Warut1/iStock via Getty Images

Introduction

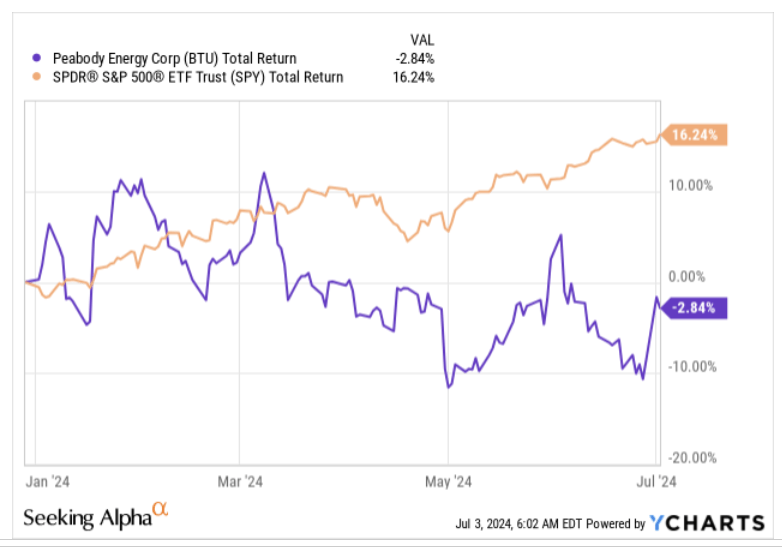

The stock of Peabody Energy Corp (NYSE:BTU), a global producer of coal for the energy and steel industries, has experienced a volatile 2024 and hasn’t ended up making a great of progress through the year. Whilst the prime benchmark for US equities has notched up steady gains of 16%, our stock in focus, has lost ground by nearly 3%.

YCharts

Back in October 2023, we had actually written a piece on BTU, covering some of the major fundamental and technical sub-plots, and nearly nine months on, we are not overly compelled to revise our neutral stance on the stock, even though there have been a few developments since.

Keep An Eye On Newsflow Linked To Anglo-American's Grosvenor Mine

As mentioned in our previous article, Peabody Energy’s Metallurgical mining division is a key area of focus, as it accounts for the largest share of group EBITDA and also has the highest EBITDA margin per tonne.

In Q1 the performance wasn’t too pleasing with volumes taking a hit on account of a planned longwall move at their Metropolitan mine, coupled with some unexpected outages at their Coppabella/Moorvale joint venture, which also left an adverse mark on the cost front. Besides, on account of mine sequencing activities at the JV, the company also mined some low-quality coal which ended up impacting the sales mix.

When the company reports Q2 earnings roughly a month from now, it’s reasonable to expect a pickup in volumes in this division (potentially 500,000 tonnes higher) from the Q1 levels, as the longwall move has been sorted, and further progress on mine sequencing at the JV, should also leave a salutary mark on the sales mix.

Beyond that, current pricing in the met coal market could be keenly driven by developments coming out from Anglo-American’s Grosvenor steelmaking coal mine, where production has been suspended on account of a fire. Grosvenor plays a key role in seaborne met coal supply and was expected to contribute 3.5m tonnes this year to global supplies. Back in 2020, we saw something similar at the same mine, and that ended up resulting in an outage of 18 months! It’s difficult to ascertain how long Grosvenor will be offline, but this tightening of Australian met coal supplies is likely to reflect favorably on price realizations in Q3.

