robas

Investment thesis

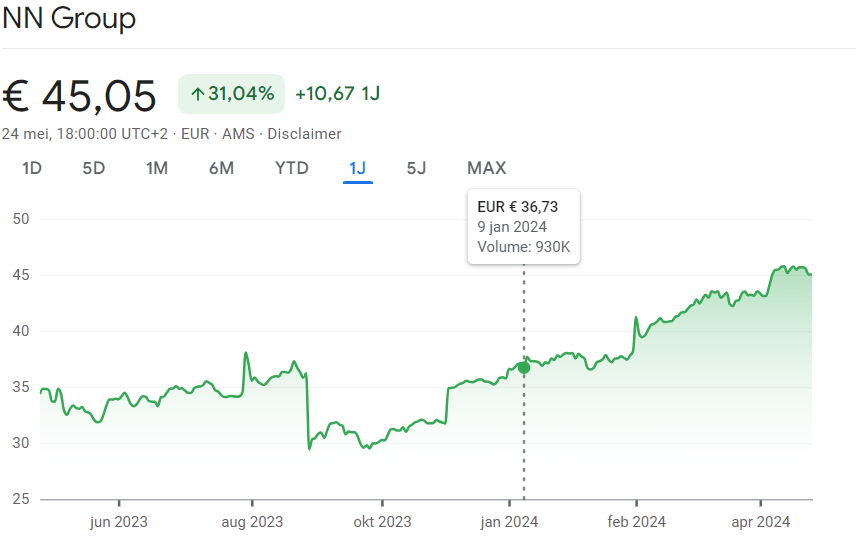

At the moment, NN Group (OTCPK:NNGPF)(OTCPK:NNGRY) is one of the largest positions in my portfolio. Last year, there were plenty of opportunities to buy NN at a really attractive price. As can be seen, even after the settlement (announced on January 9), there was still sufficient upside when it comes to the share price.

NN share price development (Google finance)

When I look back on my last article, the investment thesis seems to have turned out well. Is it too late to put your money in NN? I don't think so! At the current share price, the dividend yield of 7.1% is still attractive. A dividend yield of +7% can be seen as a high-yielder, but it is one with sufficient dividend growth left. The dividend per share in FY 2023 grew a whopping 15% compared to FY 2022, and it is likely there is still more dividend growth to come. In addition, they also do a hefty amount of share buybacks, so you get a total shareholder yield of +9% right now.

Today, I would like to update my investment thesis based on the latest information, so let's begin!

