PaulMcKinnon

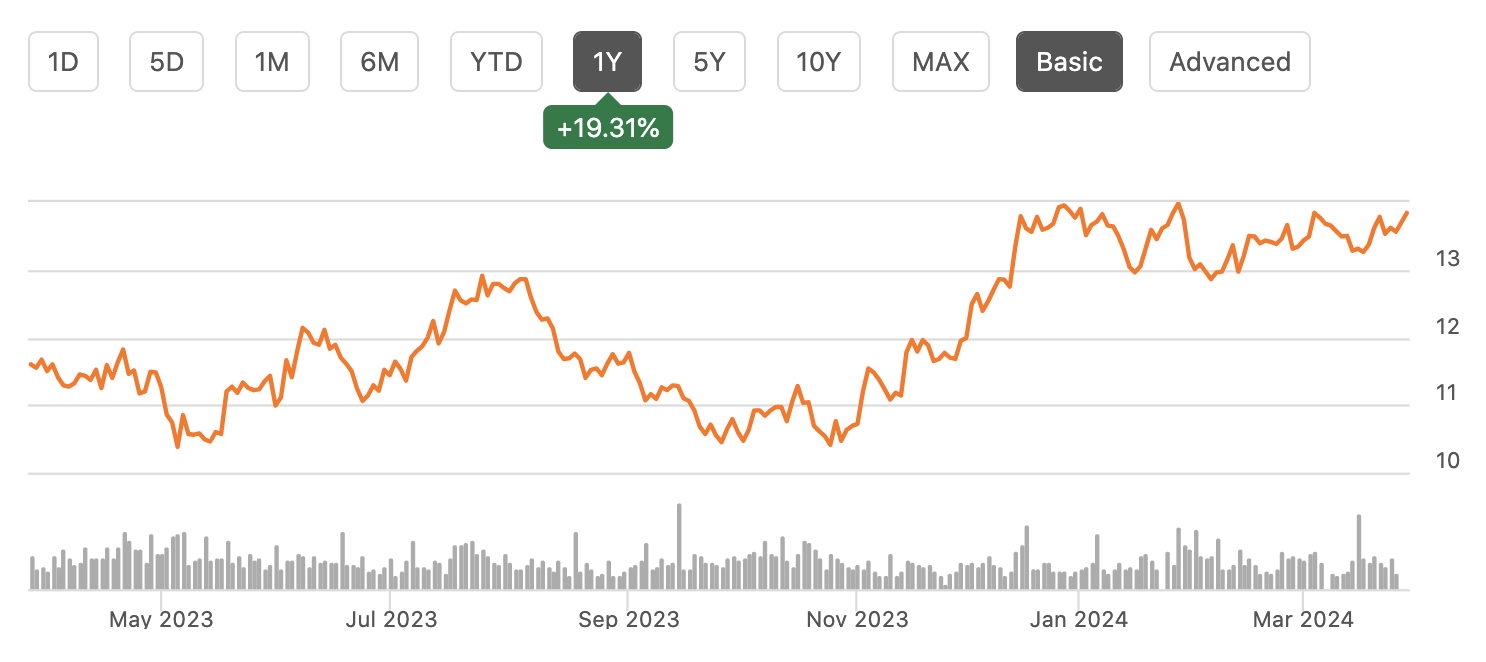

Shares of F.N.B. Corporation (NYSE:FNB) are trading near a 52-week high, up 19% from a year ago, which has lagged the S&P 500’s 30+% return over this period. Most regional banks have been underperformers over the past 12-18 months, given the challenges caused by the Q1 2023 banking crisis, though FNB has acquitted itself fairly well. Additionally, since recommending shares as a buy in November, FNB has returned over 18%, a bit ahead of the S&P 500’s 15% return. I have been impressed by recent management actions and continue to view FNB as a buy.

Seeking Alpha

In the company’s fourth quarter, FNB earned $0.38 in adjusted EPS, down from $0.44 a year ago. This beat consensus by $0.03. For the full year, it earned $1.57, up 12% from 2022. In 2023, EPS rose by 12%, making FNB one of the few banks to grow earnings, thanks to its solid handling of the deposit crisis. Q4 Headline EPS was negatively impacted by about $0.25 because in December, it sold $650 million of securities with a yield of 1.08%, taking a $67 million loss. It reinvested this in securities that will generate about $20 million more in pre-tax income in 2024 thanks to this transaction.

