The Good Brigade/DigitalVision via Getty Images

Introduction and thesis

Central Garden & Pet Company (NASDAQ:CENT) is a leading innovator, producer, and distributor of branded and private label products for the lawn and garden as well as pet supplies markets. The company operates through two segments: Pet and Garden.

CENT is a highly quality business, in what we consider a lucrative industry, underpinned by a competent management team. This alone positions the company well for long-term growth, particularly if it can continue to acquire businesses regularly to supplement its organic trajectory.

We are limited in our concerns, although expect the coming year to be difficult as the macroeconomic environment weighs heavily on the company. This limits its scope for upside, particularly when its valuation is not overly depressed. Our belief is that investors are likely confident in the company’s ability to return to its prior trajectory, reflecting its strong competitive position.

For this reason, we consider the stock a hold.

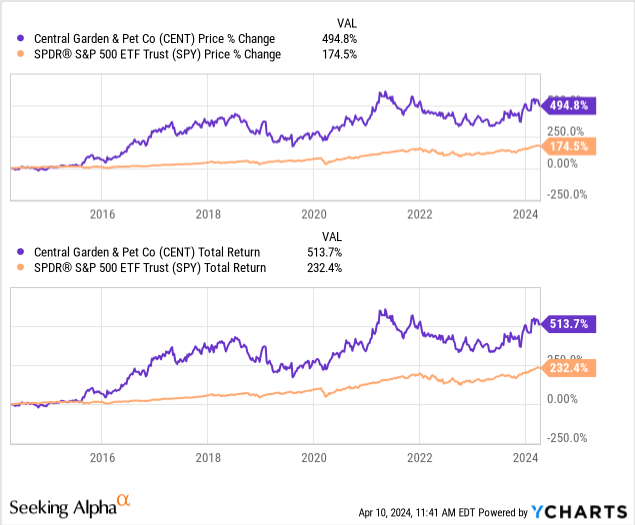

Share price

CENT’s share price performance has been impressive, with over 400% gains. This is a reflection of its impressive financial development during this period, as the company has gained market share and expanded its presence.

Financial analysis

Capital IQ

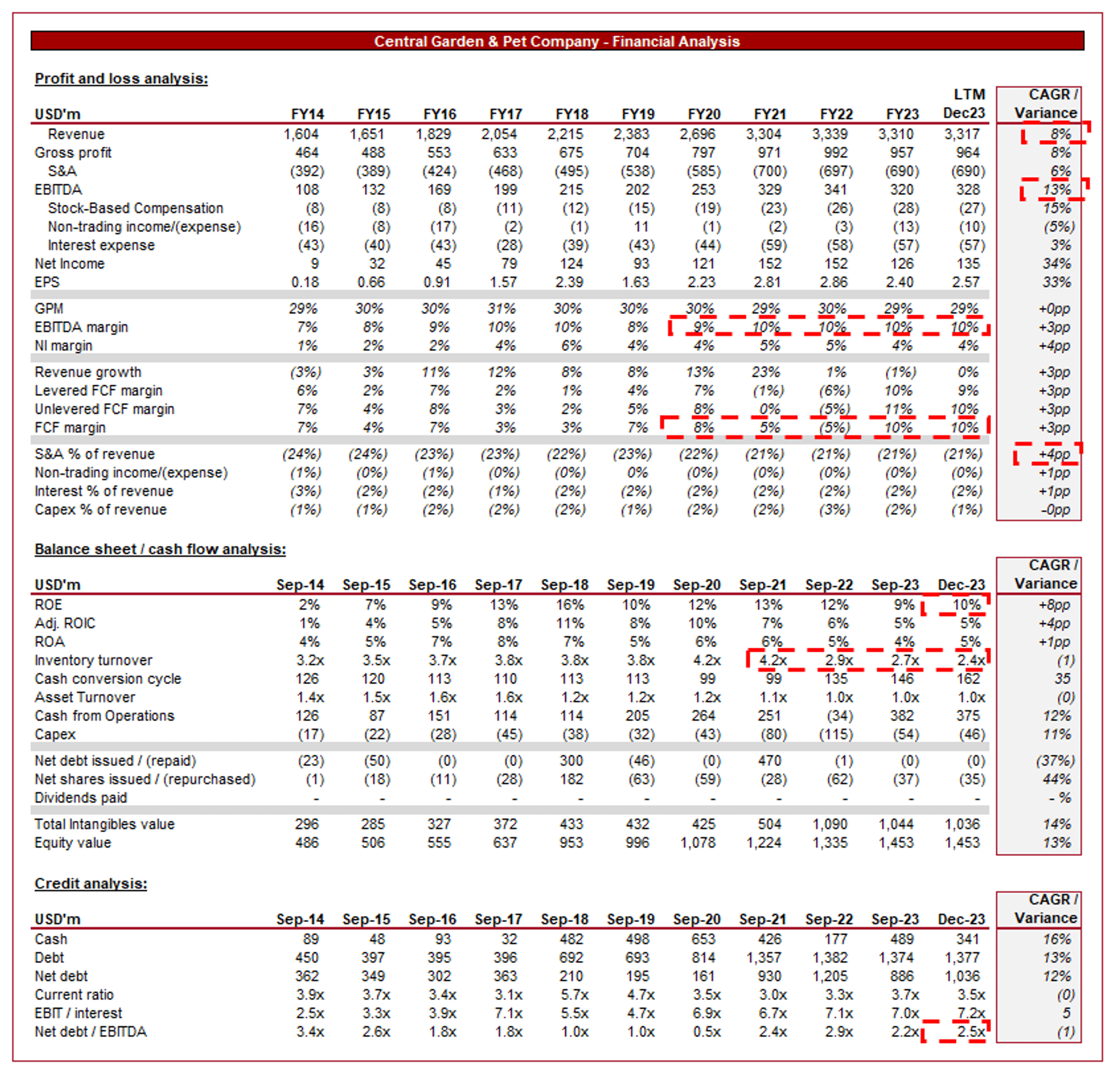

Presented above are CENT's financial results.

