Justin Paget

Dear readers,

eXp World Holdings (NASDAQ:EXPI) is a cloud-based real estate brokerage which has tried to revolutionize the real estate industry by challenging the age-old norm that a brokerage needs a physical brick and mortar location to operate. The company IPOed in 2013, but hasn’t really gained any traction until 2020 when its stock price sky rocketed from $4 per share to almost $80 per share.

The business model sounds appealing. Eliminating brick and mortar locations significantly lowers the overhead expense, improves the scalability and allows for better renumeration for real estate agents and lower fees for customers. But the one thing it doesn’t do is protect the company from weakness in the housing market. At the end of the day, this is a brokerage and it needs a healthy housing market with lots of buying and selling activity to flourish. That’s why in this piece I want to focus, above all else, on future prospects of the housing market and where it might go from here.

I’ve covered EXPI before, most recently in early-November with a SELL rating at $12 per share. My bearish thesis was based on poor short-term housing market prospects and an unreasonably high P/E of 95x. I also advised against shorting the stock, because of very high short interest at 25% of float, which could easily result in a short squeeze.

Since that article, EXPI’s price has declined by 16%, while the S&P 500 (SPX) has climbed nearly 20% higher. The underperformance was largely a result of poor Q4 results which missed expectations and came in at -$0.09 per share.

SA

Housing market dynamics are improving but remains poor in the short-term

As I’ve said, EXPI relies on a healthy housing market. And unfortunately, the housing market has been anything but healthy lately. The steep rise in interest rates over the past year and a half has led to an increase in mortgage rates from around 4% at the start of 2022 to over 7% as of today.

Redfin

At the same time, housing unaffordability has reached historical levels. Currently to afford a median house, an annual income of $115,000 is needed. That’s more than $40,000 over the median household income in the country. Combined with high rates on mortgages, this means that the monthly payment is simply out of reach for a large number of potential buyers.

Normally, one would assume that real estate prices would adjust downward in such an environment, but due to a low level of inventory in the market, this hasn’t happened and prices have remained largely flat over the past two years. The market remains largely frozen, with transaction activity down significantly, as buyers are not able to afford the monthly payment and many sellers are not motivated to sell, because they don’t want to give up their low-rate mortgage and have to commit to a higher rate mortgage when they buy their next house. This has reduced available inventory substantially.

FRED

Now the question is what will happen going forward. Amongst the primary catalysts that could improve the situation is a drop in the Fed funds rate, which would most likely translate into lower yields and mortgage rates and drive a housing market recovery.

Prior to the Fed’s most recent FOMC meeting, analysts were expecting the first interest rate cut as soon as March. But with inflation plateauing around 3%, above the Fed’s 2% target, and with strong ongoing economic growth of 3.7% in Q4 2023, above the “below trend” growth of 2% that the Fed said would be needed to tame inflation, the Fed has decided to keep interest rates unchanged for longer. Currently, trading activity implies a 53% probability of at least one cut by June and 73% by July which means that we already start to see the light at the end of the tunnel.

CME Fed Watchtool

I don’t know where interest rates will head in the future, but my base case is that interest rates and yields will decline over the course of 2024 which should help the housing market and increase buying and selling activity. I do believe that nationwide the housing market has bottomed.