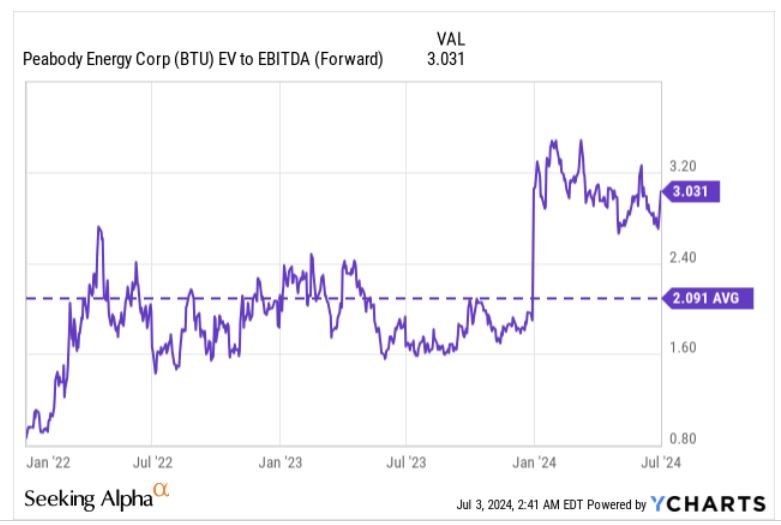

Valuations No Longer Look Cheap And Shareholder Yield Progress Could Be Capped

A notable development since our last article has been the shift in the valuation picture of BTU. Back in October 2023, BTU was priced at a forward EV/EBITDA multiple which was almost in line with its long-term average; now that scenario has changed with BTU currently priced at a premium forward multiple of over 3x, which translates to a massive 45% premium over its long-term average.

YCharts

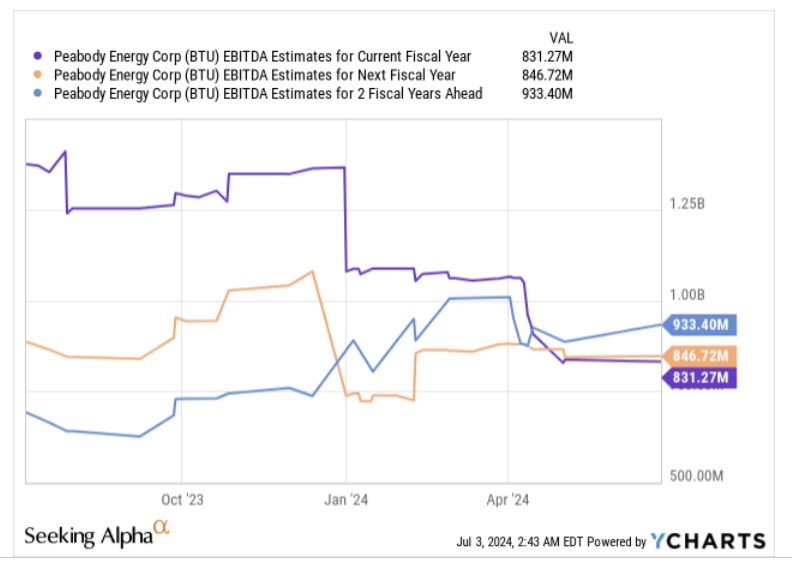

Admittedly, some investors may be open to paying that premium as the 3-year forward EBITDA outlook too has changed for the better, with FY26 now coming into the equation.

Previously, we were considering the time frame of “FY23 to FY25”, where group EBITDA was poised to decline by 25% CAGR; now, with the time frame of “FY24 to FY26” under consideration, we are looking at marginal EBITDA growth of +6% during that period (which is 2x the level of the EV/EBITDA multiple).

YCharts

Having said that, investors should also note that the FY26 EBITDA figure will still represent a 31% contraction from the group EBITDA that was generated last year ($1364m), and it’s perfectly fair to ponder if you should be paying a higher multiple for a lower threshold of EBITDA (particularly if that EBITDA appears to be growing from a low base).