Revenue & Commercial Factors

CENT’s revenue improvement has been impressive given the maturity of its industry, with a top-line CAGR of +7%. In conjunction with this, EBITDA has outperformed, with a CAGR of +14%.

Business Model

CENT offers a diverse range of products, including pet supplies, pet food, and lawn and garden care products. The company operates through multiple brands, many of which it has acquired over the last few decades, each catering to specific market segments or geographies.

CENT

Its consistent organic growth and acquisitions have allowed the company to reach a market-leading position (top 3 brands) within its industries and subsegments (differing pets and products). This has contributed to a compounding effect as it grows its recurring customer base and the widening of its moat.

The company utilizes various distribution channels, including mass retailers, home improvement centers, independent pet retailers, and e-commerce. These relationships have been developed over many decades, contributing to an unrivaled reach to consumers, many of whom are not wholly educated in brands and so will reach for those stocked at their primary retailers.

CENT

Competitive Positioning

We see the following factors as critical growth drivers and commercial qualities:

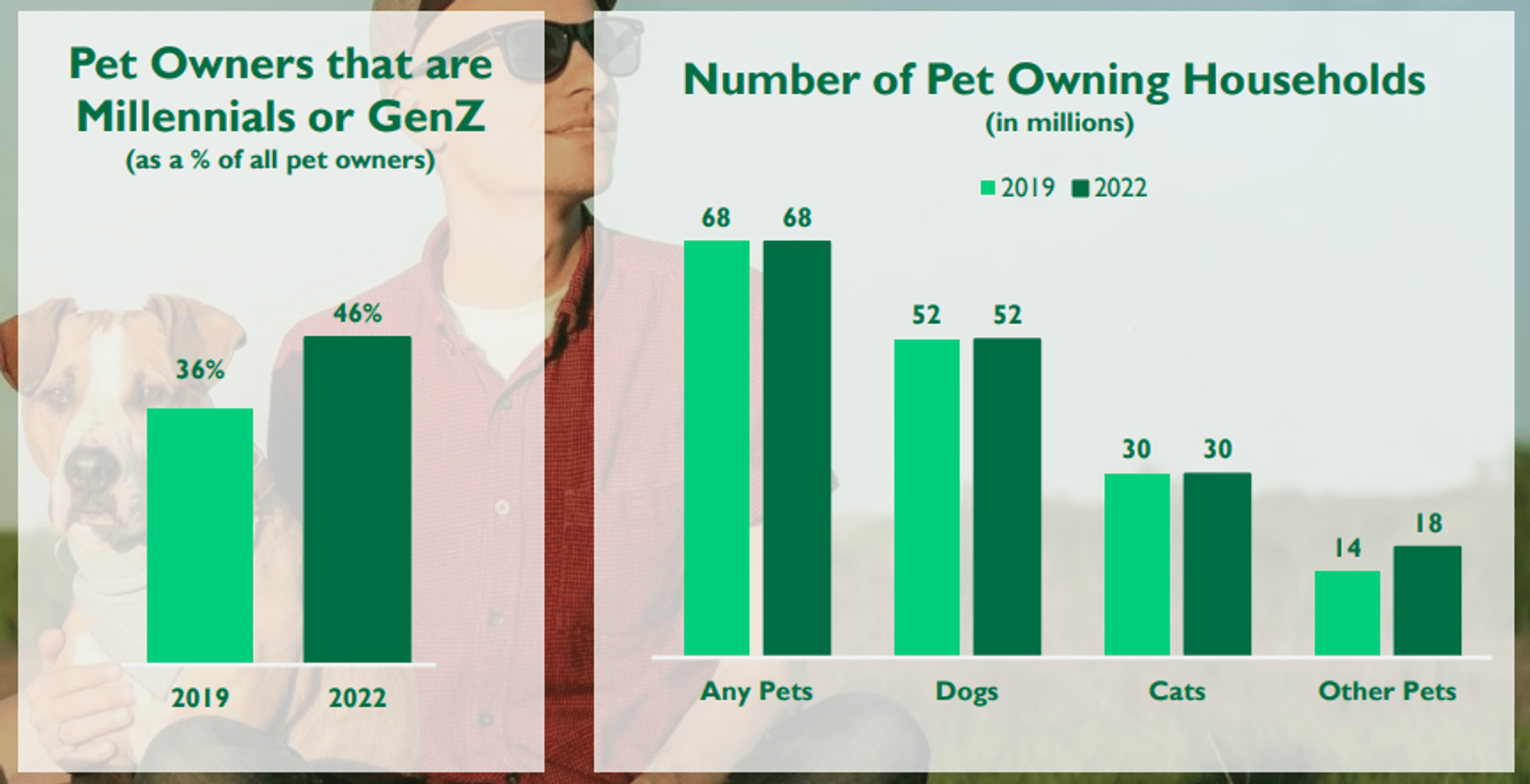

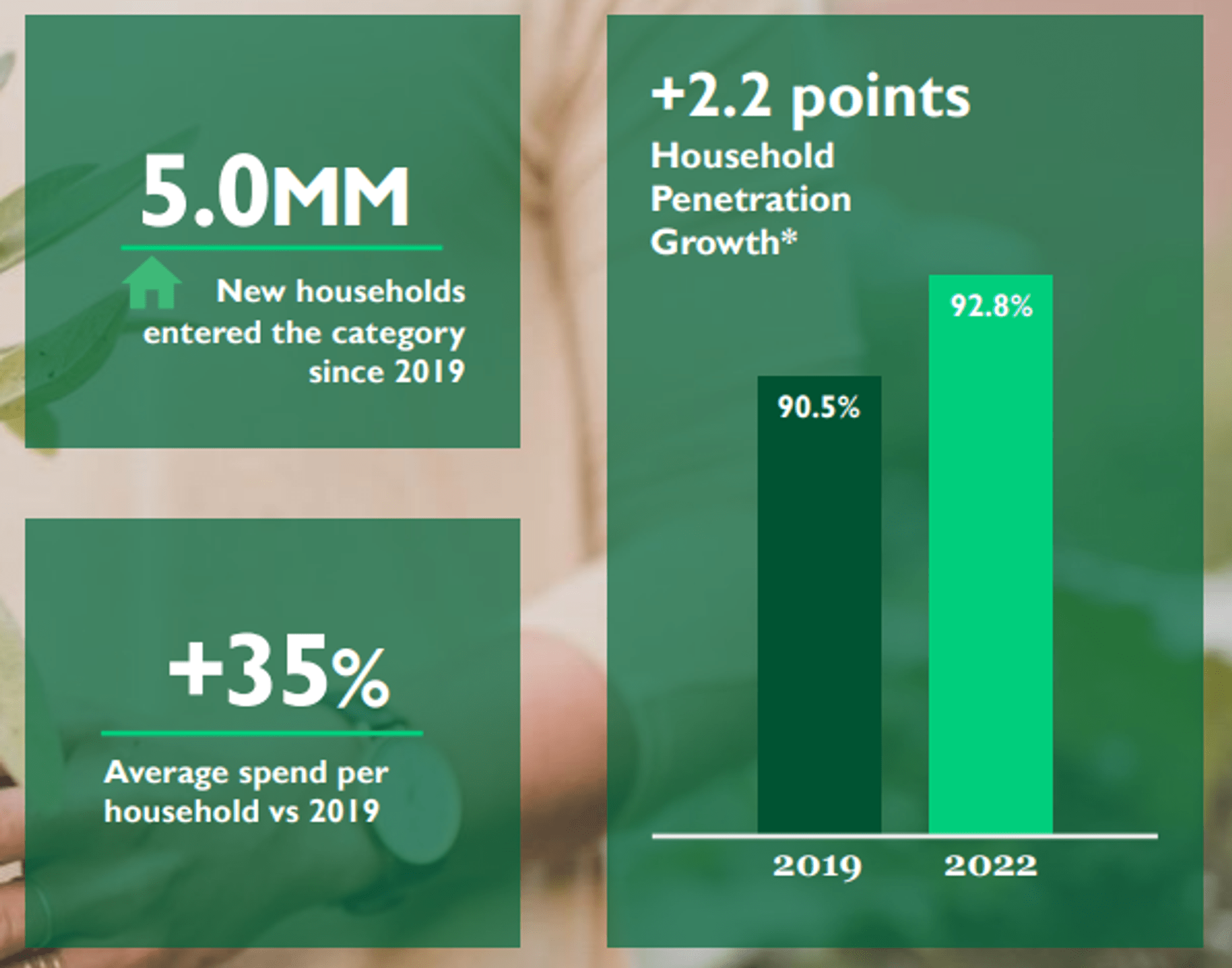

Pet Ownership: Pets have always been considered a “part of the family,” with the number of pet-owning families remaining robust. Importantly, the proportion of Millennials or GenZ is high and growing, which bodes well for long-term growth. This is also beneficial because demand is incredibly robust. Consumers are unwilling to compromise on the health of their pets, contributing to reduced demand volatility.

CENT

Home Gardening Boom coming soon?: The increased interest in home gardening, particularly during pandemic lockdowns and increased time spent at home, has boosted sales in the lawn and garden segment. Further, the lasting impact of working from home will drive demand for bigger, out-of-city homes (which have more land).

CENT

Brand Recognition and Loyalty: CENT has built strong brand recognition and customer loyalty over the years. As previously touched on, consumer demand will be resilient in its key markets, positioning the company well for consistent and recurring sales. Its efforts to interact with current and potential customers, as well as sustainability initiatives have all worked to improve its visibility.

M&A: M&A is a core component of the company’s growth strategy. It has pursued strategic acquisitions to expand its product offerings and market reach. The industry is highly fragmented, allowing a good runway for small bolt-ons over time.

Product development: CENT emphasizes innovation in product development. Despite the industry being relatively mature, we have seen consumers increasingly seeking high-quality and natural products for their pets (similarly to the trend in human food consumption). This has positioned CENT well to respond given its attitude of consistent improvement. More broadly, the company has created “Central Ventures,” where it seeks to partner with leading innovators in the Garden and Pet segment to accelerate its own growth and be at the forefront of innovation.