In my last article on FNB, I noted the company had managed the interest rate volatility fairly well over the past year with manageable unrealized losses on its investment portfolio of ~$7.2 billion. This is a very conservative portfolio over 85% of the portfolio AAA rated and just a 4.2 year duration. This has helped to minimize the magnitude of losses vs other banks with larger or longer-duration securities portfolios. Still, just about any bond bought before the Fed began raising rates aggressively is likely to have an unrealized loss.

By selling this tranche of debt and reinvesting in higher yielding securities, FNB immediately boosts net interest income. Alongside the retirement of preferred stock, the company sees a less than one-year breakeven period vs five years on share repurchases. FNB also sized this sale, at about 9% of its portfolio, to maximize its return, add as such no more security sales are likely.

FNB was able to do this because of its strong capital position. These unrealized losses flow through to accumulated other comprehensive income (AOCI) on its GAAP financial statements. Currently though, banks that are not systemically important are able to exclude these unrealized losses from their capital calculations. As a bank with under $100 billion in assets, FNB will continue to exclude these unrealized losses even after the phase-in begins for mid-sized banks at the end of 2025. By selling these bonds and taking the loss, this loss now does count against its capital position.

This is a reason why most banks continue to hold underwater low-yielding bonds. Given the extent of the rate move, taking meaningful losses will greatly reduce capital positions. As such, they hold the low-priced bonds, earning lower interest, until they gradually accrete to par and can be reinvested. Ultimately, it is a trade-off between current capital positioning and net interest income.

Because FNB has been strongly capitalized, it was able to accept the modest capital hit of this transaction in order to boost go-forward interest income. FNB has a 10% common equity tier 1 (CET1) ratio, which is down from 10.2% in Q3 but still strong. Even factoring in all remaining unrealized losses on securities, it would have a nearly 9% CET1 capital ratio, well above the 7% regulatory minimum. FNB can safely operate its business in the 9-9.5% capital area. It carries a bit of excess capital today, to compensate for the economic reality of these remaining unrealized losses.

But even with them, its capital position is essentially where it should be. As bonds continue to mature, the impact of its AOCI loss will also shrink. Because FNB has sized its investment portfolio appropriately to the overall bank’s balance sheet and because of its fairly short duration, its unrealized losses have been manageable, and indeed with its strong capital, FNB has actually been able to further optimize its balance sheet and boost net interest income.

Importantly, the rest of the bank continues to operate well. As a reminder, FNB operates the First National Bank, which has branches across the mid-Atlantic, primarily in Pennsylvania, Maryland, DC, and the Carolinas. The bank ended the year with $34.7 billion of deposits. Deposits rose $96 million sequentially, and are up 1% from a year ago, even as the industry has seen net deposit outflows, a strong performance. This is partly due to FNB’s granular deposit base where 78% of deposits are insured or collateralized.

Now while FNB has retained deposits quite well, they have of course become more costly as rates have risen. Cost of funds rose by 21bp sequentially to 2.14%, which was up 134bp from last year. Additionally, as rates have risen, customers have moved funds away from transactional, noninterest-bearing accounts to interest-bearing ones. FNB has handled this transition fairly well, and 29% of deposits are noninterest-bearing. It has seen very modest losses here, and the recent pace has been moderate. In Q4, NIB balances fell 3% sequentially on average while total deposits rose by 0.8%

FNB

Because of higher funding costs, its net interest margin (NIM) has compressed, but the pace of decline is slowing. NIM fell 5bp sequentially and 32bp from last year as net interest income (NII) fell $3 million from Q3 and $11 million from last year. With its securities sales netting about $5 million per quarter, I expect to see NII bottom in Q1 and gradually rise.

With a relatively small securities portfolio, FNB primarily is a lender with $32.3 billion of loans for a 93% loan to deposit ratio. Loans grew 1.7% sequentially and 10% from a year ago, and because much are floating rate, asset yields rose by 14bp from Q3 and 96bp from Q4 2022.