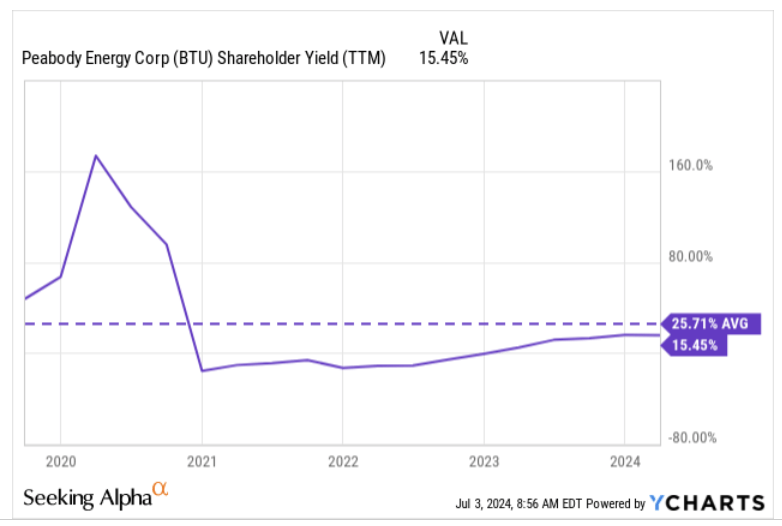

Investors may also want to note that whilst BTU's shareholder yield (a function of dividends, buybacks, and debt paydowns) has improved in recent months by around 400bps, at current prices, it is still below what the stock has averaged over the past 5 years.

YCharts

For the uninitiated, BTU’s target is to return over 65% of its available FCF to its shareholders by way of dividends and buybacks, and currently, FCF generation isn't quite robust enough. For context, the Q1 FCF was lower by 83% YoY.

Granted, operating cash flow should pick up in H2, but investors also need to recognize that after spending only $61.4m by way of CAPEX in Q1, the company is on course to spend another $314m over the next three quarters, implying a much higher quarterly CAPEX run rate of over $100m. As a result, one may not necessarily see meaningful FCF growth on a YoY basis by the end of FY24, which could end up impacting distribution and buyback momentum for the year.

Centurion Mine Redevelopment Initiatives Progressing Well

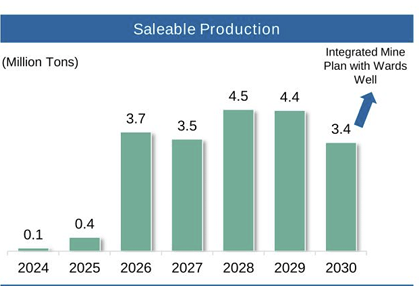

One of the major drivers for an uplift in the EBITDA growth (and CAPEX commitments), particularly in FY26, is the ongoing redevelopment of BTU’s Centurion Mine (previously known as North Goonyella) in Australia, which could see longwall coal production kick off from early 2026 (estimates saleable tonnes of 4m per year). Recently, we’ve seen the firm bring on board operators and maintenance personnel to prepare for underground development, and in the coming months, the plan is to fix gas drainage and other related infrastructure.

Even though full-fledged longwall production from Centurion will only start in around 18 months, BTU has already commissioned development equipment linked to this project, and some development coal would likely have been procured in Q2 already. In fact, note that for the whole of H2-24, BTU still plans to sell around 100KT of coal from here, with another 400KT of development coal in FY25 before hitting its FY26 longwall targets.

B.Riley Institutional Investor Conference

The texture of coking coal that will come out from Centurion is likely to be of high quality, and the fact that BTU has already locked up a 2-year contract (with a North Asian customer) for just the development coal batches, speaks to the level of interest for the product. By “high quality” we mean coking coal with low ash (less than 10% which is not common to see) and low sulfur (which is important for steel mills to meet environmental regulations) content, yet having high hot strength (of over 68 CSR or Coke strength after reaction).

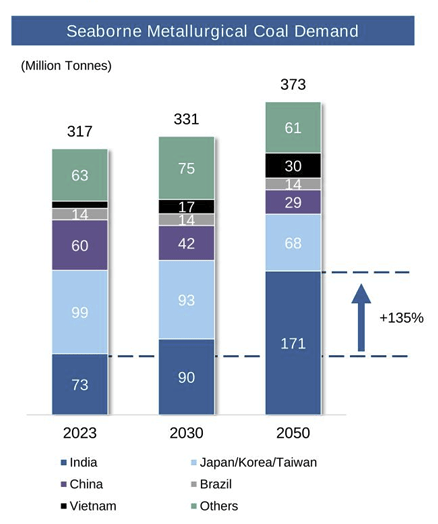

We can see Centurion’s premium grade coal has great utilitarian qualities in regions such as India, where steel mills often struggle with domestic coal with high ash and sulfur content. As far as steel production is concerned, India is the region to watch, as it is currently the second-largest steel producer in the world, and is poised to double its steel production to 300 million MT by the end of this decade. India is currently “ almost completely reliant on imported coking coal”, and that threshold of steel production could see India import around 90 to over 100 million MT of coking coal from abroad (by 2030). Australia, where Centurion is based, already serves as the predominant source.