Long-term performance driven by valuation

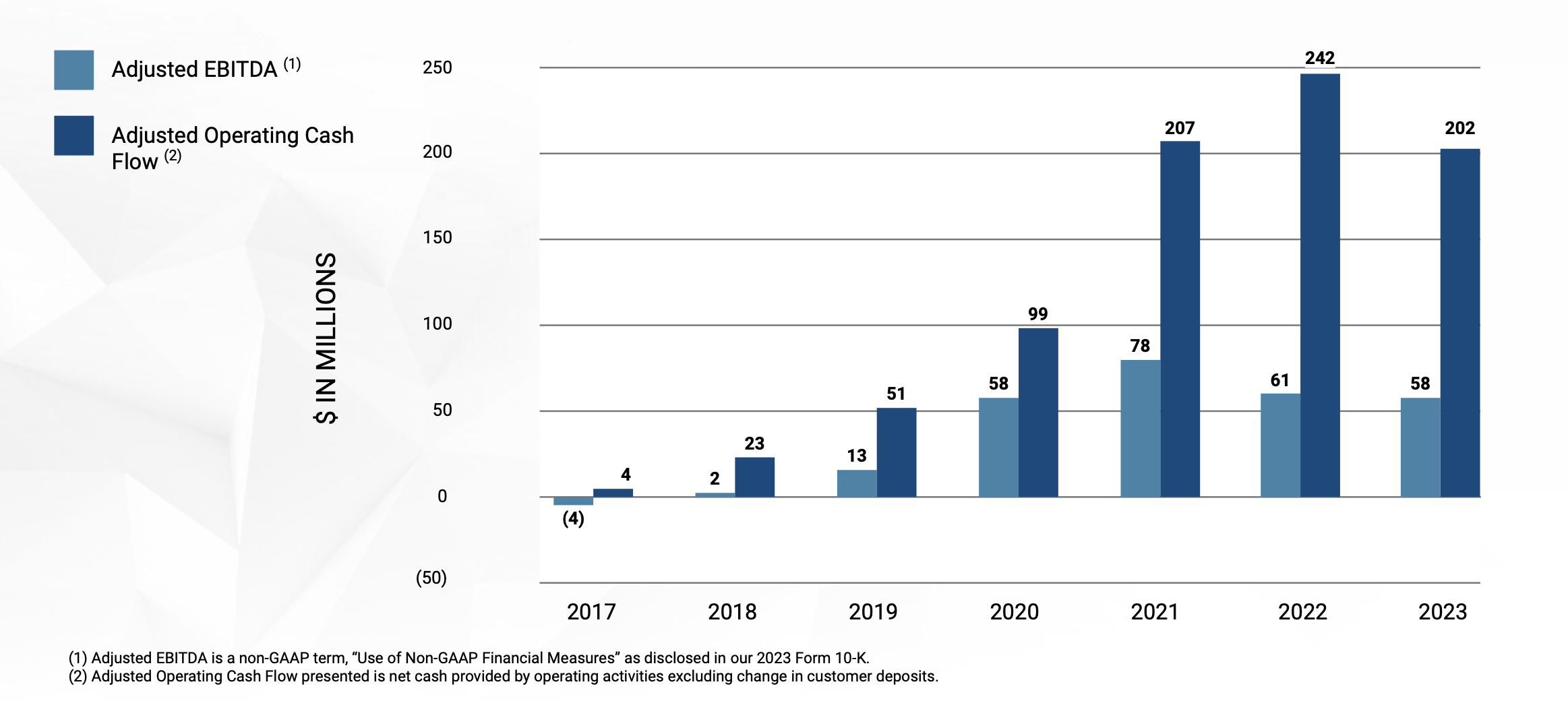

If I’m right about the trajectory of interest rates, then we’ve probably seen through earnings for EXPI this year. Though I should also mention that with EPS of just $0.17 in 2023 and negative EPS in Q4 2023, the bar is set exceptionally low.

Next year, the general consensus is for EPS of $0.44 in 2024, up 81% from last year. But I also want to point out that a year ago, the consensus for 2024e EPS was double what it is today. And I won’t even touch on expectations from 2021 which saw EPS reaching $2.00 per share by today.

SA

I like EXPI’s low overhead business model and I do think that the housing market is headed higher in the future. But the problem I have with the stock remains valuation.

Based on 2023 actual earnings the stock trades at 58x earnings and has an EV/EBITDA of 25x. That’s expensive. And while using 2024e numbers gives a more reasonable estimate of 22x earnings, I’m doubtful that EXPI will hit the target as market activity is unlikely to pick up before at least the middle of the year.

EXPI IR

Risks

I’m fairly bearish on EXPI, but I don’t recommend shorting the stock because of high short interest which increase the risk of a potential short squeeze, like the one we saw in mid-2023 from $12 per share to $24 per share.

Since I’m staying out of the stock, the only risk is that I’ll miss a rally. This could happen if interest rates and consequently mortgage rates decline faster than expected and housing market activity picks up. At the end of the day, however, I do think that the overvaluation risk overweighs this opportunity costs for EXPI. Moreover, I see better way of playing a housing market recovery such as investing in selected apartment REITs.

Bottom line

At the end of the day, EXPI is a leveraged bet on housing market activity. I do think that rates are headed lower and buying and selling activity will pick up in the latter half of 2024, but I do not think that it will be enough to hit the 2024e consensus estimate. As a result, I expect forward earnings to be revised downward (again, as they have been almost every quarter since early 2021). I would have been perfectly happy, buying a small speculative position around 20x trough earnings, but at 58x and with a slower than expected recovery, I see the stock as too risky leading me to a SELL rating

If you want to access my entire Portfolio and all my current Top Picks, feel free to join ‘High Yield Landlord’ for a 2-week free trial.

We are the largest and best-rated community of real estate investors on Seeking Alpha with 2,500+ members on board and a 4.9/5 rating from 500+ reviews:

![]()

You won't be charged a penny during the free trial, so you have nothing to lose and everything to gain.

Start Your 2-Week Free Trial Today!