal 2023 Third Quarter Form 10-Q

IEP has spent $241 million over the last 9 months paying out dividends, at odds with operations that are losing money. This inherent mismatch does not inspire confidence in the current distribution even though another cut would be disastrous and is currently deemed unlikely as it would spark another intense selloff of the units.

Net Asset Value And Activism

Icahn Enterprises November 2023 Investor Presentation

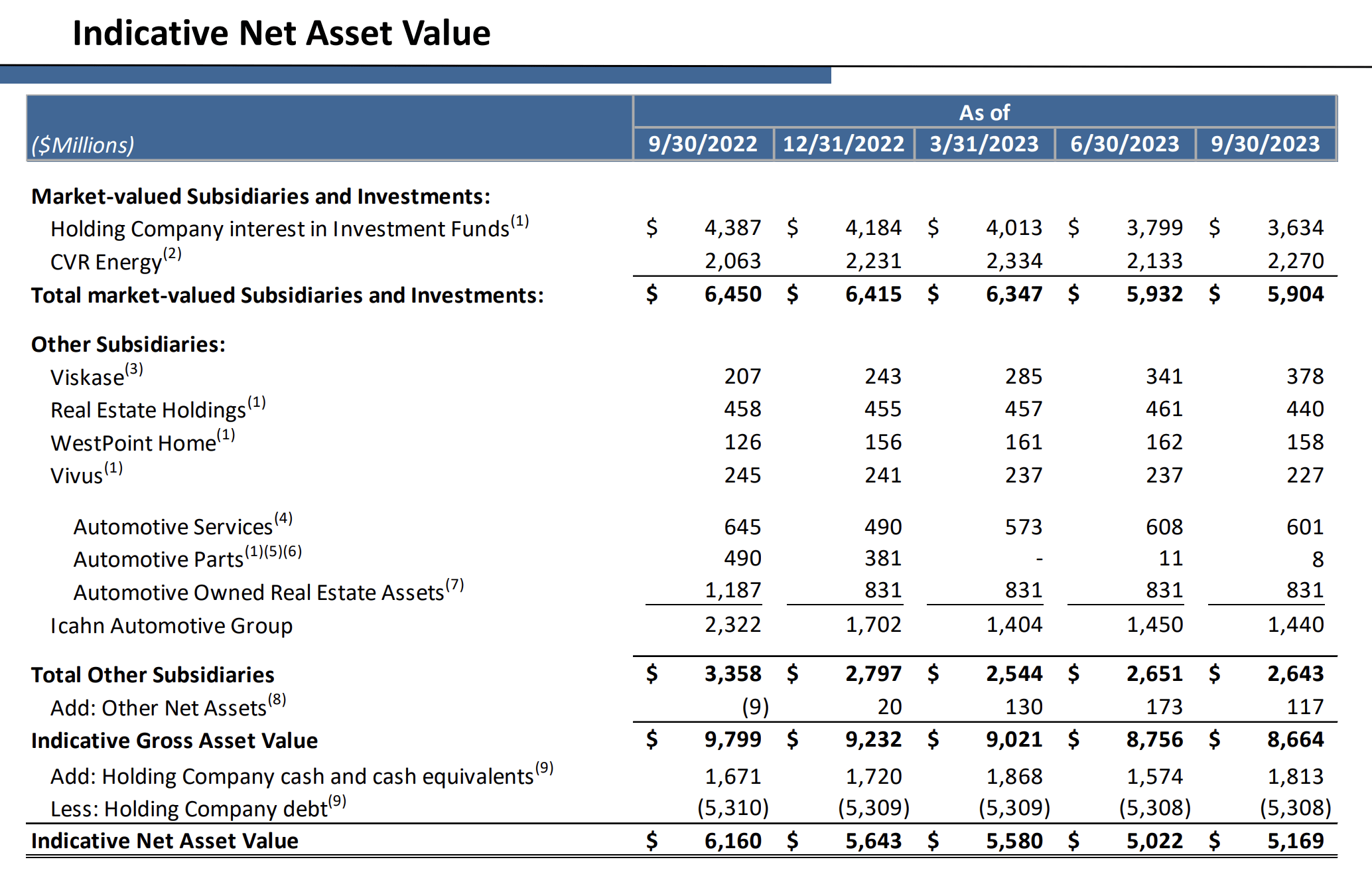

Further, IEP's net asset value at $5.17 billion at the end of the third quarter means it's currently trading at a 43% premium to NAV with its market cap at $7.4 billion. Shareholders are paying this much over NAV as the dividend yield would stand at roughly 39.1% if the market cap were to directly reflect NAV. This would be a roughly 2.56-year payback period.

