Ladislav Kubeš/iStock via Getty Images

Introduction

Nordic Semiconductor ASA (OTCPK:NDCVF) (OTCPK:NRSDY) has experienced a significant decline in its stock price since mid-2021, dropping from a high of $36 per share to now trading under $9. This downturn is attributed to justifiable concerns, yet the current valuation seems excessively pessimistic. Despite the short-term challenges posed by the current macroeconomic environment, which has led to reduced global spending and diminished the immediate demand for Bluetooth devices compared to the COVID-era, Nordic Semiconductor's sector holds substantial long-term growth potential. The semiconductor industry's cyclical nature is once again evident, with a rapid decrease in demand for Bluetooth chips. However, I am of the opinion that adopting a long-term investment perspective could unveil significant opportunities for substantial returns.

Sector Analysis: When Will It Improve?

Since the beginning of 2023, the semiconductor industry as a whole has experienced a downturn, with one notable exception: AI, which has seen significant growth. However, Nordic Semiconductor has faced considerable challenges during this period. The company primarily serves customers in the short-range wireless component market, particularly Bluetooth semiconductors. This sector experienced a surge in demand during the COVID-19 pandemic, as consumers indulged in luxury items such as headphones, high-tech refrigerators, and smartwatches. However, as inflation surged in the Western world and central banks rapidly increased interest rates to counter inflation, consumer spending decreased rapidly also.

