Klaus Vedfelt

The bear camp warned us for months about "sticky" inflation and the higher-for-longer interest rates that would accompany it, until the disinflationary trend resumed, following a pause during the first quarter of the year. They then pivoted to warnings about growth, which softened dramatically from last year's levels, indicating that a recession was on the horizon, but that hasn't panned out.

The latest warning comes in the form of an AI-fueled bubble in technology stocks, which resulted in extraordinarily narrow breadth, as just a handful of names were responsible for most of this year's gains in the major market averages. Bears purport that when that bubble bursts, it will take the rest of the market down with it. It looks like that was their third strike, as a dramatic improvement in breadth over the past week should override concerns about a bubble if it exists.

Finviz

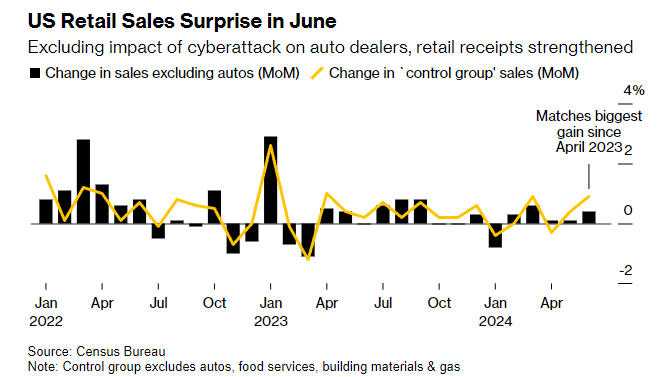

We had another Goldilocks economic report in yesterday's retail sales for June. The consensus was expecting a monthly decline of 0.3%, but sales were unchanged, despite a steep 2.3% decline in the automobile category due to a cyberattack on CDK Global, which makes the software that supports car dealerships. Core retail sales, which excludes autos, gasoline, food services, and building materials, rose a solid 0.9%, which was the largest monthly increase since April 2023. That is the number used to calculate GDP, which means we finished the second quarter on a strong note. This is vitally important to the soft landing narrative because last week's first negative print in the overall Consumer Price Index since the start of the pandemic was raising growth concerns.

Bloomberg

A rate cut by the Fed intended to support economic growth is much different than one instigated by a declining rate of inflation. If the upcoming cut was to fend off slowing growth, we would likely be on the cusp of a recession by now, and the stock market would be losing ground in advance of that. The cuts the market is pricing in today are in consideration of the disinflation that is drawing us nearer to the Fed's 2% target. This is what the market is telling us through the significant improvement in breadth that we have seen over the past few days. Investors are taking profits in mega-cap technology names, but not because there is a bubble. It looks more like a pause to refresh the uptrend or consolidate the phenomenal year-to-date gains. That money is finding its way into the remaining sectors and segments of the stock market, led by small-cap stocks.

Bloomberg

The Russell 2000 Index (RTY) has now risen a stunning 11.5% over the past five trading days. If we listen to the market, it is telling us that the economic expansion is alive and well, despite the recent softening from higher interest rates, which should be meaningfully lower by the end of the year. At the same time, the rate of inflation is on track to fall to the Fed's target in the months ahead, as the personal consumption expenditures (PCE) price index is already at 2.6%. In other words, a soft landing is on the horizon. That means there is a significant upside in the marketplace if investors focus on the laggards of the past 18 months.

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.