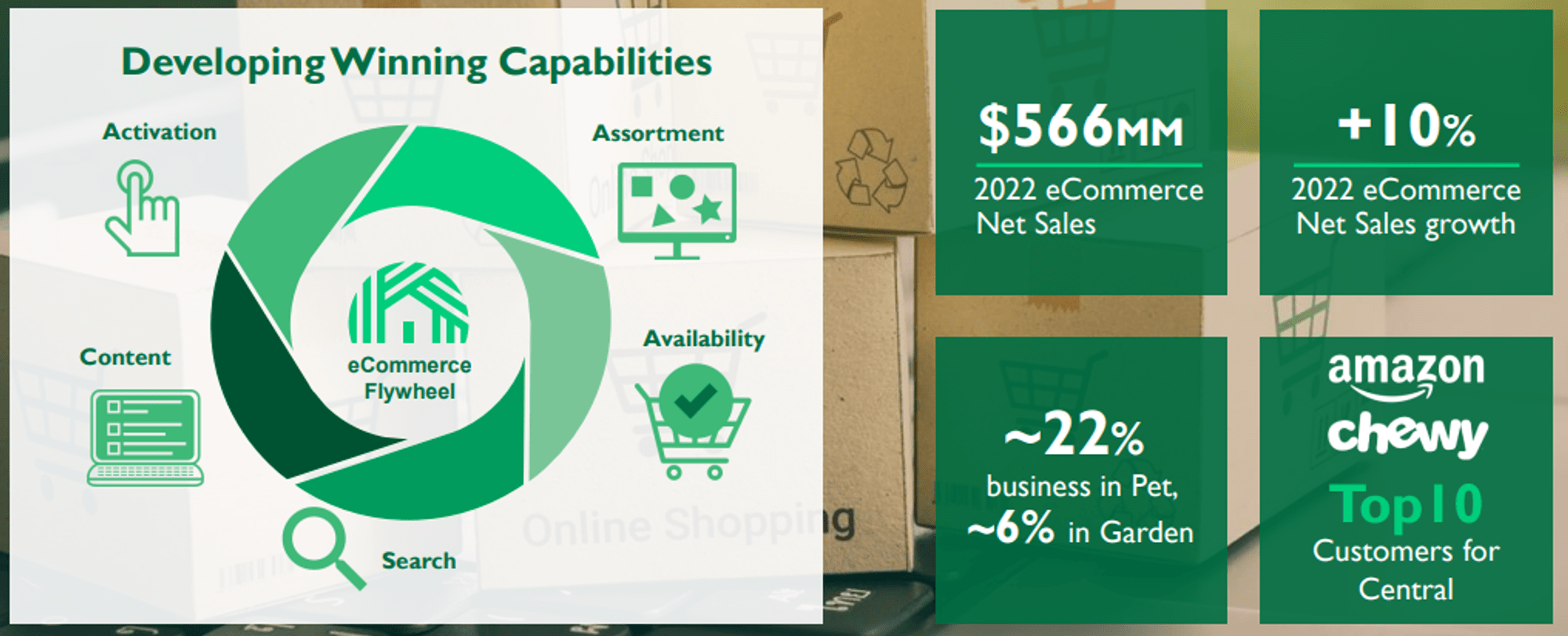

E-commerce Success: The integration of e-commerce into its business model has allowed CENT to tap into the growing online retail market, and particularly the Millennial/GenZ segment that is growing so well. E-commerce is a strategic focus for the company and is delivering early successes through penetration. With a number of brands and strong existing relationships with distributors, this is a significant opportunity for CENT to improve margins and sales.

CENT

Financials

CENT’s recent performance has been muted, with numerous quarters of negative growth. Top-line revenue growth was (4.8)%, +0.8%, +6.0%, +1.1% in its last four quarters, although importantly, margins have remained stable.

The weakness experienced is attributable to current market conditions, with elevated interest rates and inflation contributing to softening spending by consumers as they seek to protect their finances. This is not to suggest consumers are not feeding their pets, but instead that pet adoption has materially softened and consumers are seeking to trade down where possible, with a similar impact on garden spending.

Management is performing well to gain market share during this and achieve operational improvement, but there is an inherent cyclicality which limits the ability to outperform. The company, to an extent, is exposed to the level of demand from retailers, which, as its inventory turnover illustrates, is softening. Looking ahead, we expect CENT to face further pressure on growth, although not necessarily a substantial drawdown given the resilience shown thus far.