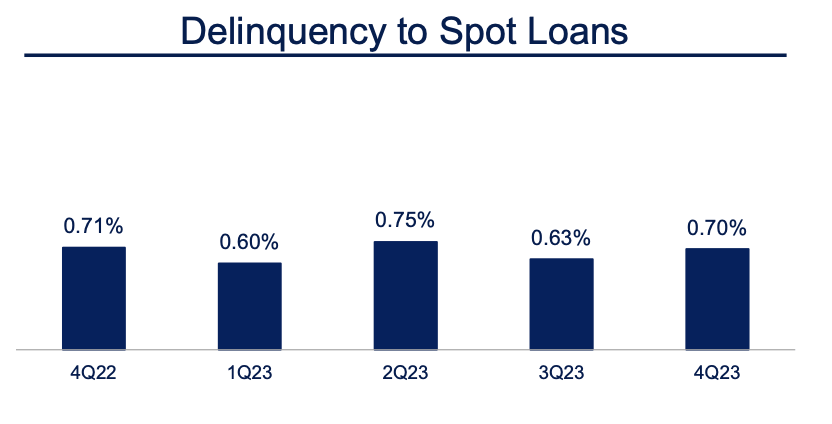

Importantly, I view FNB as a differentiated underwriter, and there was a return to its history of strong credit results after its $32 million blemish from an alleged fraud in Q3, which I argued at the time investors should view as one-time. Charge-offs are a modest 0.10%, and even as the economic cycle ages, we are not seeing a worsening in credit quality. Its 0.7% delinquency rate is flat from 0.71% a year ago while NPLs of 0.34% are down from 0.39% a year ago. There is no sign of material degradation. On top of this, FNB is very well reserved for a potential worsening. It has set aside 1.25% of loans for potential losses, providing 378% coverage of NPLs, up from 354% a year ago. This is above my 250% healthy level of reserves benchmark.

FNB

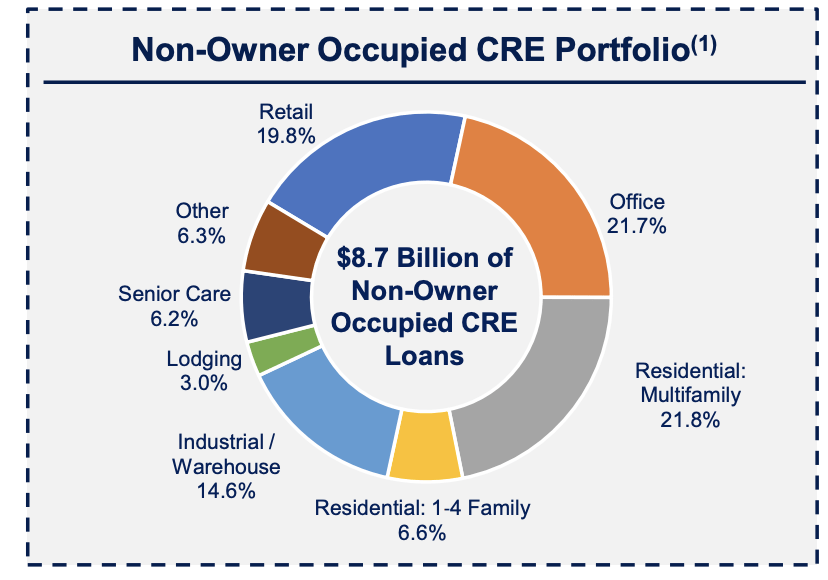

One reason for its steady credit profile is that unlike many regional banks, FNB has modest commercial real estate (CRE) exposure. Non-owner commercial real estate is just 27% of its loan portfolio. As you can see below, just a fraction of this is office, the most troubled sector. Within office, there is just a 0.26% delinquency rate. Additionally, 20% of office maturities are this year. This will be key to watch. Given the low delinquencies, I expect most of these to mature without issue, further reducing FNB’s exposure to the sector. However, investors should monitor coming quarters to see if there are any issues with this piece of the portfolio. Given excess reserve coverage, FNB can afford to see a tick-up in charge-offs.