S&P Global

B.Riley Institutional Investor Conference

Closing Thoughts - Charts Look Neutral With A Slight Bullish Tilt

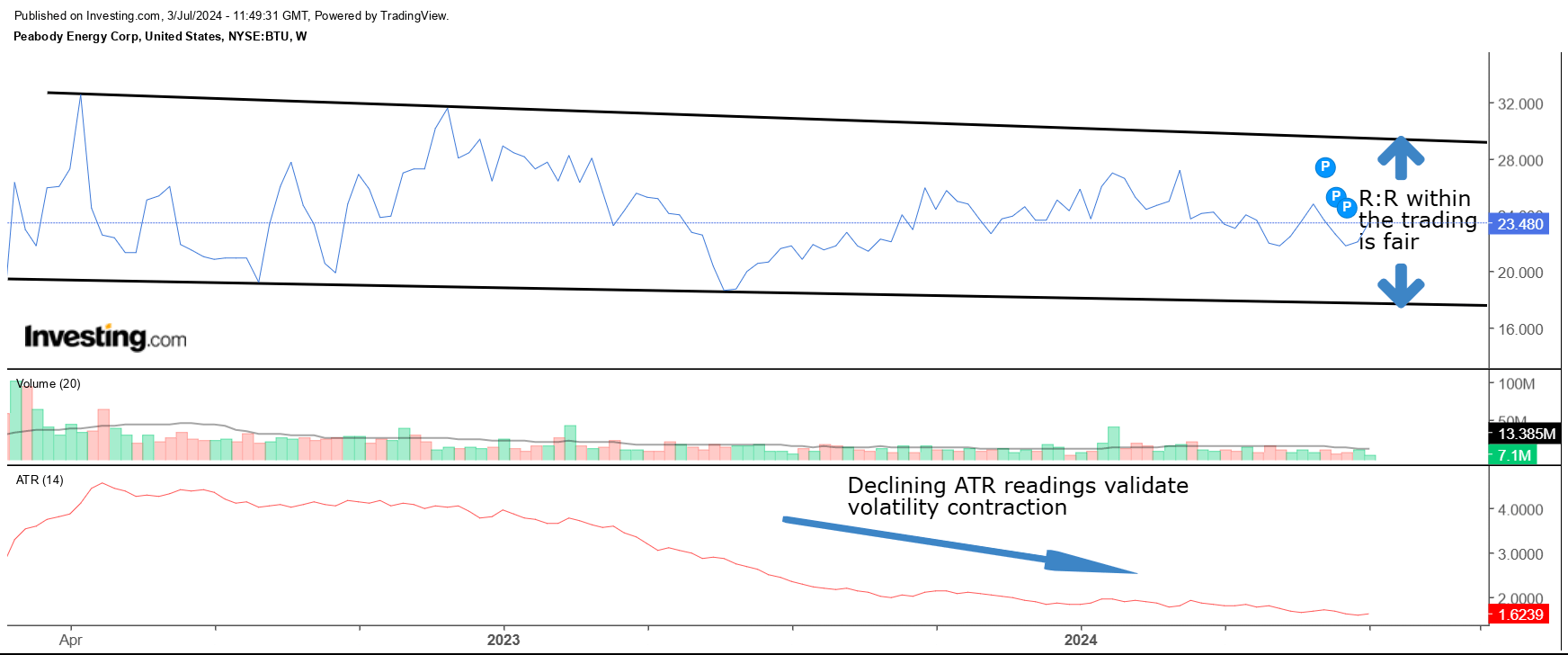

The broad takeaway from BTU’s standalone chart is that this stock has become a trading play that is likely to chop around within a certain range. Given this backdrop, we think investors should pay particular attention to the risk-reward within the trading range

BTU’s weekly price imprint since 2022 shows a stock experiencing significant volatility contraction, which is supplemented even further by the ATR (average true range) indicator more than halving during the time period in question.

