ClaudioVentrella

Bristol Myers Squibb (NYSE:BMY) shares have been plunging recently over concerns about patent expirations, and growth prospects. In 2022, this stock was trading for more than $80, but it has been nearly cut in half since then. This has piqued my interest since I like to be a contrarian investor and seek out stocks that might be victims of excessive negativity, which seems to happen from time to time, and even to the best stocks. For example, just about 18 months ago, Meta Platforms (META) was trading for less than $100 per share, and now it is very close to $500 per share. NVIDIA (NVDA) was trading for about $140 per share in 2023, and now it is trading for more than $900 per share. It was not easy to buy Meta Platforms when it was trading below $100, because at that time investors were concerned that it had very little future growth potential, and the same was true for NVIDIA.

So, all of this has me wondering about whether or not investors have just become way too negative about Bristol Myers Squibb and its growth prospects. Let's take a closer look:

The Chart

The chart below shows a longer-term view of this stock as it goes back to 2012. What's notable is that since 2013, this stock has never gone below the 200-week simple moving average (represented by the brown trendline), except for just recently when it dipped below this level. This could mean right now is the best buying opportunity in more than a decade because every time this stock has been even remotely close to the 200-day simple moving average, it was a buy and the stock ended up rebounding.

I think it's also notable that in late 2022, this stock was trading for more than $80 per share, and now it's nearly half of that level. I don't think this business is half of what it used to be just a couple of years ago, but the market does. However, as we know, the market gives us big buying opportunities, and it is usually not easy to take advantage of these opportunities because they typically come when the stock has had a large decline and there's plenty of negative sentiment. This seems to describe Bristol Myers Squibb right now, and this stock just hit a new 52-week low.

Finviz.com

The Pipeline Issues And Future Growth Plans To Grow Earnings

Bristol Myers Squibb has seen sales of Revlimid decline as this blockbuster cancer treatment went off-patent in 2022. Plus, its anti-stroke treatment known as Eliquis is going off-patent in 2026. However, it still has numerous candidates that are not seeing patent expirations any time soon. Furthermore, Bristol Myers Squibb has been aggressively acquiring high potential companies which are designed to offset patent expirations and add to growth. For example, in 2023, it announced it would buy Karuna (KRTX), RayzeBio (RYZB) and Mirati (MRTX). These companies have candidates that could be keys to reigniting growth for Bristol Myers Squibb.

Earlier this year, Bristol Myers Squibb announced it would eliminate around 2,200 jobs as part of a $1.5 billion plan to reduce expenses. There are one-time charges that this plan is incurring, which is one reason why 2024 is not expected to be a highly profitable year, but one of transition. Acquiring a number of high-potential drug candidates and reducing expenses are all part of the plans to grow earnings in the future.

Earnings Estimates And The Balance Sheet

Analysts expect Bristol Myers Squibb to earn $0.56 per share in 2024, on revenues of roughly $46 billion. However, earnings are expected to rebound significantly in 2025, with estimates at $6.94 per share, and revenues at just over $46 billion. In 2026, this company is expected to earn $6.30 per share on revenues of $43.85 billion. This is clearly not an earnings growth stock, and yet I still find it compelling because the company is only trading for about 7 times estimates for 2025.

In terms of the balance sheet, it has $57.46 billion in debt and around $9.67 billion in cash. I would prefer to see less debt, but it still has an "A2" credit rating from Moody's.

The Dividend

This company pays a quarterly dividend of $0.60 per share, which at $2.40 per share annually, provides a yield of nearly 5.5%. Ten years ago, the quarterly dividend was $0.36 per share. This shows the dividend has nearly doubled in this time span. In addition, the dividend looks secure since it represents a payout ratio of about 34% on 2025 earnings estimates.

The dividend yield of nearly 5.5%, is very attractive and this is even a bit more than what most money market funds currently yield. But, even more importantly, money market yields are likely to plunge over the next couple of years as interest rates are likely to be lowered by the Federal Reserve. There's a big debate on when the Federal Reserve is going to lower interest rates, but it seems that this is a near certainty sooner or later.

Earlier this year, the Federal Reserve released forecasts (otherwise known as the Fed dot plot), which suggest a 2.25 point drop in the Fed Funds rate by the end of 2026. This could reduce the Fed funds target rate from the current range of 5.25% to 5.5%, to a range of 3% to 3.25%, in the next couple of years. I think investors will show a lot more appreciation for the nearly 5.5% yield that Bristol-Myers Squibb provides when interest rates on money market funds are potentially 40% lower in a couple of years.