FNB

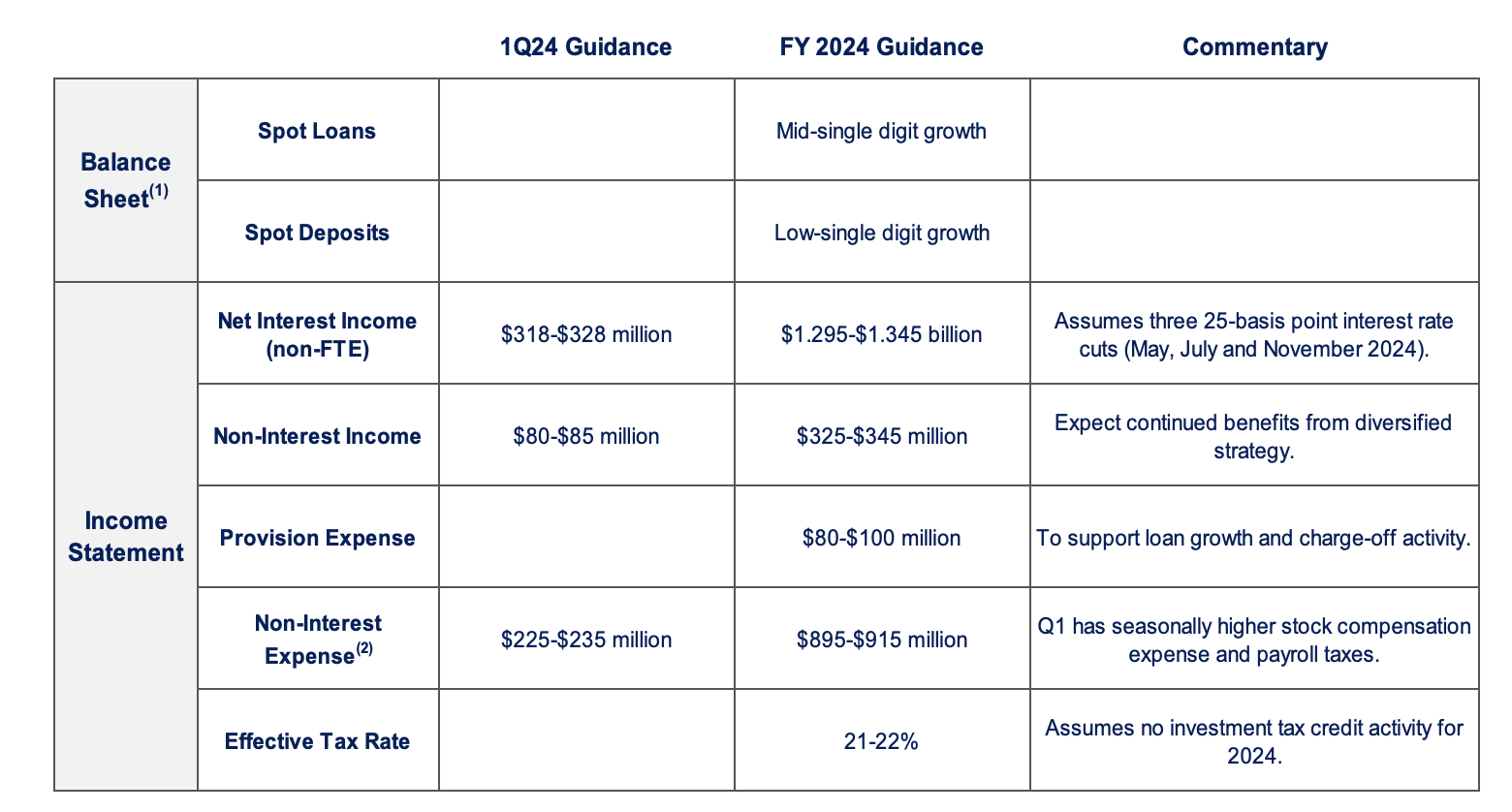

Below is the company’s guidance for this year. Q4 NII was $1.296 billion annualized, so FNB is guiding to a modest increase here, assuming three Fed rate cuts as it continues to grow deposits. Given its securities sale, I expect interest income to be $1.32-$1.35 billion. Management is also guiding to noninterest income that will be flat to up 6%. Given improving capital market activity, I view this as reasonable.

FNB

As such, I am looking for FNB to earn about $1.50-$1.55 this year. That provides ample coverage of its 3.5% dividend yield. Given it used up some excess capital to optimize its securities portfolio, I expect a bit less buyback activity than previously, especially as it views the first use of its retained capital as supporting ongoing loan growth. Still, after its dividend, FNB will retain over $1 in EPS. I would expect 50-70% to be used to support growth, enabling about a 2-3% reduction in the share count from repurchases.

With its strong balance sheet management and solid loan book, I view FNB as a sound long-term investment and attractive at 9x forward earnings. I expect shares to migrate to ~$15.5 or 10x forward earnings, providing about 12% appreciation potential, over the next year, especially as buyback should accelerate further in 2025 as it will have earned back the capital impact of its December actions. With net interest income bottoming, shares have further upside.