bombermoon

I believe over the next two quarters is the perfect time to buy Enphase (NASDAQ:ENPH) stock. I will be allocating to the company over this period, with high expectations of future performance based on long-term trends in solar energy adoption that, I believe, will continue as normal once the wider global economic climate is less stagnant, as it is at this time. I consider the investment one of the best green-energy investments in the world, and my analyst rating for Enphase stock is a Buy.

Company Overview

Enphase Energy is a global energy technology company with headquarters in Fremont, California. It is most famous for its invention of solar microinverter technologies, and the firm plays a crucial role in the renewable energy sector, including a key role in the solar photovoltaic market.

Enphase has three main offerings:

- Microinverters: As discussed above, these convert direct current electricity generated by solar panels into alternating current electricity for standard use in homes and businesses. The technology increases the energy production of solar panels, improves system reliability, and simplifies installation and maintenance.

- Battery Energy Storage: These technologies allow users to store excess solar energy for use during peak demand or when there is no sun. The products significantly support grid independence.

- Energy Management Software: Enphase provides software platforms for full monitoring and management of its energy solutions by both homeowners and installers. This addition facilitates higher energy efficiency.

At the time of this writing, Enphase has approximately 75% of its operating revenue from the United States, and approximately 25% from the rest of the world. In 2023, the firm made significant strides in expanding geographically, including bringing its Solargraf software platform to Brazil. It also extended its relationship with BayWa r.e. to distribute IQ8 Microinverters in Poland and launched them in Germany. The IQ8 and IQ Battery 5P were also introduced in Australia.

Market Outlook & Operational Strategies

At this time, Enphase Energy is considered a leader in the solar microinverter market. The market grew at a 14.2% CAGR between 2017 to 2021, and the demand for microinverters is expected to continue to experience high growth, with an anticipated 18.1% CAGR in global demand from 2022-2032, according to Future Market Insights.

Alternatively, IMARC Group expects the global solar microinverter market to have a CAGR of 13.3% from 2024-2032. It mentions the rising adoption of solar and trends in carbon footprint reduction, as well as demand for higher efficiency and reliability, as key factors driving the market. IMARC's research shows that The Asia Pacific holds the largest market share, in part fuelled by supportive government initiatives in the region.

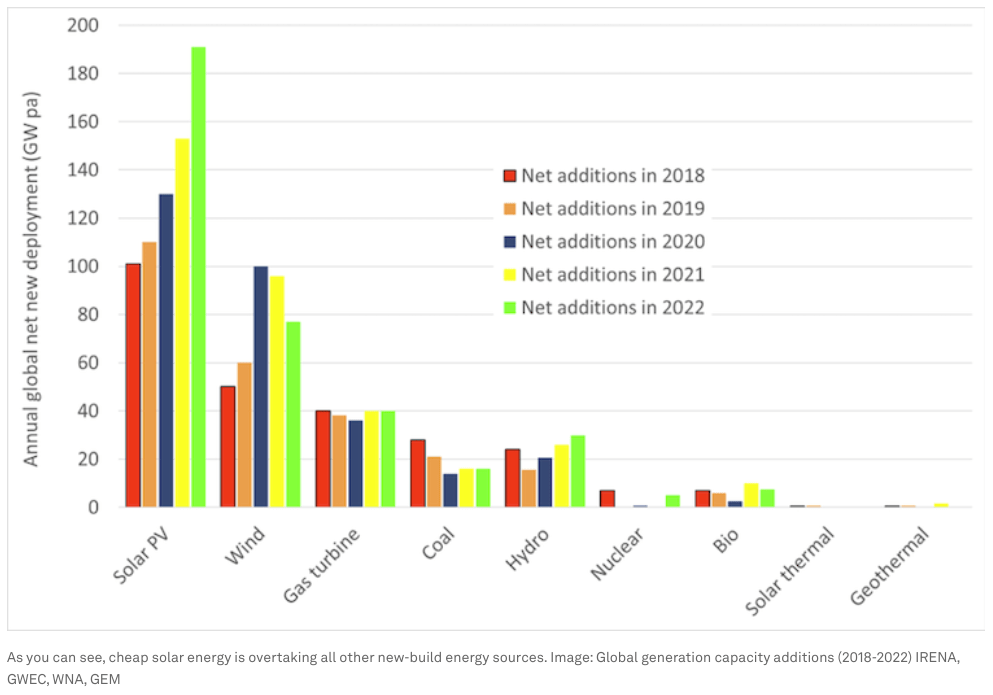

Consider also this chart from the World Economic Forum, from an article that claims that "solar is growing much faster than any other energy technology in history." It estimates it is growing fast enough to "displace fossil fuels from the entire global economy before 2050":