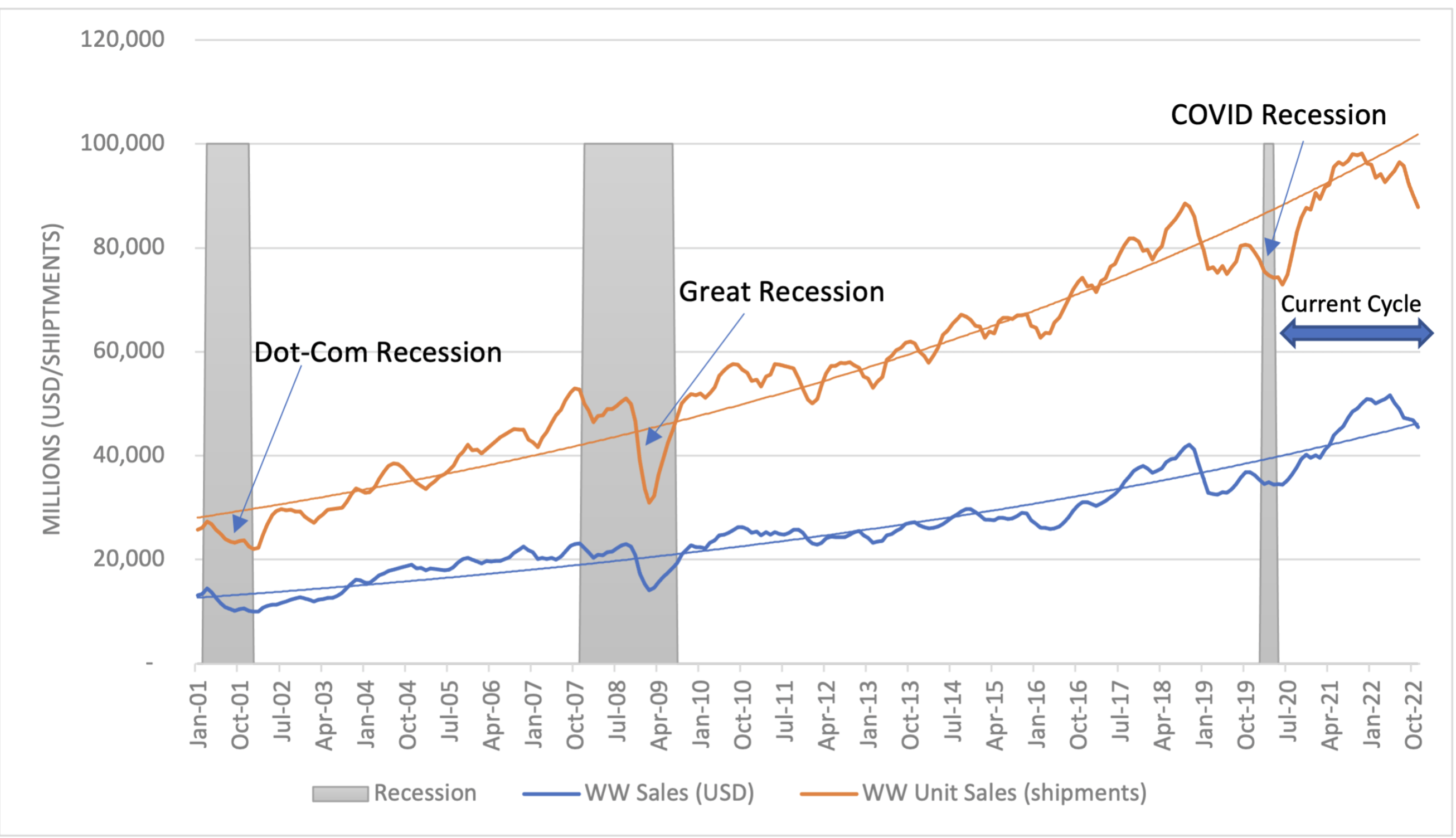

It's crucial to recognize that the semiconductor industry operates in cycles, yet what remains paramount is discerning the underlying trajectory. While temporary dips in demand are inevitable, it's essential to transcend these downturns and focus on the broader perspective. Undoubtedly, semiconductors constitute a vital component of our future. Chips are key to emerging technologies, such as AI, IoT, 6G, innovation in medical devices and our electric grid and climate solutions all rely on these tiny pieces of silicon that have become so important to our lives. And that reality will not change in the short term or the long term" - SIA.

Semiconductor's cyclical history (SIA)

Nordic Semiconductor heavily relies on the Bluetooth market to drive its revenue stream. To assess the underlying trend of this market, it's essential to examine Bluetooth's market outlook. Bluetooth has projected market estimates from 2023 to 2027, indicating growth across all sectors, particularly in location services and device networks, with expected CAGR exceeding 20% for each, respectfully. Nordic Semiconductor anticipates significant growth opportunities in these areas, as it is a prominent player. Location services encompass digital keys, personal item finding, asset tracking, and indoor navigation, while device networks include products like networked lighting control, monitoring systems, and electronic shelf labels.

Currently, Nordic Semiconductor benefits from underlying long-term trends. However, pinpointing precisely when these shifts will favor Nordic Semiconductor is challenging. Nevertheless, I would assume that a path toward lowering interest rates could bolster consumer demand, enhance consumer confidence, and stimulate the overall economy.

Company Analysis

Company Specifics

Nordic Semiconductor's main segments are separated into Short-range wireless components, which are Bluetooth and Proprietary wireless, and then we have Cellar IoT and ASIC components. Bluetooth stands for approximately 90% of all the revenue and is the main segment for Nordic Semiconductor. Therefore, I will mainly go through this part of Nordic Semiconductors business.

Nordic Semiconductor has introduced a range of semiconductors, yet to fully capitalize on them, but they have taken advantage of the current supply, preparing for future expansion. What they have done is bolstered its supply chain by securing a strategic manufacturing deal, ensuring expanded capacity to support long-term growth goals. This includes a dual source of 22nm wafers from TSMC and Global Foundries for its upcoming nRF54 Series SoCs. Additionally, Nordic has strategically boosted its inventory of 55nm wafers for the nRF52 and nRF53 Series SoCs.