CENT

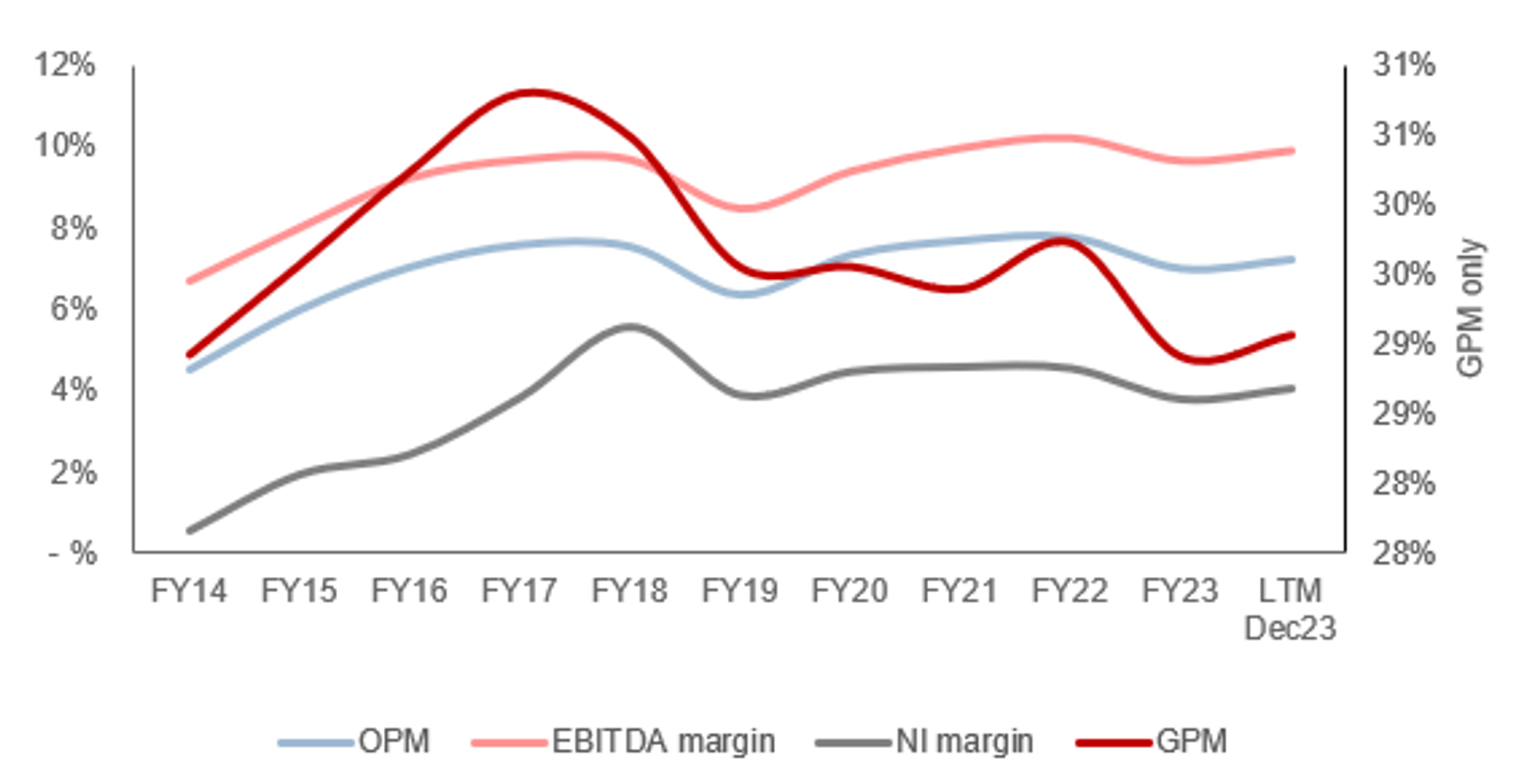

CENT’s margin development has been impressive, with EBITDA-M increasing from 7% in FY14 to 10% in the LTM period. Improvement post-FY18 has been limited, likely suggesting the company is not able to further extract any material operating cost leverage. We attribute this to increased competition, forcing the business to relinquish any gains at a GP or OP level.

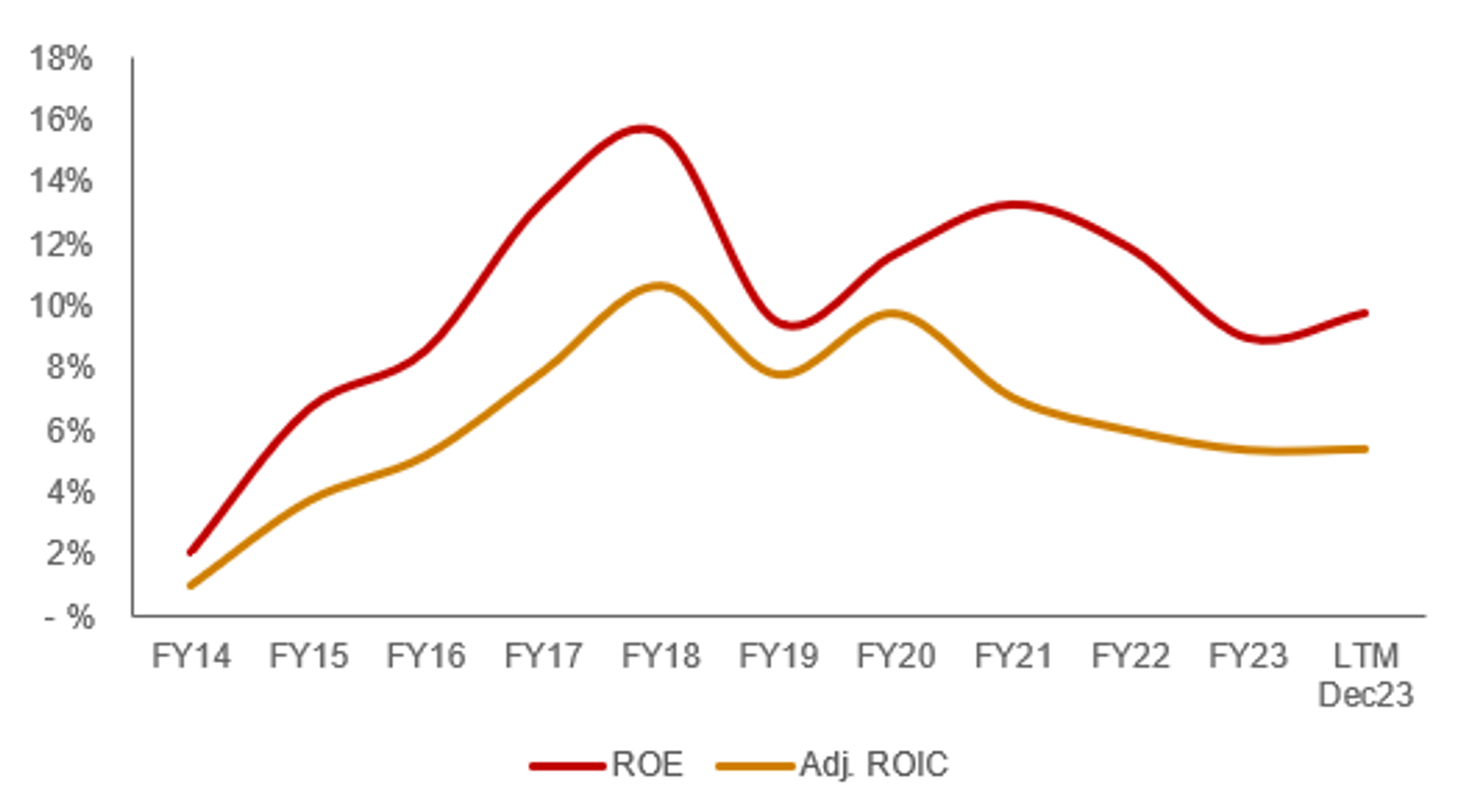

CENT is conservatively financed, with an ND/EBITDA ratio of 2.3x. With interest comprising ~2% of revenue, we see limited concerns around liquidity or solvency. Management’s capital allocation policy is weighted heavily toward M&A, with over 60 acquisitions in the last 30 years and over $1b spent in the last decade.