Growth drivers

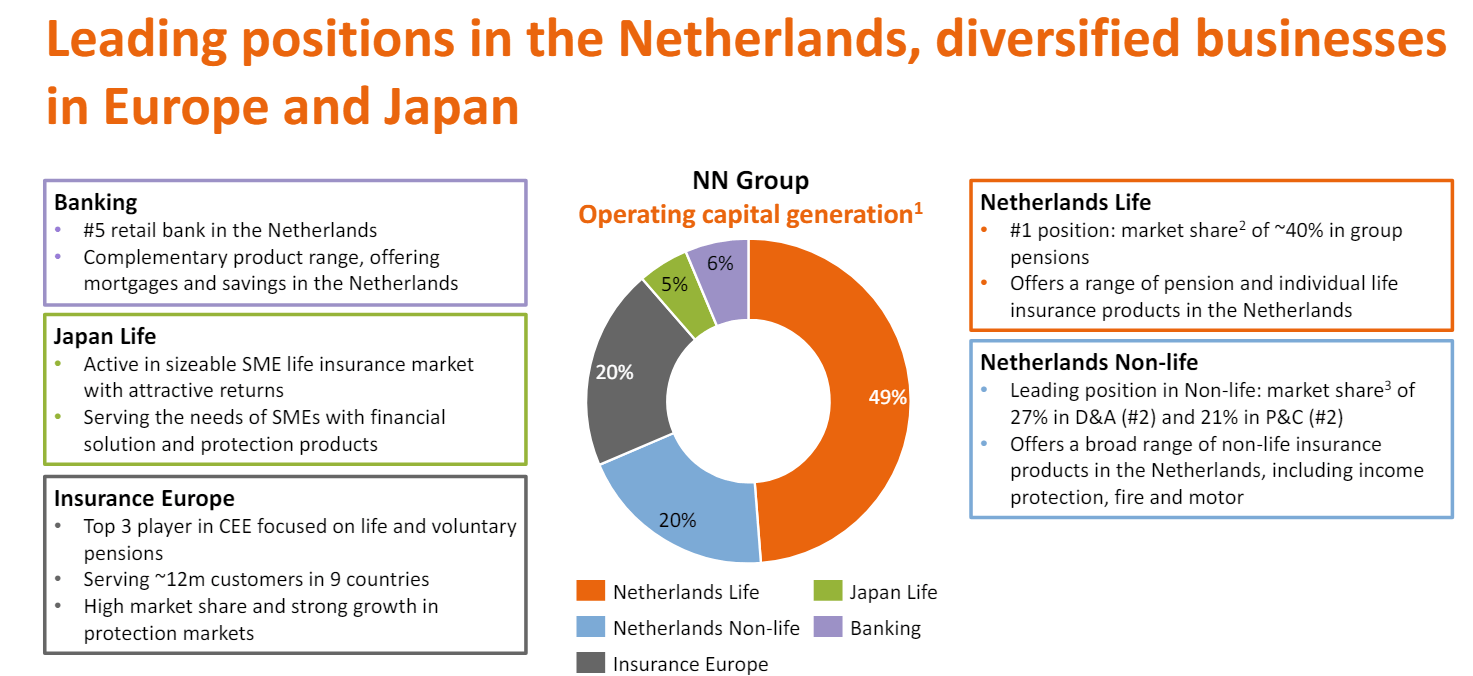

Don't expect enormous growth from a company like NN. As you can see in the slide below, a large portion of their operating capital generation is coming from the Netherlands. The Dutch insurance market is already highly penetrated, but there are certainly some opportunities to mention to steadily grow their business.

OCG distribution (NN company profile)

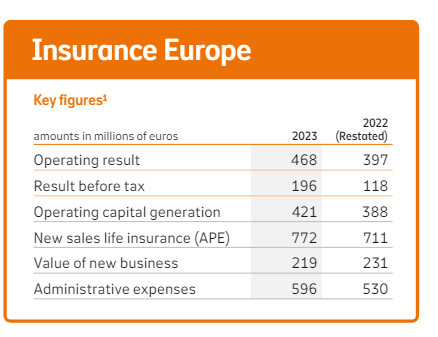

Insurance Europe is one of them. In FY 2023 Insurance Europe showed some strong underlying growth with higher sales in Central and Eastern Europe, especially in countries like the Czech Republic, Poland and Hungary. In this part of the world there is an increased awareness when it comes to protection products and since NN has a leading position in life protection in Europe, it is likely that the company is going to benefit from this trend.

Insurance Europe overview (FY 2023 annual report)

Secondly, the new pension system in the Netherlands could also be a potential growth driver for NN. On May 2023, the Dutch Parliament approved the new Pension Act and there will be a transition period until 1 January 2028. NN is the most dominant player (40% market share in group pension) in the Dutch pension system and started its preparations early on. In this situation, it is very useful that NN is a heavyweight because it will be a lot harder for small and medium-sized pension funds to adapt to the new laws and regulations. This means that potential buyouts are looming and NN can benefit from this.

Based on the 2023 annual report, the first new pension contracts were already concluded and administered. What is also a positive signal is that the net inflows in FY 2023 are at record levels (€2.3 billion compared to €2 billion in FY 2022). NN also sees a growing demand for personalized pension products and financial planning tools.

Financial Performance

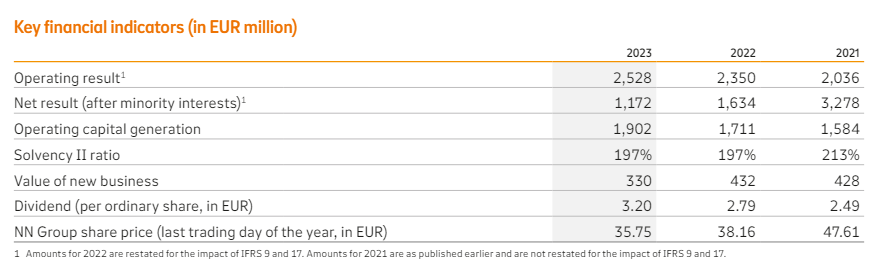

NN provides a detailed update on their financial performance twice a year. Today I would like to go through the most recent results with you based on the numbers from the FY 2023 annual report.