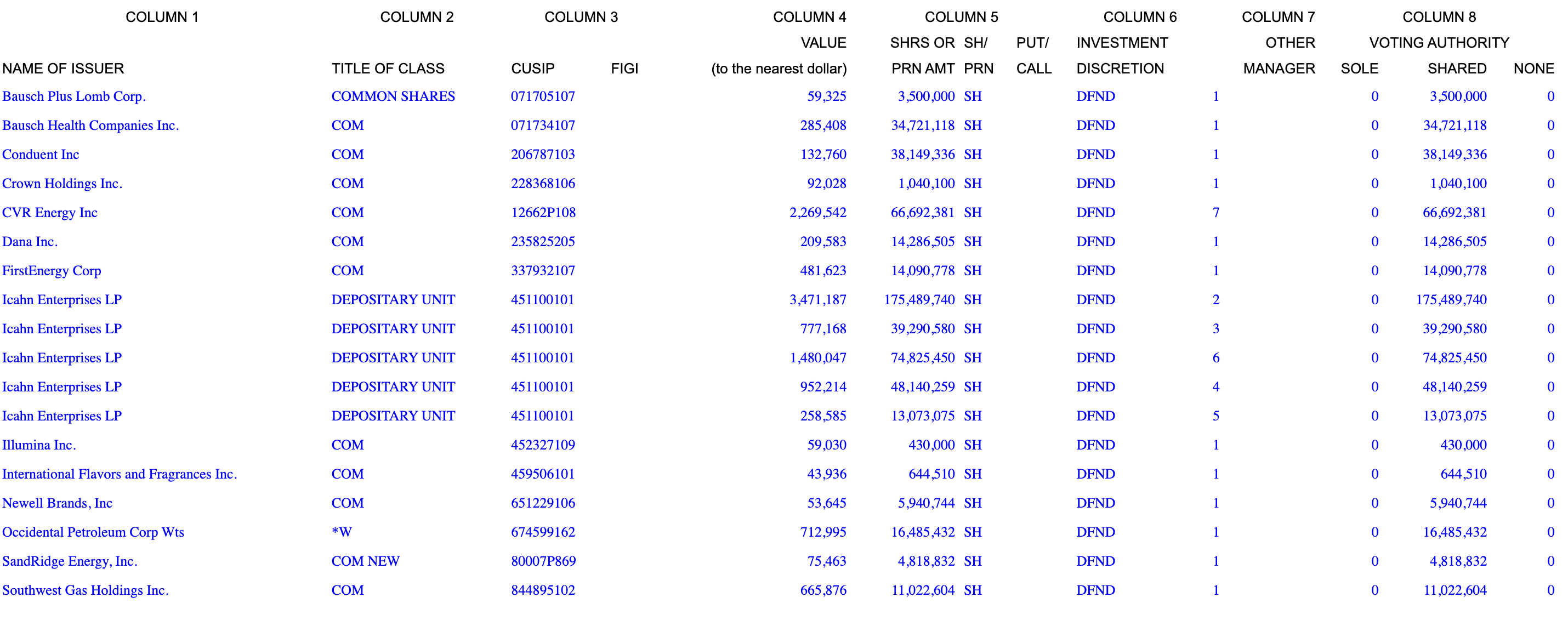

Icahn Enterprises L.P. Fiscal 2023 Third Quarter Form 13F

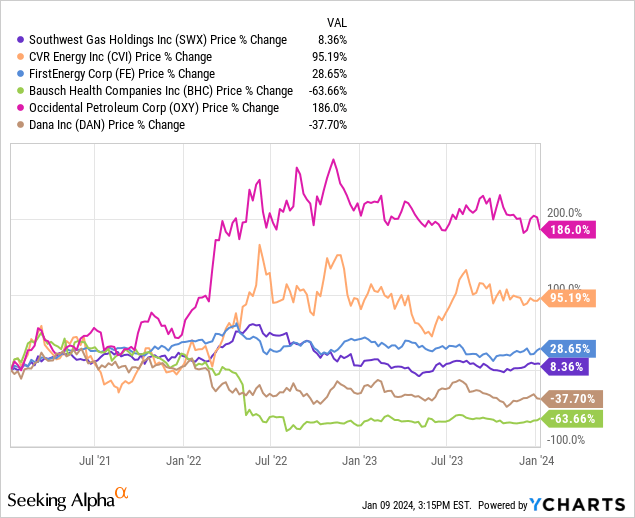

CVR Energy (CVI) is one of IEP's largest positions from its 13F filing. The company is focused on renewable biodiesel and has performed well, up 9% over the last 1 year and by 29% over the last 5 years. IEP also owns warrants in the oil and gas company Occidental Petroleum (OXY). OXY has also performed extremely well but has been countered by IEP losses on Bausch Health (BHC) and other positions.

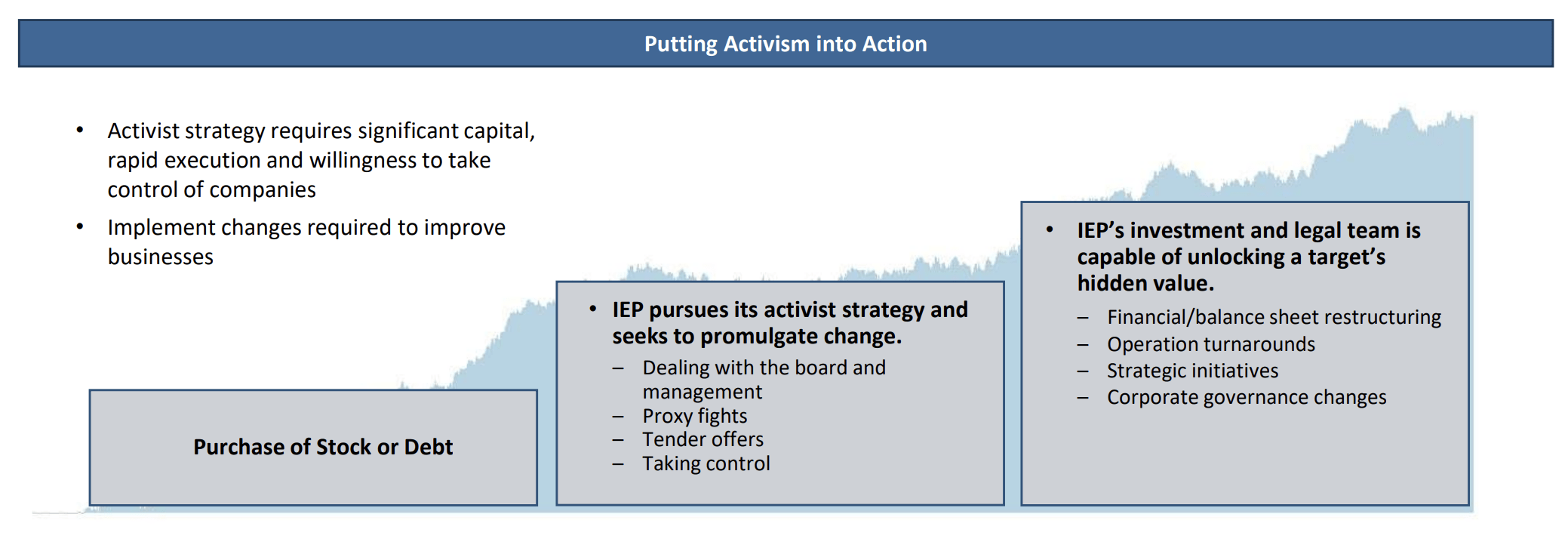

Carl Icahn has stated that he's not a buy-and-hold forever investor, differing from the strategy pursued by Warren Buffett's Berkshire Hathaway (BRK.A). His investment philosophy is built around "Putting Activism into Action" with IEP buying undervalued companies and pursuing initiatives including board changes to unlock shareholder value.

Icahn Enterprises November 2023 Investor Presentation

Overall, I'm not attracted to the portfolio or the operating structure of IEP. The individual position in companies like OXY or CVI can just be bought directly without the uncertainty that comes with the current distributions. The units remain a hold for existing shareholders.