We are highly supportive of an M&A strategy, so long as it is accretive or neutral on a margin basis and ROE basis. The latter is usually forgotten (or neglected) by Management teams, contributing to shareholder value destruction while the business is seemingly performing better. This is not the case for CENT. Its ROE has progressively improved over the last decade, only softening in line with demand, which is the volatility we would expect.

Management believes the pipeline is strong, positioning it well to supplement organic growth with further M&A.

Capital IQ

Capital IQ

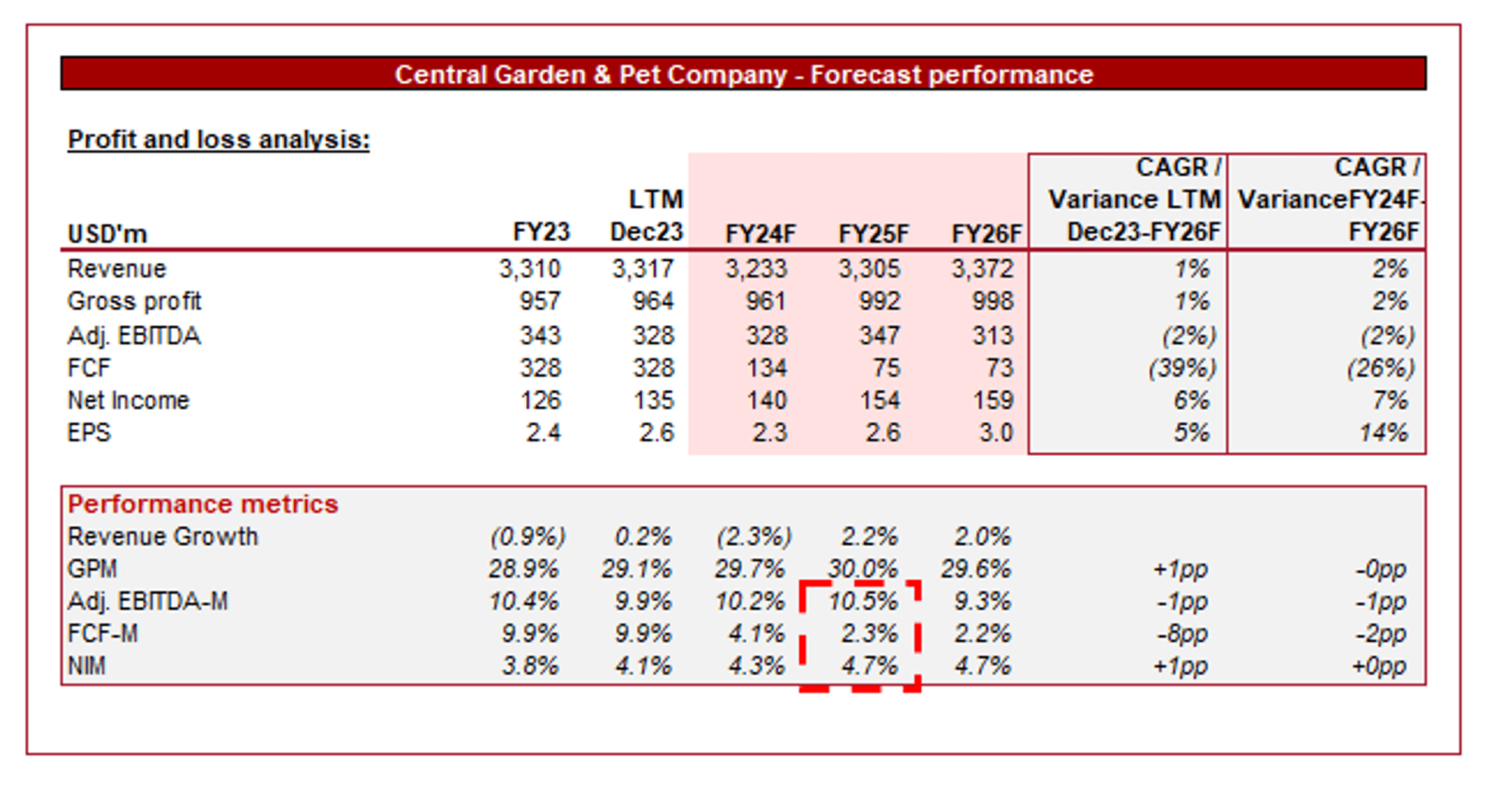

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting mild growth in the coming years, with a CAGR of +1% into FY26F alongside flat margins. We believe these forecasts are conservative, as they seemingly do not reflect the impact of M&A or its broader organic growth trajectory. Given the limited margin improvement in recent years and the near-term headwinds faced, the margin assumptions appear reasonable.