These are the most important metrics in a nutshell.

key financial indicators NN (FY 2023 annual report)

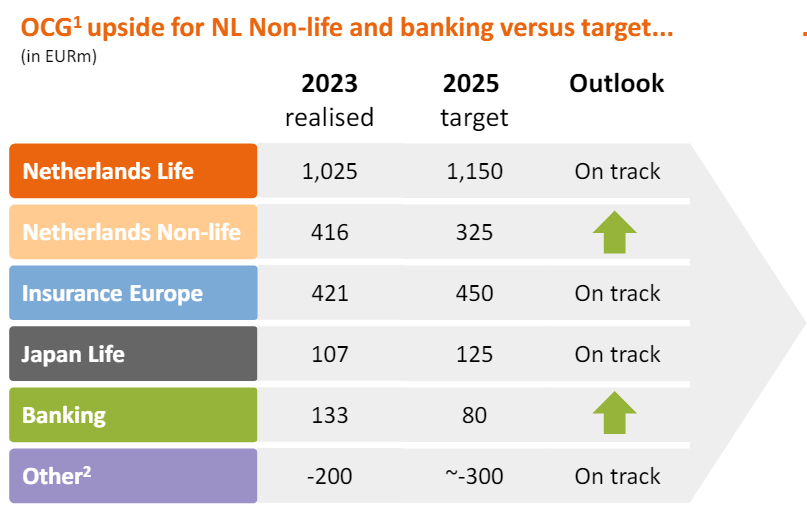

The OCG is one of the most important financial metrics for NN. The company managed to increase the OCG by 13% on a year-over-year basis, which is impressive. With a total OCG of €1.9 billion, they already exceeded their 2025 target of €1.8 billion, which caused them to increase the target to €1.9 billion.

FY 2023 results vs 2025 target (NN company profile)

NN reported an overall strong business performance. Their Netherlands non-life segment did really well this fiscal year. As stated earlier, Insurance Europe did great, and their banking activities benefited from higher interest rates. Netherlands Life was the biggest under-performer, with a -10.2% in OCG year-over-year. This was mainly due to the negative effects of the financial markets. However, the company expects to be back at 2022 levels in FY 2025.

Netherlands Life vs Non-Life (FY 2023 annual report)

So, in my view, NN is doing well. Their business mix is getting more diversified because of the meaningful growth in Insurance Europe and Netherlands Non-Life insurance, which is a good thing. Due to the financial market headwinds, the Netherlands Life business segment has under-performed, but this was to be expected. This segment could also perform better in the future with the new Dutch pension system, although this growth may take some time to show up.

