scyther5/iStock Editorial via Getty Images

For some unfortunate tech stocks, the day of the IPO is its biggest moment in the sun, and every day thereafter is a disappointment. Such is the case for Vimeo (NASDAQ:VMEO), the video hosting and editing brand that competes against Alphabet's (GOOG) (GOOGL) YouTube.

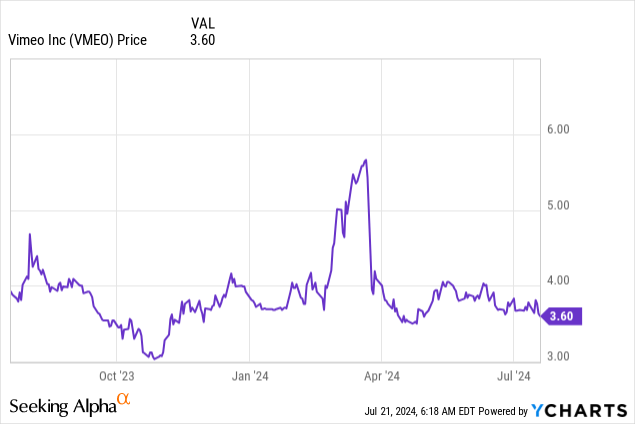

Year to date, shares of Vimeo have barely moved, missing out on the massive gains on the S&P 500. And while small-cap stocks have jolted sharply upward in recent weeks on hopes of a Fed rate cut, Vimeo has remained stubbornly depressed: and in my view, it's likely to remain more so.

Vimeo likes to tout itself as a software-as-a-service business, giving creative professionals and companies the tools and means to create beautiful, high-quality videos and share them with the world at high res. Unfortunately, the company is losing subscribers: for the very reason that it's a much smaller player in the video space that is charging a fee where competitors are free. The company is trying to address this by pivoting to the enterprise, but the B2B business is far too small to mask declines in the consumer segment.

And so, despite its cheap valuation, I'm initiating Vimeo at a sell rating. In my view, the company will continue to struggle in justifying its business model, and revenue deterioration will eventually push the stock toward deeper losses.

Why pay for something that's free?

Before we address Vimeo's efforts to bolster its offerings for enterprise clients, we'll first discuss where the company is ailing: in its original consumer business.

Vimeo, for investors who are unaware, is a full-service platform dedicated to creating, editing, and sharing high-quality videos. You can think of Vimeo as an alternative to YouTube, but much smaller. And while its larger rival YouTube also has editing tools, Vimeo positions itself as a more polished, professional video creation and management platform that caters toward serious creatives.

Unfortunately, in a macro environment in 2024 in which many software businesses have reported heightened churn from SMB customers and individual users, Vimeo has not been able to escape that same fate.