Nordic Semiconductor's cutting-edge wireless solutions continue to gain global acclaim. The company's debut Wi-Fi product, the nRF7002 Wi-Fi 6 companion IC, was a finalist for the UK Elektra Awards' "Internet of Things Product of the Year." Furthermore, Nordic's industry leadership was highlighted with a nomination for the "Most Respected Public Semiconductor Company ($500 Million to $1 Billion in Annual Sales)" at the 2023 GSA Awards, underscoring its commitment to innovation. Additionally, Nordic earned the title of "India's IoT Semiconductor Company of the Year" at the Electronics Maker Best Awards 2023, a testament to its excellence in product innovation and sustainability.

Historical Performance

Evaluating companies historical performance is a key component of diving into a company. Nordic Semiconductor's prior performances have been outstanding, but the semiconductor business does include some volatility.

Nordic Semiconductor's historical performance for the years 2018 to 2022 has been outstanding, but this is where the cyclical history of this company is being displayed, when the years are good, Nordic Semiconductors shareholders are really being complimented by it.

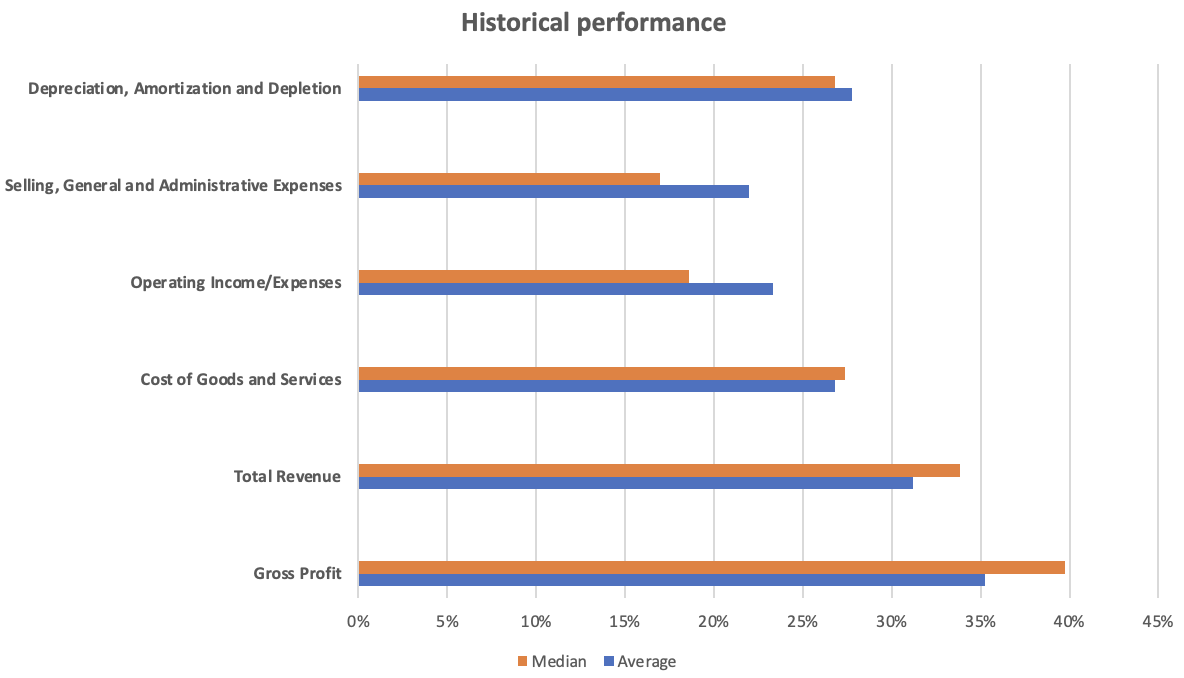

Historical financial performance (Morningstar (Nordic Semiconductor))

Reflecting on the financial trajectory, it's notable that while revenues have risen, the accompanying costs along with depreciation and amortization (D&A), and selling, general & administrative expenses (SG&A) have not escalated at an equivalent rate. This discrepancy has favorably contributed to an enhancement in profitability over time, underscoring the company's growing operational efficiency and prudent expense management. This trend is a positive indicator for the investment case, suggesting a sustainable increase in the company's value creation potential.