World Economic Forum

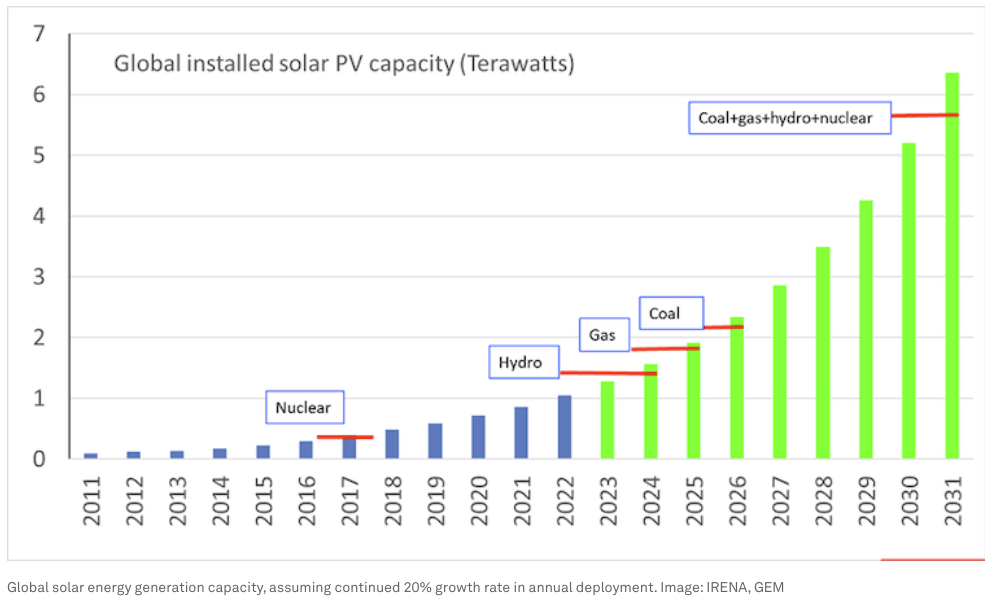

Also consider this immense representation of the global solar energy generation capacity, which will far outsize coal, gas, hydro, and nuclear combined by 2031 if the 20% annual growth rate in the deployment of solar PV technologies continues:

World Economic Forum

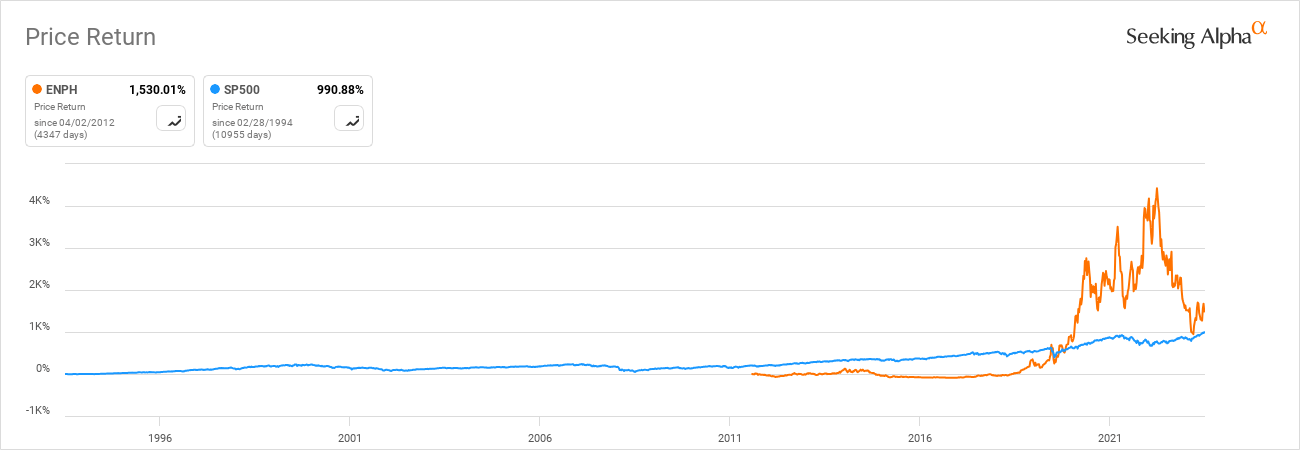

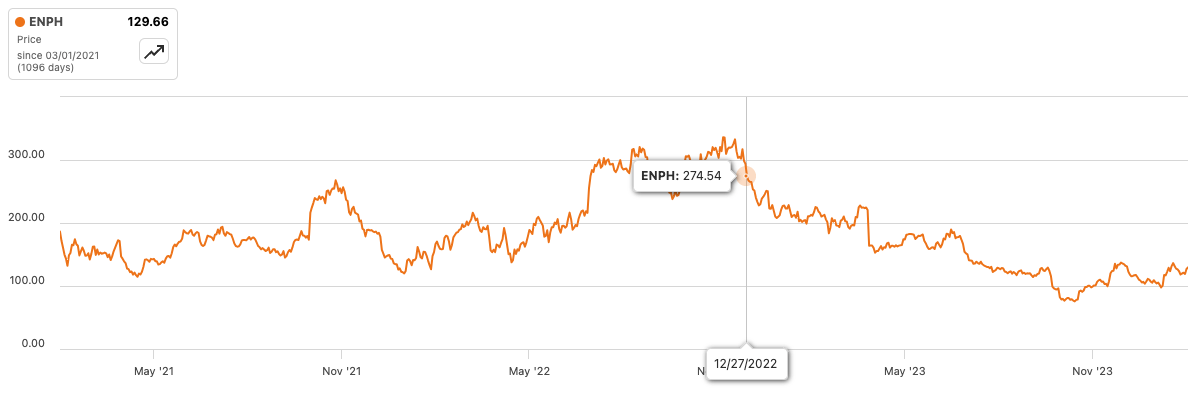

Taking into account these considerations, I think Enphase is an undeniably strong long-term bet on the future of energy. I think now is an ideal time to buy in, considering the stock is selling at 62% below its all-time high at the time of this writing.

Seeking Alpha

Key Financials

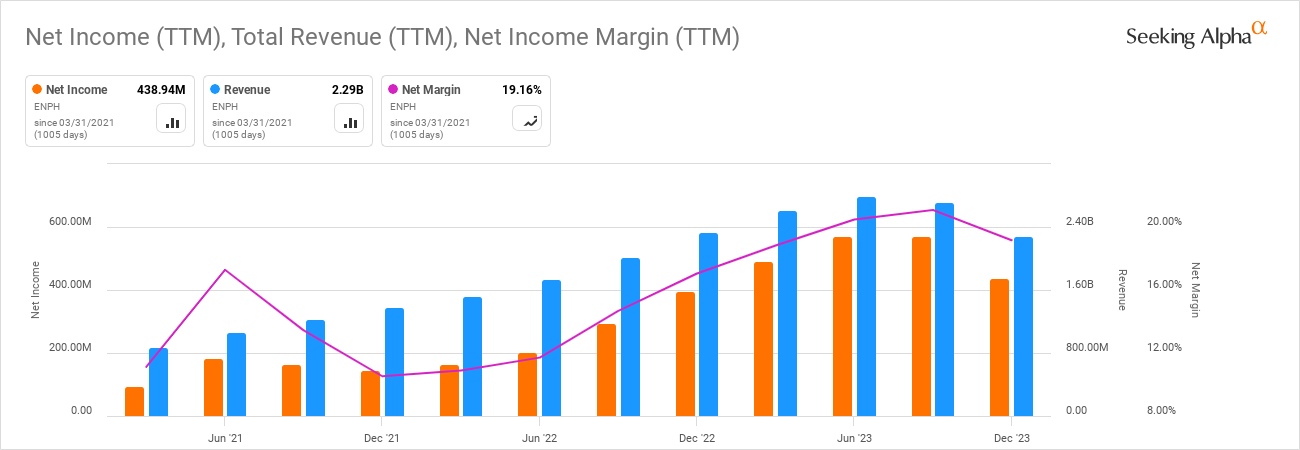

We can see over the past three years that Enphase has had long-term increases in net income and net income margin after a significant drop in 2021. I believe that Enphase, over the medium term, will experience phases of lower profitability than expected as it meets real market demand and has to face governance shifts in favor and momentarily unfavorable to the expansion of the solar PV market. However, over the long term I predict that it will come out on top as a leader in the dominant energy market in the world, and a significantly profitable stock to have bought now over the long term.

Author, Using Seeking Alpha Author, Using Seeking Alpha

Enphase has had a balance sheet for a decade that has not yet achieved a state of stability I would like, and it makes for a moderate risk for my potential allocation. At this time, the firm has an equity-to-asset ratio of 0.29 and a debt-to-equity ratio of 1.32. Compare this to SolarEdge Technologies (SEDG), which has an equity-to-asset ratio of 0.53 and a debt-to-equity ratio of 0.31, SMA Solar Technology (OTCPK:SMTGY), which has an equity-to-asset ratio of 0.41, and no debt, and SunPower Corp. (SPWR), which has an equity-to-asset ratio of 0.23, and a debt-to-equity ratio of 1.24.