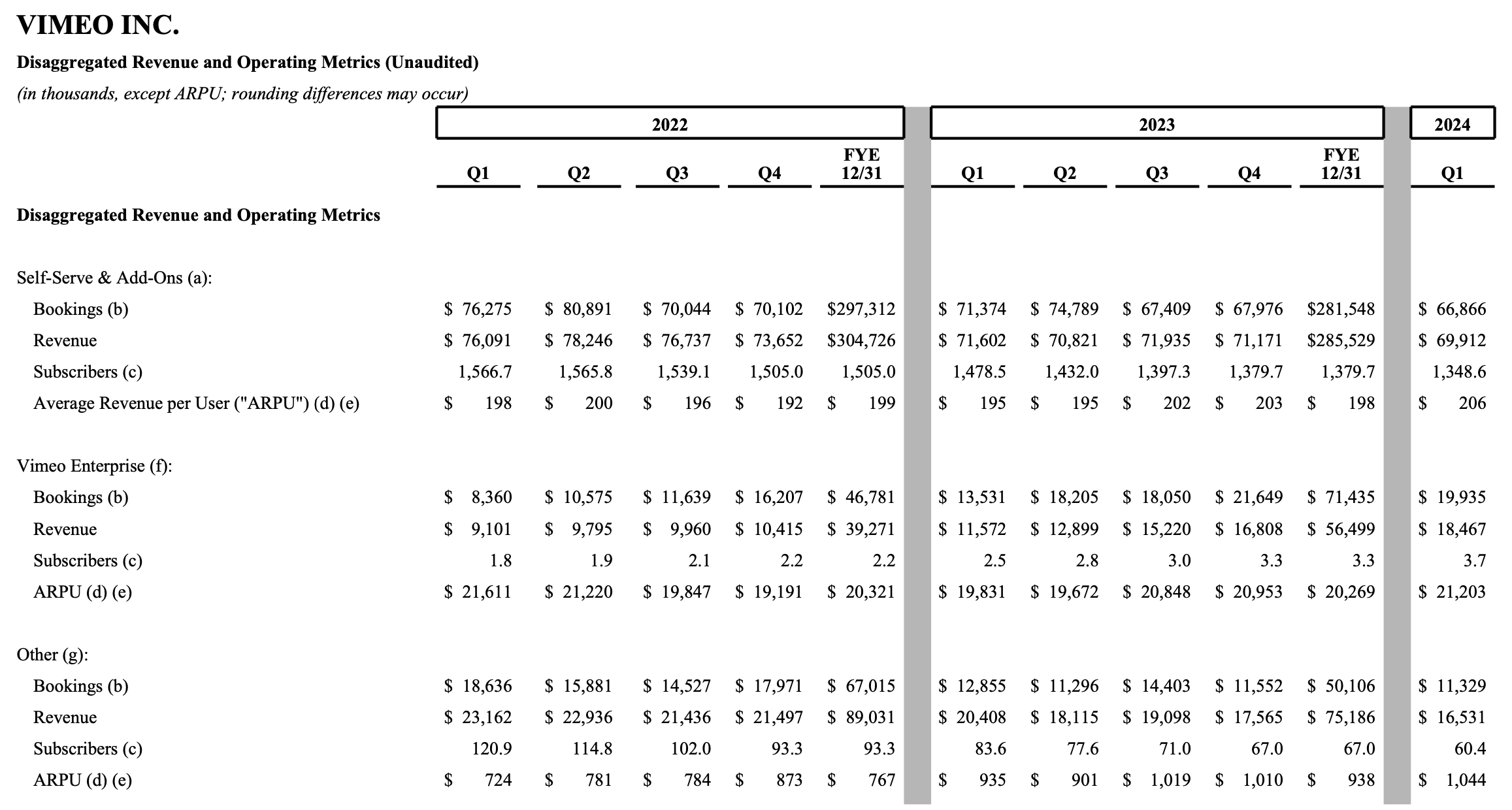

Vimeo trended metrics (Vimeo Q1 shareholder letter)

Self-serve / individual subscribers in Vimeo's most recent quarter fell to 1.35 million, a loss of 130k subscribers (-6% y/y) and 30k subscribers from Q4.

To me, these sagging metrics raise a very important existential question for Vimeo: why should people pay for something that a competitor offers for free?