Industry analysis

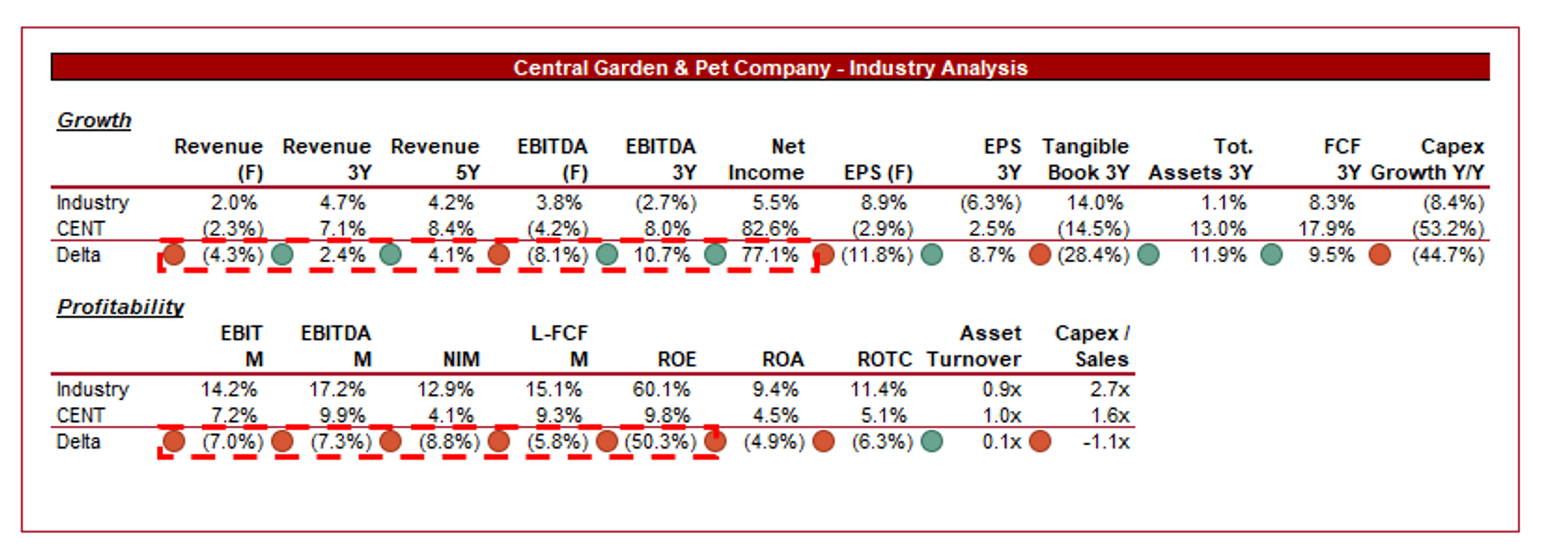

Seeking Alpha

Presented above is a comparison of CENT's growth and profitability to the average of its industry, as defined by Seeking Alpha (12 companies).

CENT performs moderately relative to its peers but is not a standout performer. The company’s growth has been comparable to its peers, attributable to its ability to price well in a high inflation environment, alongside operational excellence and acquisitions.

The company’s area of weakness is its margins, as despite noticeable improvements, it is materially lagging behind. This is partially due to the peers it is grouped with, the majority of which are significantly larger and operate in a number of verticals, allowing for superior unit economics.