We can see from the cash flow statement that Enphase has a significant amount of total debt issued in 2021, but none since this, which bodes well for the balance sheet in the future. However, it has prioritized the repurchase of common stock over paying down the remaining long-term debt it has on its books since its last debt repayment in 2021. I tend to believe that when a balance sheet has an equity-to-asset ratio of under 0.5, it may be wiser for a business to prioritize debt repayments than share buybacks to create more financial stability for the future.

Seeking Alpha Seeking Alpha

Since 2020, Enphase has made several acquisitions that reveal why the firm has higher levels of debt at this time. These include Sofdesk's Solargraf, the Solar Design Services business from DIN Engineering Services, 365 Pronto, ClipperCreek, and SolarLeadFactory LLC. Of these, the most critical is likely its acquisition of Sofdesk in 2021, which provided Solargraf, the integrated software for increasing efficiency in the end-to-end residential solar PV sales process and improving operational management.

Significant Undervaluation

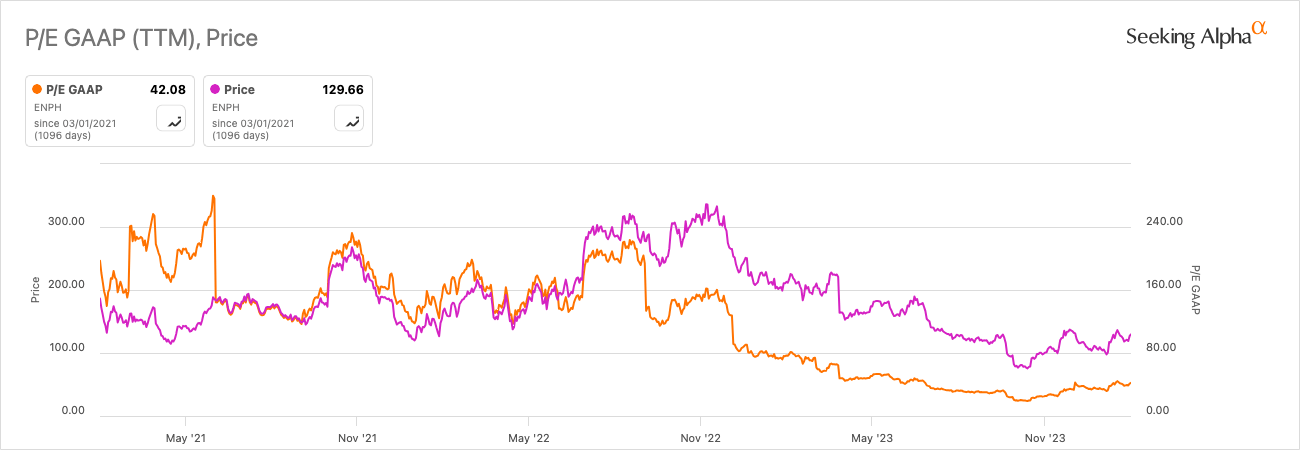

The obvious opportunity here is that Enphase stock is down approximately 60% from its all-time high. However, Enphase isn't cheap on a price-to-earnings basis, with a TTM P/E GAAP of around 42 and a forward P/E GAAP of around 76, indicating potential short-to-medium term downside to come.