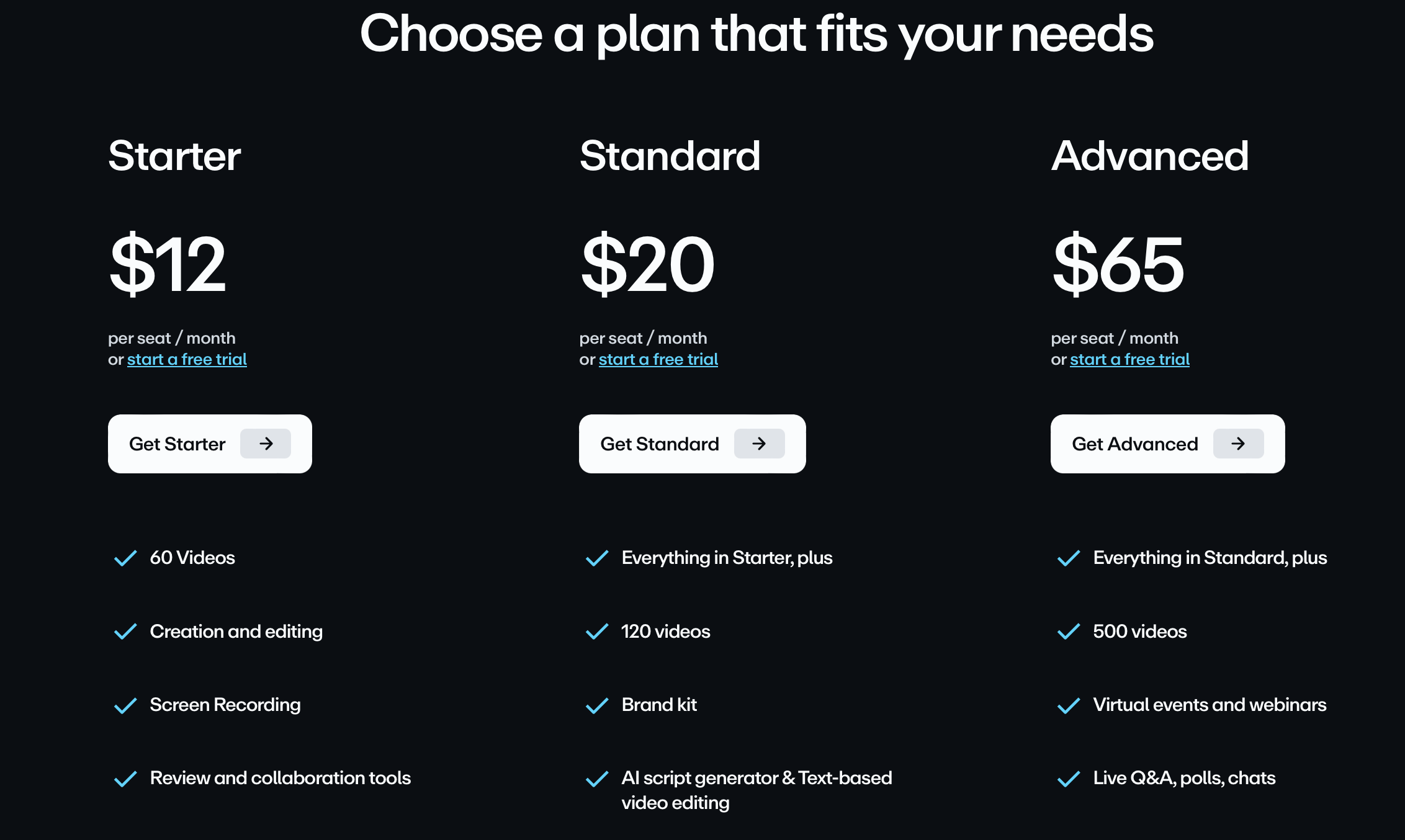

Vimeo pricing (Vimeo website)

The chart above shows Vimeo's latest individual pricing plans, taken from its website. Its starter package begins at $12 per month and limits users to uploading only 60 videos. YouTube, meanwhile, charges nothing for video uploads and doesn't limit the quantity of user uploads.

Vimeo's major selling point is a (purportedly) more professional experience and a video hosting platform that isn't tied to the mainstream YouTube channels. But the major con here is that as Vimeo is not affiliated with YouTube or Alphabet (GOOG), according to Limelight, Vimeo-hosted videos are less likely to be prioritized on Google searches vis-a-vis YouTube videos. That's a double-whammy against content creators deciding between hosting their videos on Vimeo versus YouTube. Why pay for something that YouTube offers for free, and which may offer fewer hits?

