VioletaStoimenova

Introduction

Essential Properties (NYSE:EPRT) is now one of my favorite REITs because it is growing rapidly while its share price has not moved much in recent years. In addition, EPRT offers strong growth, favorable tenant metrics and good diversification, and has a strong balance sheet.

I first published about Essential Properties in September 2021 and gave it a hold rating. What I like about Essential Properties is that they lease their properties to service-oriented tenants. These businesses are needed in society and therefore provide stable income that makes rent more secure.

Since 2021, their property allocation has changed somewhat. The allocation is now slightly more driven toward experience-oriented tenants.

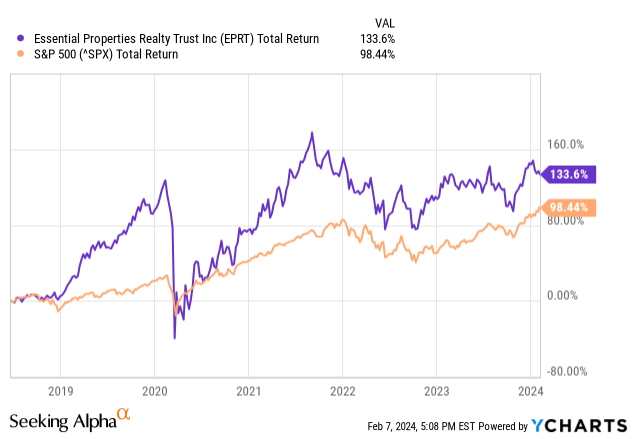

The stock's total return since 2021 is a loss of about 16%, while Essential Properties continued to grow strongly. However, long-term investors have outperformed the S&P 500.

The market seems dissatisfied with REITs in general as interest rates have risen sharply to cope with high inflation. Right now, the buying opportunity is attractive because the Fed wants to cut interest rates this year.

Furthermore, Essential Properties has many characteristics that make it an interesting investment:

- Good portfolio diversification and metrics.

- Strong balance sheet.

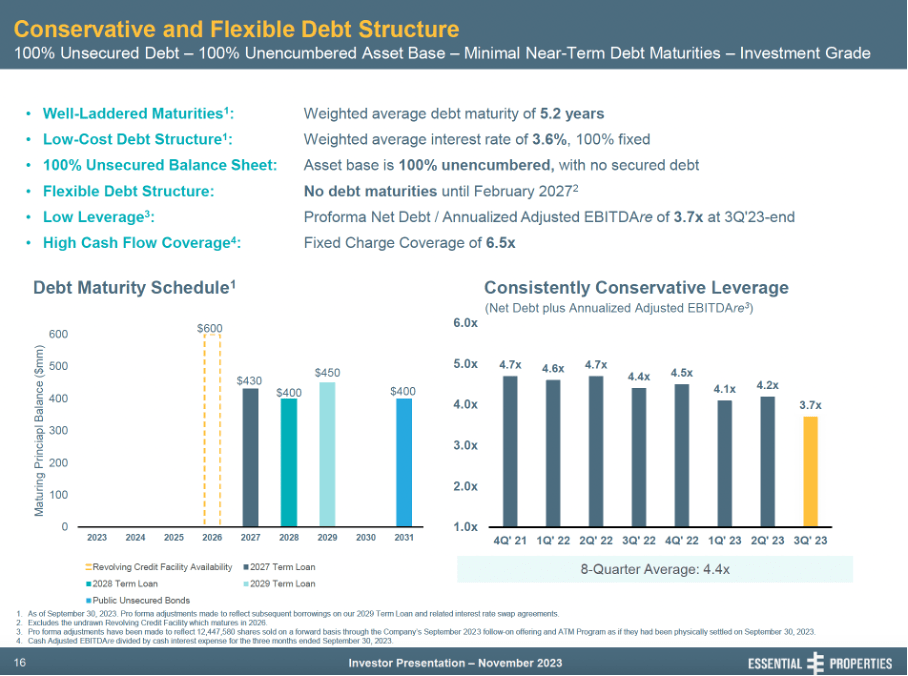

- Favorable debt maturities (first one is in 2027!).

- Favorable valuation metrics and dividend yield.

The maturities of the debt are very favorable because the Fed intends to continue to lower interest rates in the coming years. The first major repayment will take place in 2027, and interest rates are expected to fall sharply by 2027. Refinancing is then very favorable for Essential Properties.

Portfolio holdings, Metrics and Liquidity

Essential Properties is a safe investment because it’s a safe tripe net lease play just like Realty Income (O). Property taxes, insurance, and maintenance is paid by the tenants. Essential Properties is much smaller in size then Realty Income as its 2023e revenue is $355M compared to $3.8B for Realty Income.

Essential Properties will announce their results for the fourth quarter of 2023 on February 14. And I am curious about their portfolio allocation and the financial health of their tenants. In recent years, Essential Properties has been receiving more rent from car washes and I’m curious to see if this trend continues. With Q3 2023 results, I can compare it to its historical portfolio in 2021.

Essential Properties has a strong real estate portfolio with financially sound tenants. Its shift in diversification is not worrisome as still 78.9% of its tenants operate in the service industry (down from 84.5% in Q2 2021 when I first published my article). The experience industry now brings in more revenue, especially entertainment. I see this an increased risk, but still manageable as it brings in only 8.3% of cash ABR.