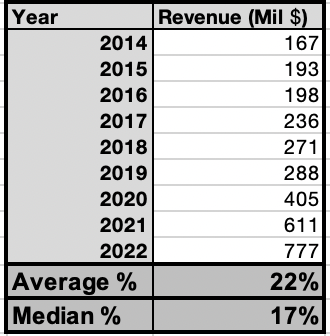

Historical revenue (Morningstar)

The historical performance from 2014 to 2022, while solid, was skewed by the exceptional growth during the 2020 to 2022 period. Over this eight-year span, the average annual revenue growth stood at 22%. However, this figure is elevated due to particularly robust expansion in the latter years. A more consistent indicator, the median annual revenue growth, was 17%, indicating a strong performance throughout the period, albeit with less variability than the average suggests.

My Perception Of Q4

NOD's guidance for Q1 2024 indicates a significant revenue decline of 48% year-over-year, which is substantially worse than the market expected. This guidance has raised concerns, especially since it significantly underperforms the anticipated market conditions, as indicated by key customers and IoT peers. Nordic Semiconductor has delayed their earnings forecasts for Q1, which is not a good sign, but for us, long-term investors. This does not really matter and could only present opportunities.

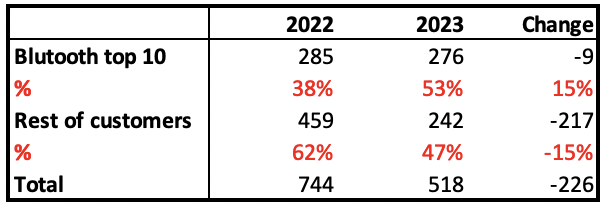

Q4 2023 revenues were below expectations, primarily due to reduced spending from non-tier-1 customers. The resilience of the top 10 Bluetooth customers suggests that major players are somewhat shielded from current market volatility and remain committed to product development despite a downturn. In contrast, the broader customer base may be more vulnerable to market downturns, higher interest rates, and inflation. This vulnerability could explain why revenues from these other customers have declined by $217 million this year compared to 2022.

Customer % (Nordic Semiconductor Q4)

What Has Nordic Semiconductor Done To Address The Ongoing Problems?

I have mentioned that they have taken advantage of the current supply situation, but the management has also done other initiatives to reduce costs and help out shareholders.

Nordic Semiconductor has been strategically focusing on cementing its leadership in markets poised for substantial long-term growth. However, faced with challenges such as declining revenues, margin pressures, and uncertain revenue forecasts, the company has recognized the necessity to adapt. This adaptation involves reallocating investments and implementing cost-cutting measures.

In the third-quarter report of 2023, Nordic announced an initiative aimed at optimizing costs. The measures undertaken include minimizing the use of external consultants, streamlining the operational framework, and evaluating the essential resources needed to sustain the company's primary research and development programs. By the fourth quarter of 2023, Nordic managed to decrease its workforce and the number of full-time consultants by approximately 100 (around 7%) and 30, respectively.

As a result of these actions, the company anticipates a reduction in quarterly operating expenses by about USD 5 million, starting from the first quarter of 2024.

What Are The Company-Specific Risks Of This Company?

The risks associated with Nordic Semiconductor are certainly present and multifaceted. A critical concern is the company's ability to maintain its competitive edge. Competition in the semiconductor industry is fierce, and companies that do not innovate and keep up with market demands can be quickly overtaken and replaced.

Financially, Nordic Semiconductor appears to be on solid ground. The company carries minimal debt, evidenced by a favorable debt-to-equity ratio of 16.2%. Thus, financial solvency does not pose an immediate risk. Instead, the principal challenges for Nordic Semiconductor stem from competition and the cyclicality of its non-1-tier customer base.