Seeking Alpha

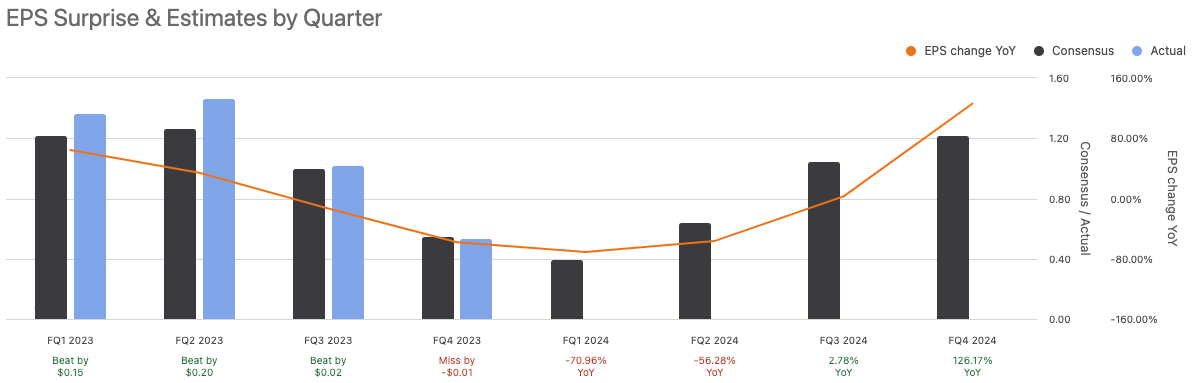

We can also see from earnings estimates in the coming year that EPS is expected to be significantly poor for the first two quarters of fiscal 2024. However, the second two quarters show some light, with analysts on consensus expecting 126.17% YoY growth in Q4. Additionally, consensus EPS estimates for 2025 are resoundingly positive, indicating what I believe will be a great year for the firm. Based on the EPS estimates outlined, I will be building my position in Enphase throughout the next two quarters more aggressively than I will be in the latter half of fiscal 2024, buying in at depressed prices for a better valuation.

Seeking Alpha Seeking Alpha

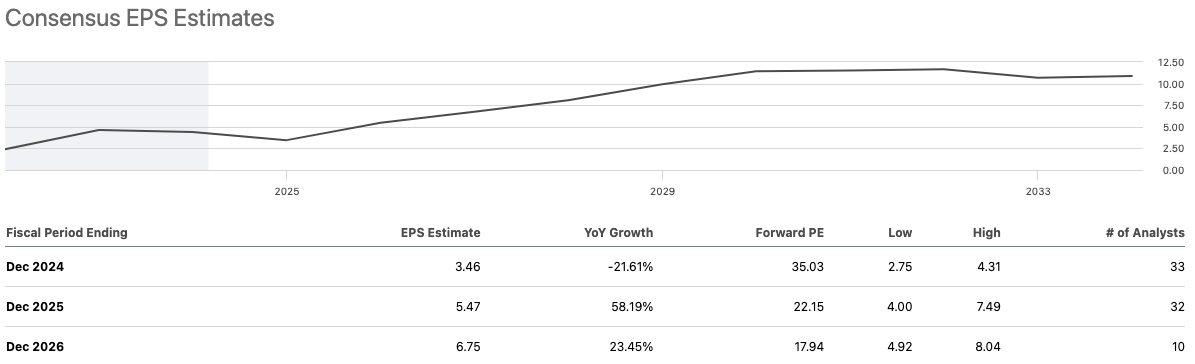

Considering full-year 2024 EPS YoY growth expected on consensus of -21.61%, I estimate that the stock should be selling at around $215 instead of the present price of around $130, indicating a margin of safety of 39.5% at the time of this analysis. To calculate this, I used historical prices to help me determine a time at the end of 2022 when the stock was trading at close to what I deem fair value; I then depreciated this price proportionally to the depreciation in earnings expected, and arrived at a higher fair value than the present trading price. The reason I approached the valuation in this way is that in the technology sector, a standard discounted cash flow analysis is evidently obsolete, as investors are willing to buy shares at a significant premium, and the strong sentiment needs to be adequately priced into a stock. Relying on simple cash flows will miss exceptional future returns as a result of not noticing the value of herd psychology and sentiment.

Author, Using Seeking Alpha

Further Risk Analysis

The fall in stock price in 2022 and beyond was driven by a decrease in US revenue and a decrease in overall sell-through of microinverters in fiscal 2023. Revenue in Europe also decreased, including a decrease in sell-through of microinverters and IQ batteries in Europe. In fiscal 2024, the same challenges remain, with continued reduced demand in Europe and a further decline in the US, most notably in California. At this time, its days inventory is building up, and its days sales outstanding is building up, indicating the difficulties in selling its goods, but also a difficulty in collecting payments from customers. This is quite a challenging picture for investors to deal with, but my long-term investment thesis hinges on the fact that the company is going to experience continued high growth as demand for solar continues to proliferate beyond this tighter economic period. I believe that with the advent of AI and as this proliferates throughout economies, driving wealth generation and efficiency in business, solar energy will again be at the forefront of institutional and civilian demand as regulatory pressures continue to mount in support of green energy trends.

Conclusion

I am planning on allocating to Enphase mostly in the next two financial quarters, and I expect to add to my position over time, buying in at times when the valuation looks more favorable. I see the investment as a significant long-term allocation in the future of energy, and I consider Enphase one of the critical organizations that will continue to drive success in the industry. I consider the present risks around demand a result of tighter economic conditions globally at this time, and I expect this to ease eventually, bringing normal high growth. While the balance sheet is my largest risk with the investment, I believe this is manageable, and I will keep a careful eye on how it develops.