Solvency ratio

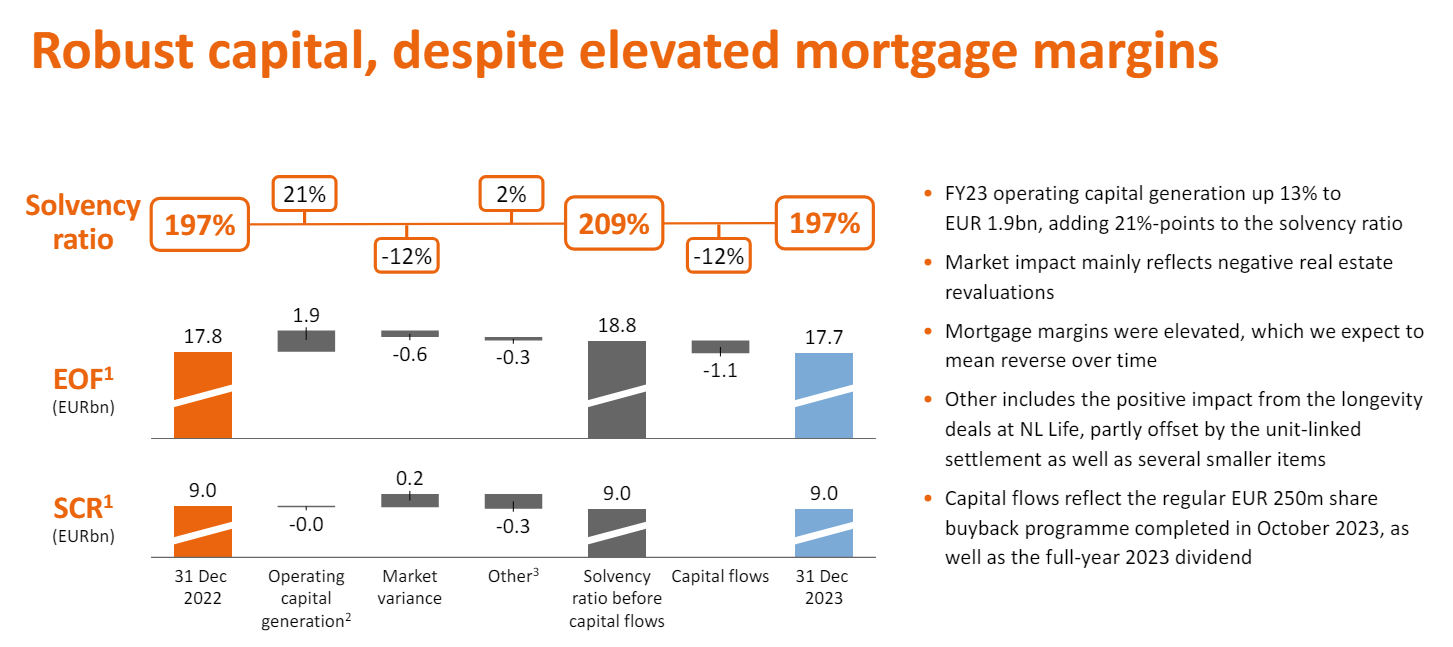

The solvency ratio of 197% is exactly the same compared to last year. The positive part was the increasing OCG, but the solvency ratio was negatively impacted by capital outflows to shareholders combined with the final settlement agreement on the unit-linked insurance policies. Additionally, the negative real estate revaluations also had a negative impact to the solvency ratio.

Solvency ratio FY 2023 (NN group company profile)

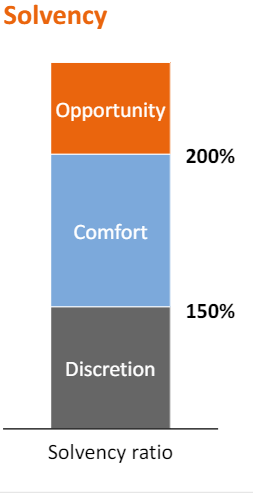

Despite the turbulent year, NN was able to keep its solvency ratio in good shape. It is important for the investment thesis that NN stays in the comfort or opportunity zone.

NN solvency (NN company profile)

This is a quote from the 2023 annual report of what they mean by the comfort zone.

NN Group defines a comfort zone between 150%-200% Group Solvency ratio where NN Group intends to pay a progressive dividend per share and execute an annual share buyback. In the case of a Group Solvency ratio sustainably above 200%, there is an opportunity to increase the share buyback further.

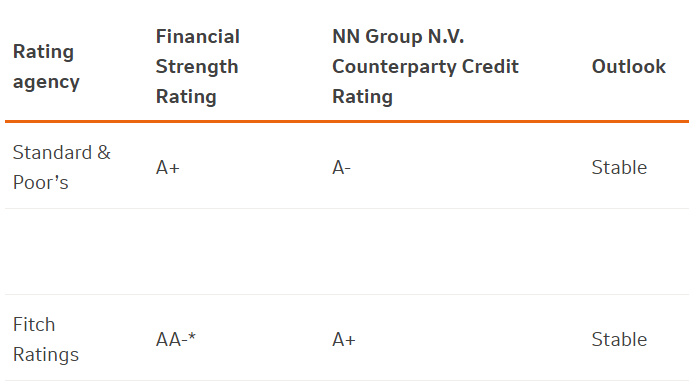

NN also enjoys an A+ credit rating from S&P Global. With an "Excellent" score on Financial risk and a "Strong" score on business risk, it looks like NN is in a good financial position.