AI Could Be A Huge Positive For Bristol Myers Squibb

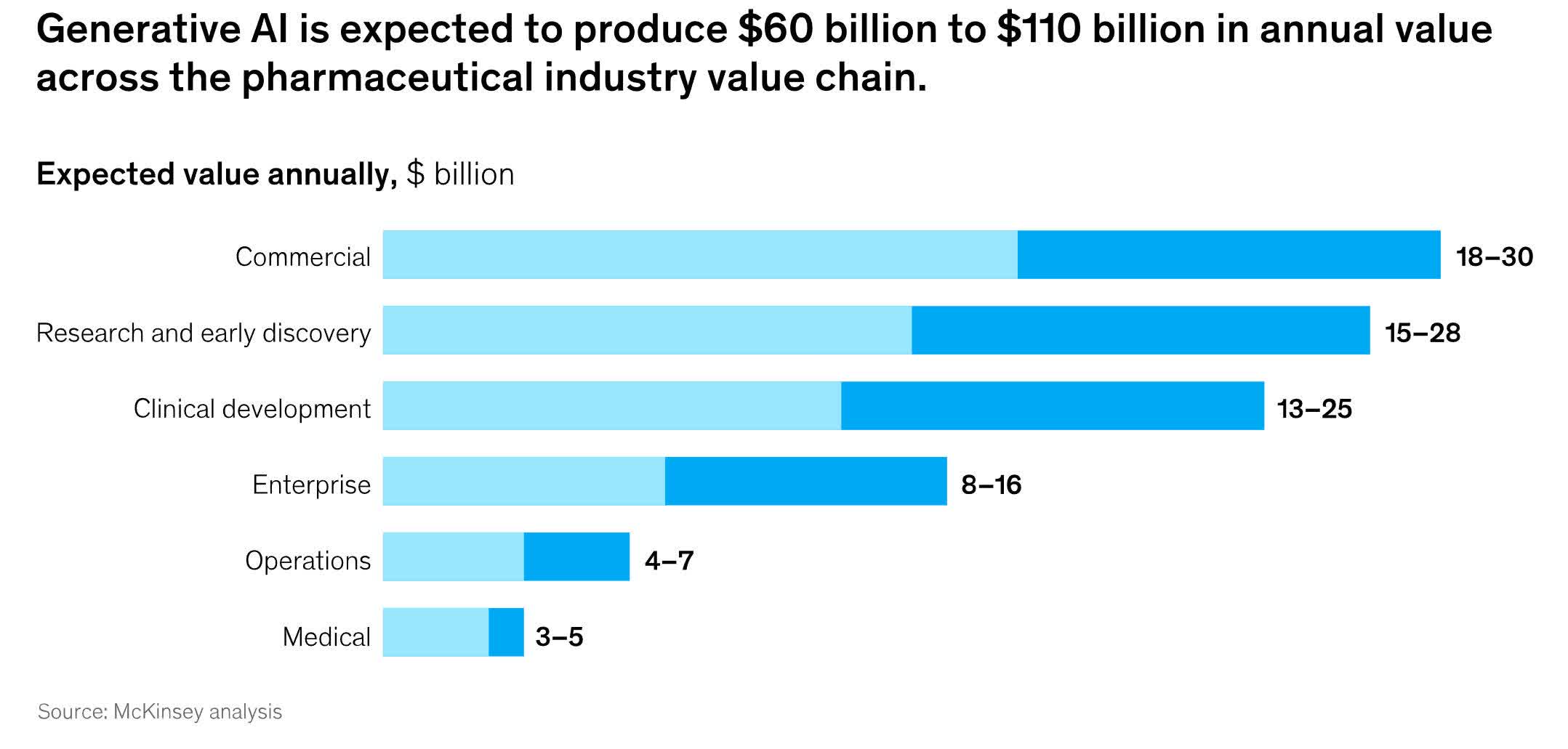

AI could be a major development and beneficial factor for the pharmaceutical sector. Generative AI is expected to enable more efficient clinical trials. This should also lead to expedited regulatory approvals. The McKinsey Global Institute estimates that Generative AI could produce $60 billion to $110 billion annually in value for the pharmaceutical industry.

McKinsey & Company

What I Like About Bristol Myers Squibb

I like that I can buy this stock at a level that has not been seen in over a decade in terms of the 200-week simple moving average. Being able to buy at just around 7 times earnings estimates and with a yield that beats money market fund rates, is also very attractive.

While patent expirations are a challenge for all the companies in this sector, the patent protection they have initially when introducing blockbuster drugs is very valuable, and I have no doubt that Bristol-Myers Squibb will develop and also acquire more blockbusters in the future, just as they have historically. It's tough now because all we know is that some upcoming patent expirations create uncertainty, and we don't yet have all the answers as to how successfully some of the recently acquired candidates will fare. But there is enough in the pipeline for me to be hopeful.

Another positive is that this sector is relatively recession resistant. Many investors seem to believe that the Federal Reserve will be successful with a soft landing, but that hasn't always been the case in the past. Jamie Dimon, CEO of JPMorgan Chase (JPM) is skeptical of the soft landing scenario, and he might end up being right. If the economy gets tough, high-flying growth stocks could experience sharp declines, while more steady industries like pharmaceuticals could continue to see strong demand.

With a big section of the U.S. and global population aging and with people living much longer these days, there is, and will be more demand for drugs and treatments going forward. AI might also lead to breakthroughs that extend longevity even further, which could also boost demand for drugs and treatments.

Potential Downside Risks

Bristol Myers Squibb is facing challenges now, and the stock seems to be regularly hitting new 52-week lows. When investor sentiment is extremely negative, a stock can overshoot to the downside, and it is hard to say when this stops. This stock already seems very undervalued, but as we saw in the past with Meta Platforms and other stocks, when investors have growth concerns, a stock can go down to levels that make little sense. This means the bottom might be even lower for this stock.

Another major potential downside risk to consider, in addition to the patent expirations, is the possibility that the acquisitions this company makes, may not perform as well as expected, and some candidates could fail. We are also in an election year, and this could keep pressure on drug companies to lower prices.

In Summary

There are challenges and negatives to consider, but with a nearly 5.5% yield and a price to earnings multiple of just around 7 times for 2025, I believe a lot of bad news is already priced into this stock. With this stock just having made a new 52-week low, additional weakness has to be considered. For this reason, I am only buying a small partial position to start with, and I will accumulate this stock over time. At some point, just as with other stocks that took a major beating when growth prospects were in doubt, I believe investors will reconsider the investment opportunity in this historically successful company. In the meanwhile, the generous yield will reward investors with money market-like payouts while waiting for a higher share price.

No guarantees or representations are made. Hawkinvest is not a registered investment advisor and does not provide specific investment advice. The information is for informational purposes only. You should always consult a financial advisor.