Investing

When a stock is stuck in a trading range, you want to buy it when it is closer to support or when the reward-to-risk equation (the gap in the CMP vs resistance, relative to the gap in the CMP vs support), is well above 1x. Right now, as things stand, the reward to risk is roughly fair at 1x.

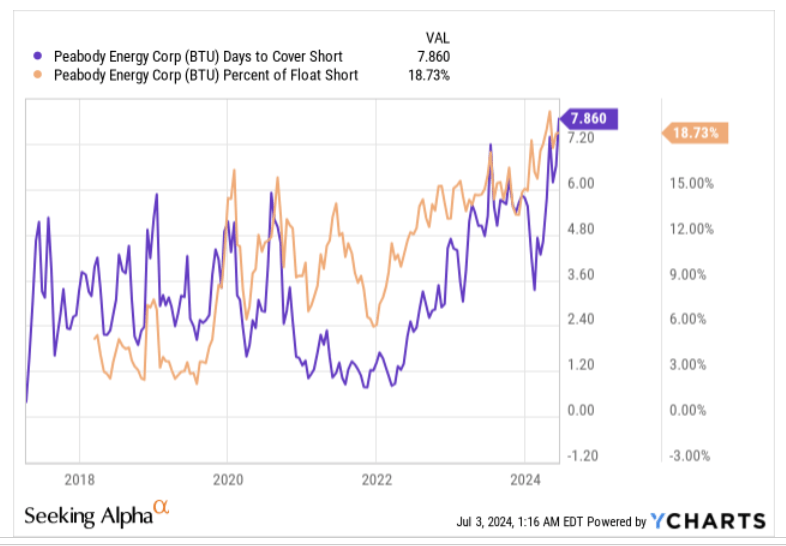

Having said that, some long speculators may be inclined to bet on a bout of short covering, as the percent of float that is short is quite elevated (at almost 19%), coupled with a record high days-to-cover of almost 8x, which won’t necessarily be easy for the shorts to cover.

YCharts

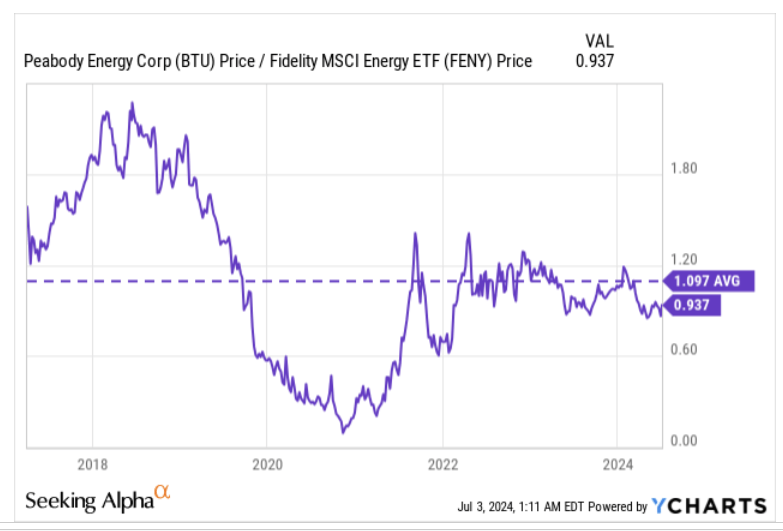

Also, if we switch our attention to how BTU is positioned relative to its peers from the broad energy sector, we can see that its current relative strength ratio is around 14% lower than its long-term average, offering some scope of mean-reversion.

YCharts

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.