Credit rating scores (NN group investor relations)

Capital return policy

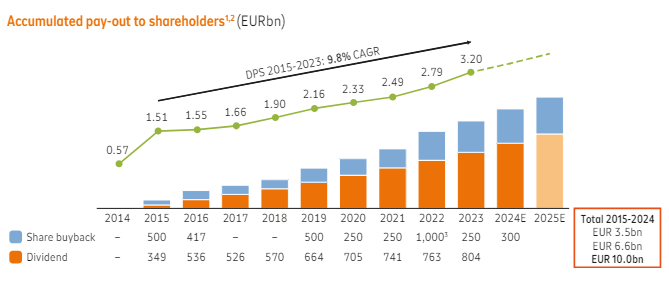

The capital return in the form of dividends and share buybacks is the bread and butter of my investment thesis. For all the USA-based readers that are interested, dividend tax is withheld at the rate of 15% from gross dividends distributed.

At the current share price, the dividend yield is 7.1%. This is quite a bit lower compared to last year, but in my view still attractive. Especially if you take the dividend growth into account.

Capital return policy (NN company profile)

I don't expect 9.8% growth to be the standard for the future because the growth trend in FCF is moving more towards mid-single digits.

Secondly, the amount of share buybacks has also been increased. This has increased from €250 million to at least €300 million. Purely hypothetical, if we use €300 million on a total market cap of €12.83 billion, we are still talking about 2.3%. Therefore, the total shareholder yield would still be 9.4% at current prices. Not bad, if you ask me.

Valuation

NN is trading at a TTM price-to-book ratio of 0.58, which is significantly lower than the sector median of 1.14. This could be an indication that the company is undervalued. However, this is not entirely unjustified. NN has a TTM return on equity of 5.3%, which is just slightly above its own 5Y average, but significantly below its sector median of 10.61%. This seems to be priced in by the market.

To calculate a fair value for the business, the dividend discount model has been used. This model is well applicable for NN as it is a stable business with a clear ambition to grow the dividend for the foreseeable future.

The last time I used a dividend of €3.12 for FY 2023. This ultimately became €3.20 (€1.12 interim dividend + €2.08 final dividend). I think the expected dividend per share of FY 2024 will be around €3.40, which is about 6% higher compared to FY 2023. This is in line with the used dividend growth rate of 6%, and it is also significantly lower than the 9.8% dividend per share CAGR it achieved from FY 2015 to FY 2023. Personally, I prefer to be a bit more conservative in my assumptions, and it will also be difficult for a company like NN to keep achieving high single-digit dividend growth. Based on the 2023 annual report, the company itself thinks it can similarly grow their FCF in the mid-single digits long-term, which could be linked to their dividend growth. Last but not least, I used a rate of return of 12.5% because this is my personal rate of return on my investment.

This comes to a fair value of €52.30 per share. Compared to the current share price of €45.05, NN is 16% undervalued.

Conclusion

Based on my updated investment thesis, I think NN is still a BUY. The company is performing better than expected and there are still opportunities for the business to grow further in the future. The combination of dividend yield, dividend growth and share buybacks are still attractive and there is also upside from a share price point of view.

Of course, there are several investment risks to consider before investing in NN. Inflationary pressure, geopolitical friction and higher interest rates are factors that can cause headwinds for NN. All these factors can have an indirect or direct effect on NN's overall financial picture. To focus specifically on the investment thesis, all these factors together have an impact on the valuation of NN's assets and liabilities (for example negative real estate revaluations), and could lead to a more volatile solvency ratio. In an unfavorable situation, this could have severe consequences for their capital return policy.

Despite the first positive signals regarding the pension business with the record net inflows, it is difficult to determine what the real impact of this new system will be on NN's profitability. Further details need to be established in secondary legislation, and the actual implementation is expected after the start of 2026. So, time will tell.

If we evaluate all the pluses and minuses, I think that NN can still be a solid long-term investment for the dividend growth- and income investor.

I will come up with another update later this year. The first half-year results will be published on August 15, and I will provide a new update on NN's progress afterwards.

Happy investing everyone!

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.