While it's challenging to forecast the company's future competitiveness, its historical performance provides some reassurance. Nordic Semiconductor has demonstrated robust average revenue growth of 22% year-over-year over the past eight years. Nevertheless, there remains the risk of market share loss. Should the company's revenue decline, its valuation would likely decrease rapidly, as it is heavily predicated on anticipated future growth. A failure to meet market expectations could lead to a swift revaluation.

This exact scenario is unfolding currently, with a significant year-over-year revenue drop of 48%. However, it's important to note that this decline is not attributed to a loss in market share, but rather to reduced demand from non-tier-1 customers.

Another risk factor is the inherent cyclicality in the semiconductor industry, which has been evidenced in the past. The volatility among non-tier-1 customers is particularly pronounced, likely exacerbated by macroeconomic factors such as inflation and rising interest rates. These customers have shown to be more susceptible to economic fluctuations, representing a potential risk to Nordic Semiconductor's stability.

Competition

In assessing the competitive landscape for Nordic Semiconductor, it's crucial to recognize that while competition exists, it doesn't come in the form of direct rivals. Each company in this space operates within unique segments and follows distinct business models, making direct comparisons with Nordic Semiconductor challenging. Notably, no other company relies as heavily on Bluetooth revenue as Nordic Semiconductor does. However, Texas Instruments emerges as a competitor, primarily focusing on analog semiconductors.

Recently, they have capitalized on the automotive industry's growth, particularly in China, though their overall revenue declined by 13% year-over-year. Qualcomm, another competitor, also manufactures Bluetooth chips and reported a 5% revenue increase from Q1 2023 to the following quarter. Both Qualcomm and Texas Instruments have experienced slowdowns, albeit not to the extent observed with Nordic Semiconductor in 2023.

It's essential to highlight that Bluetooth is not the primary source of income for any of these competitors, and there is a lack of available data specifying their exact revenue from Bluetooth operations.

Valuation

Multiples

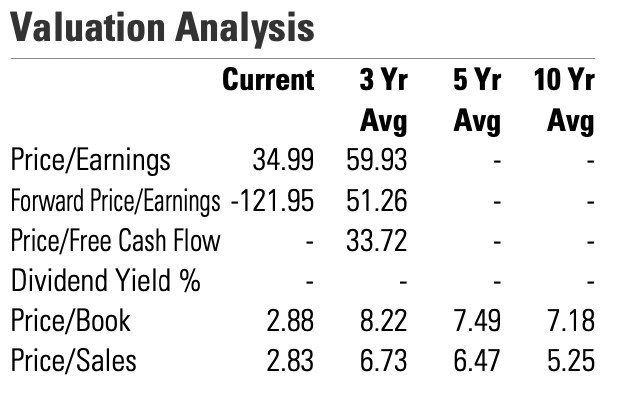

Historical multiples (Morningstar)

Starting with the price-to-book, P/B and price-to-sales, P/S ratios, it's evident that the current multiples are significantly below the averages of the past 3, 5, and 10 years. The 3-year average represents a dream scenario for Nordic Semiconductor, characterized by heightened profitability during the COVID-19 pandemic. In contrast, the 5-year and 10-year averages provide a more realistic view of what a "normal" valuation might look like for the company, with a P/B of 7.18 and a P/S of 5.25, against the present P/B of 2.88 and P/S of 2.83. For these valuation multiples to shift, it would require a trend toward a more positive revenue trajectory for Nordic Semiconductor.