Top 10 Tenant Concentration (Essential Properties 3Q23 Investor Presentation)

From the Investor Presentation of now and 2021, we see that cash ABR income from car washes and entertainment has increased significantly over the past two years. However, unit-level rental coverage is more than adequate at 4.0x and no cause for concern. I hope this trend does not continue as car wash ABR already account for over 15.3% of total ABR.

Essential Properties' lease metrics are strong. 99.8% of the properties are leased, of which 65.1% are master leases. And the weighted average remaining lease term is 13.9 years, providing a lot of certainty.

96.1% of all leases are escalated on a contractual fixed rate basis, and only 2.5% are escalated due to increases in the CPI. In my opinion, this poses a risk if inflation remains high for a long time. In that case, the combination of increased interest rates and high inflation could have a negative impact on Essential Properties' earnings.

Healthy Portfolio Metrics

Their portfolio metrics have improved strongly. More than 74.1% of cash ABR has a unit-level coverage ratio of more than 2.0x. At the time of my first article in 2021, this was only 56.6% of cash ABR.

And we also see this positive trend in its tenant credit ratings. In 2021, more than 8% of tenants had a credit rating of CCC+ and this has now greatly improved to just 2%. And over 40.4% of cash ABR leases expire after 2038, while in 2021 this was only 31.1%.

Tenant Credit Rate and Lease Expiration (EPRT 3Q23 Investor Presentation)

Favorable Debt Maturities

The first debt maturity occurs in 2027. The Fed intends to cut interest rates at least once this year. And its new December projections estimate that the longer-term federal funds rate will be about 2.5%. Essential Properties is therefore in a favorable position to have the opportunity to refinance their debt at a low interest rate.

With an all-time high liquidity of $990 million, Essential Properties has the ability to increase their investments to support long-term FFO growth. It has therefore ample liquidity to fund further growth.

Favorable debt maturities and conservative leverage. (EPRT 3Q23 Investor Presentation)

Valuation, Growth and Risks

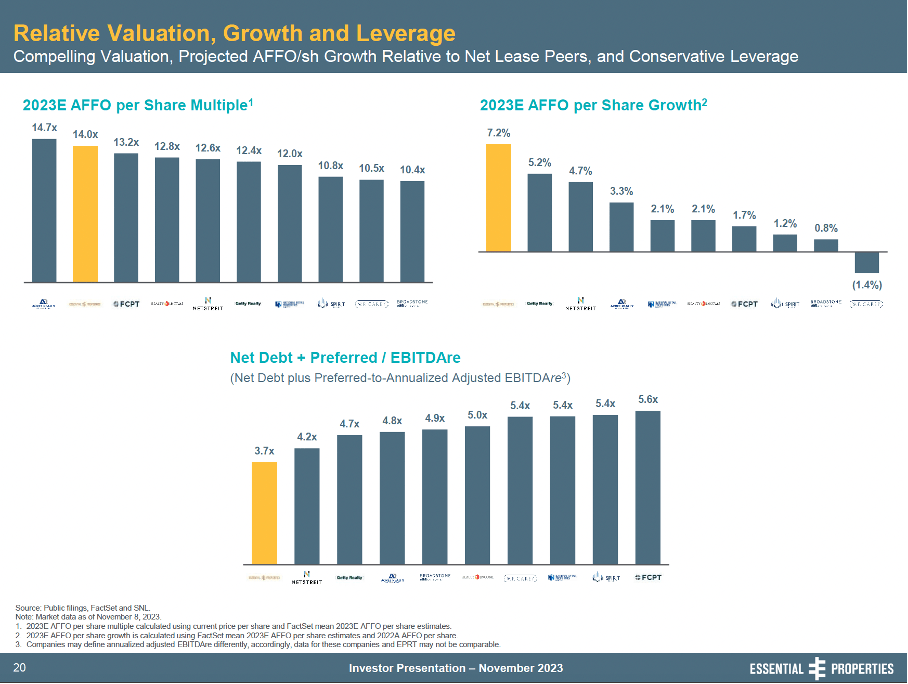

Finally, we look at the valuation metrics of Essential Properties and sector peers. Each investor presentation gives a good overview of sector peers and important metrics.

What I find important to compare are REITs that have primarily service-oriented tenants. I also want to invest in REITs with at least 2% growth in AFFO (I take 2023rd AFFO from the chart below); which gives room for dividend growth. Getty Realty (GTY), Essential Properties, NNN REIT (NNN) and Realty Income (O) stand out here.

Net debt + Preferred / EBITDAre is most favorable for Essential Properties, followed by Getty Realty, Realty Income and NNN. This allows EPRT and Getty Realty to increase debt to finance their growth.

Essential Properties and Getty Realty stand out favorably in general. The valuation metric AFFO multiple is slightly more favorable for Getty Realty than for Essential Properties (12.4x versus 14.0x). Essential Properties, on the other hand, is much safer because only 18% of its ABR consists of the top 10 tenants. For Getty Realty, this is much higher at 72% of ABR.

Valuation, Growth, and Leverage of Sector Peers (EPRT 3Q23 Investor Presentation)

Comparing these statistics, Essential Properties strikes me as one of the best Triple Net Lease REITs with mostly service-oriented tenants. Their portfolio is the most diversified and manages to grow their AFFO strongly with little leverage. This makes it one of my favorite investments in Triple Net Lease REITs. Essential Properties is therefore a worthwhile investment.