Valuation

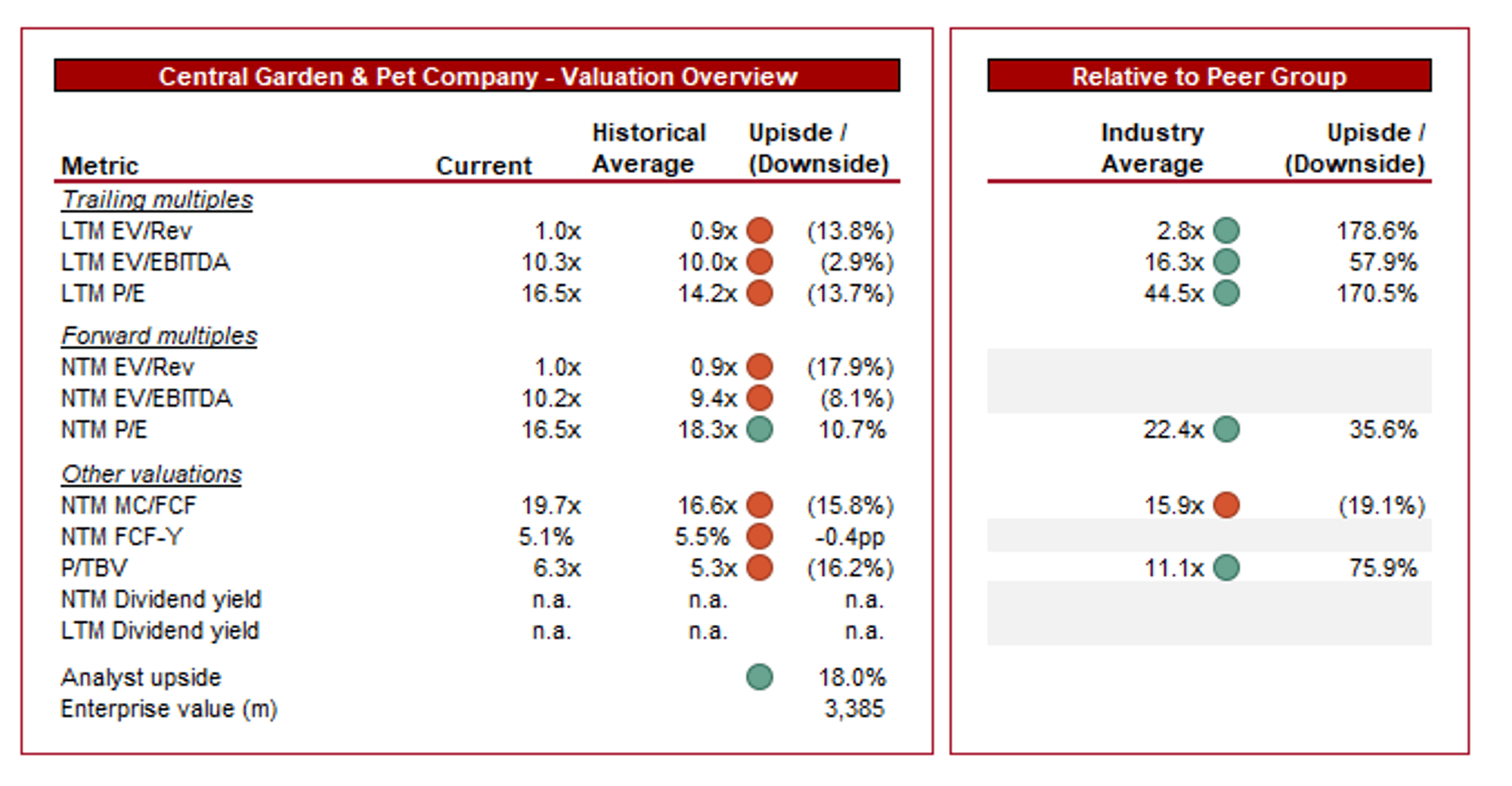

Capital IQ

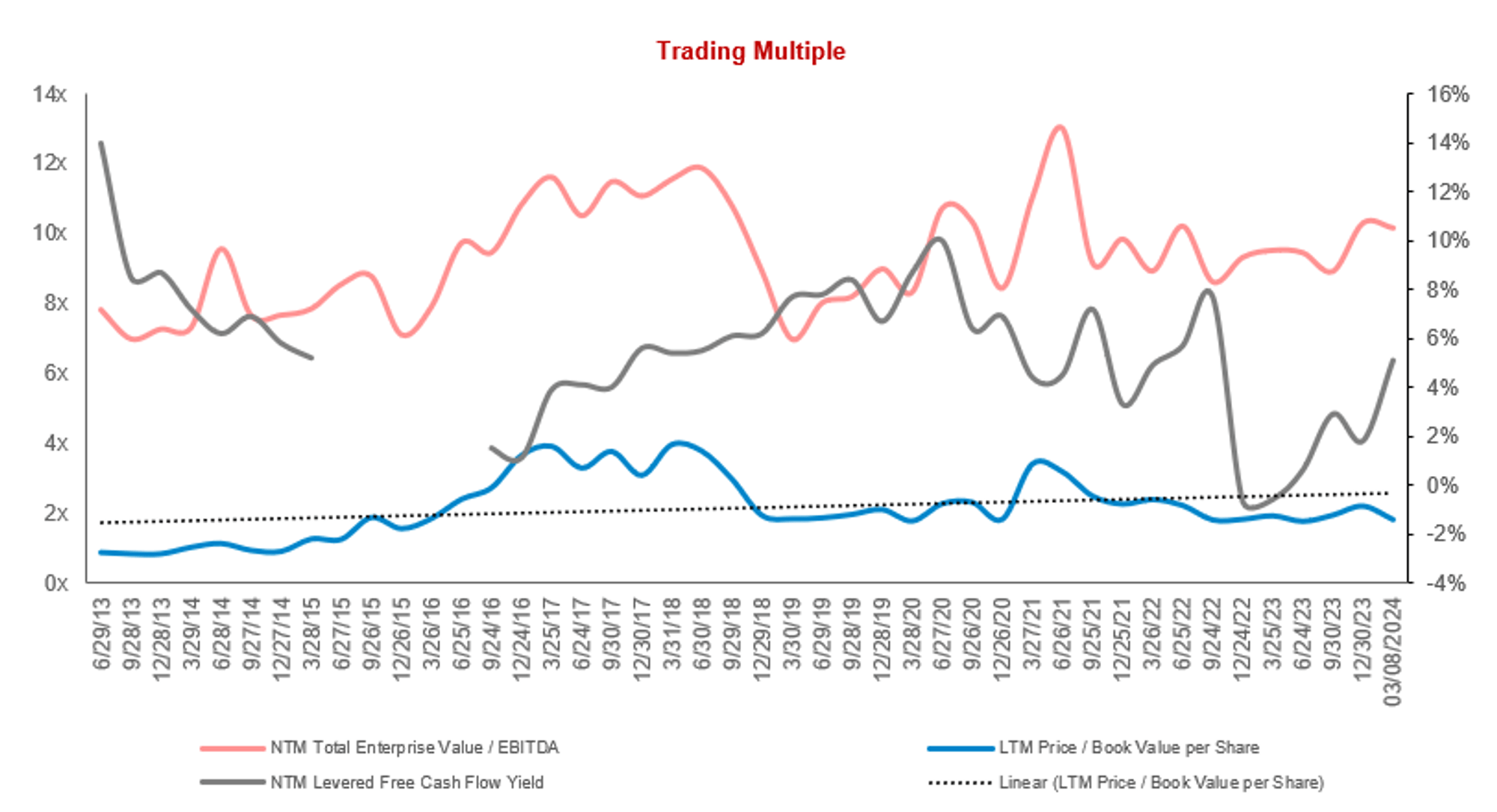

CENT is currently trading at 10x LTM EBITDA and 10x NTM EBITDA. This is a premium to its historical average.

Given the company’s positive development, namely increased market share and the broadening of its moat, alongside financial improvement in factors such as margins, we could see an argument to suggest a premium is justifiable. This said, any potential for this will be offset by near-term headwinds should an investor seek to buy in today, for which the time frame is still uncertain.

Further, CENT is trading at a substantial discount to its peers on an LTM EBITDA basis (~58%) and on a NTM P/E basis (~36%). A discount is justifiable in our view given the limited scope to revert to the average on margins, while achieving outperformance on growth in a mature industry is limited. This said, at the current discount size, we believe the stock is undervalued on this metric.

Overall, the business is likely undervalued, although not to a material extent.

Capital IQ

Key risks with our thesis

The risks to our current thesis are:

- [Upside] E-commerce penetration and transition to online retailing

- [Upside] Continued product innovation and market expansion.

- [Downside] Adverse impact of economic downturn on consumer spending.

Final thoughts

CENT is a high-quality business in our view, with limited issues. The company is growing well, underpinned by strong tailwinds and attractive industry characteristics, such as the robust demand for pet products. We expect continued success in the years to come. This said, with tailwinds extending into FY24 and limited upside at its current valuation, we do not believe the current timing is correct.