DCF Valuation

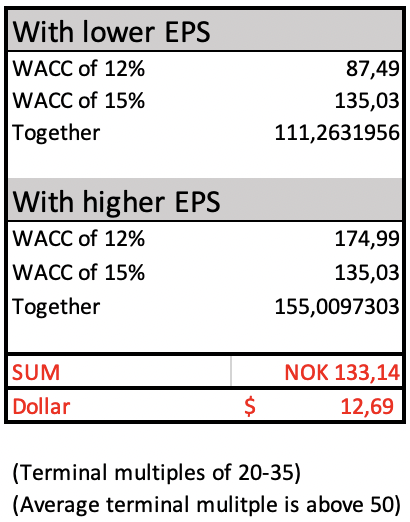

DCF valuation, different scenarios (My own calculations)

In my DCF analysis, I conducted a nuanced valuation incorporating two distinct scenarios. The first scenario assumes a lower EPS of 2 NOK, while the second scenario projects a higher EPS of 4 NOK, applying different WACC values for each. It's important to note that the EPS for 2023 was nearly zero, making these projections relevant for the 2024 fiscal year.

In this sensitivity analysis, the growth rate is categorized into three distinct scenarios, each spanning over the next five years. The first scenario forecasts a 20% annual growth rate, the second anticipates a 30% growth rate, and the third scenario projects a 10% growth rate.

The likelihood of each scenario unfolding is also assessed, with the 20% growth scenario assigned a 60% probability, while both the 30% and 10% growth scenarios are given a 20% chance of occurring. This analysis is further refined by applying varying WACC and terminal multiple assumptions. The terminal multiples are aligned with the respective growth rates, meaning a 20% growth rate is associated with a terminal multiple of 30x, indicating higher growth rates are matched with correspondingly higher multiples.

The valuation employs terminal multiples ranging from 20x to 35x, considered the "optimal" scenario. Despite these projections being on the conservative side, they are still aligned with historical averages.

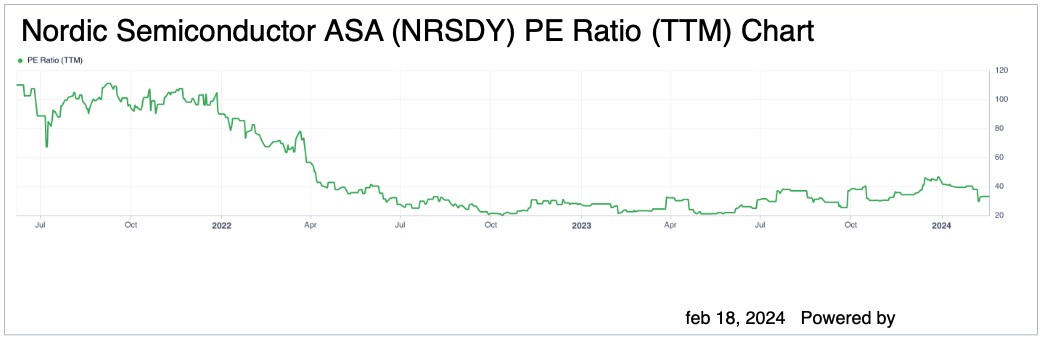

Historically, Nordic Semiconductor's price-to-earnings (P/E) ratio has significantly exceeded 30x, even surpassing 100 during 2021-2022, a surge justified by a revenue increase of over 50% from 2020 to 2021. However, such high multiples are unlikely to recur.

PE ratio the last two years (Gurufocus)

Together with all the different scenarios, the final valuation became 131,39 NOK, which is equal to $12.69 per share NDCVF/NRSDY. I will add that my valuation is weighted towards on "lower" multiples and growth outlooks.

Conclusion

Despite recent challenges, Nordic Semiconductor appears poised for a promising future. With patience and a strategic perspective, this stock is likely to yield significant returns for long-term investors. The key turning point is anticipated to coincide with a reduction in interest rates, which is expected to rejuvenate consumer purchasing power and confidence. Nordic Semiconductor is well-positioned to capitalize on enduring trends in the Bluetooth sector and technology sector, including advancements in digital keys, tracking devices, wireless consumer goods, lighting control, and monitoring systems.

My DCF analysis has determined a per-share value of $12.69 for the stock. Based on this valuation, I advise acquiring the stock at any price under $9, considering the available data.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.