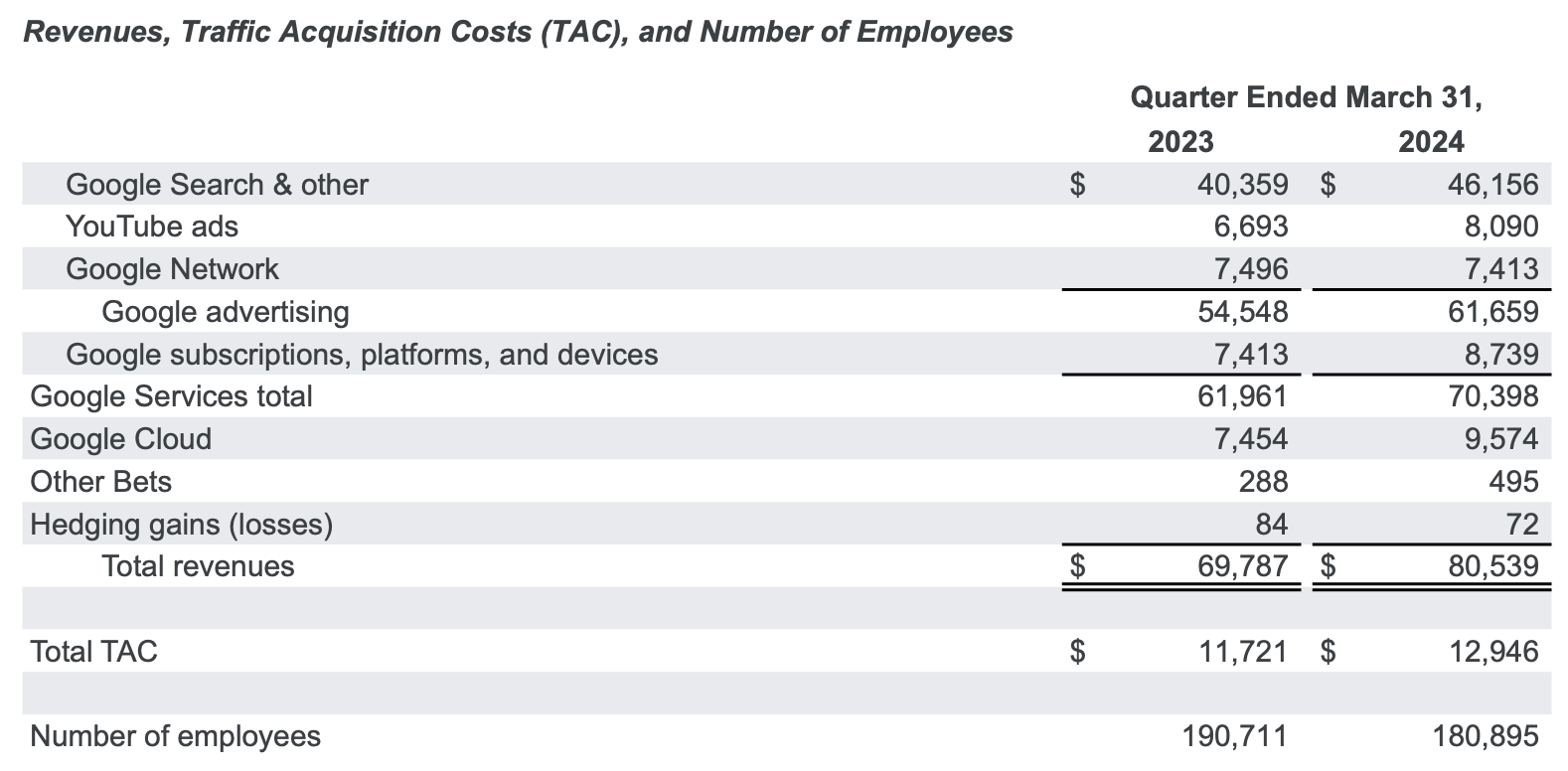

While Vimeo is struggling to retain users and get back to growth, YouTube is expanding rapidly, and it's one of Alphabet's most successful segments. YouTube revenue in the most recent quarter soared 21% y/y to $8.1 billion, which was just over 10% of Alphabet's overall revenue.

Alphabet revenue disaggregation (Alphabet Q1 earnings release)

Vimeo's bet on enterprise

The company's answer to declining individual subscriptions is basically to pivot away from the business (it's spending less on advertising and marketing to individual users) and to focus on enterprise.

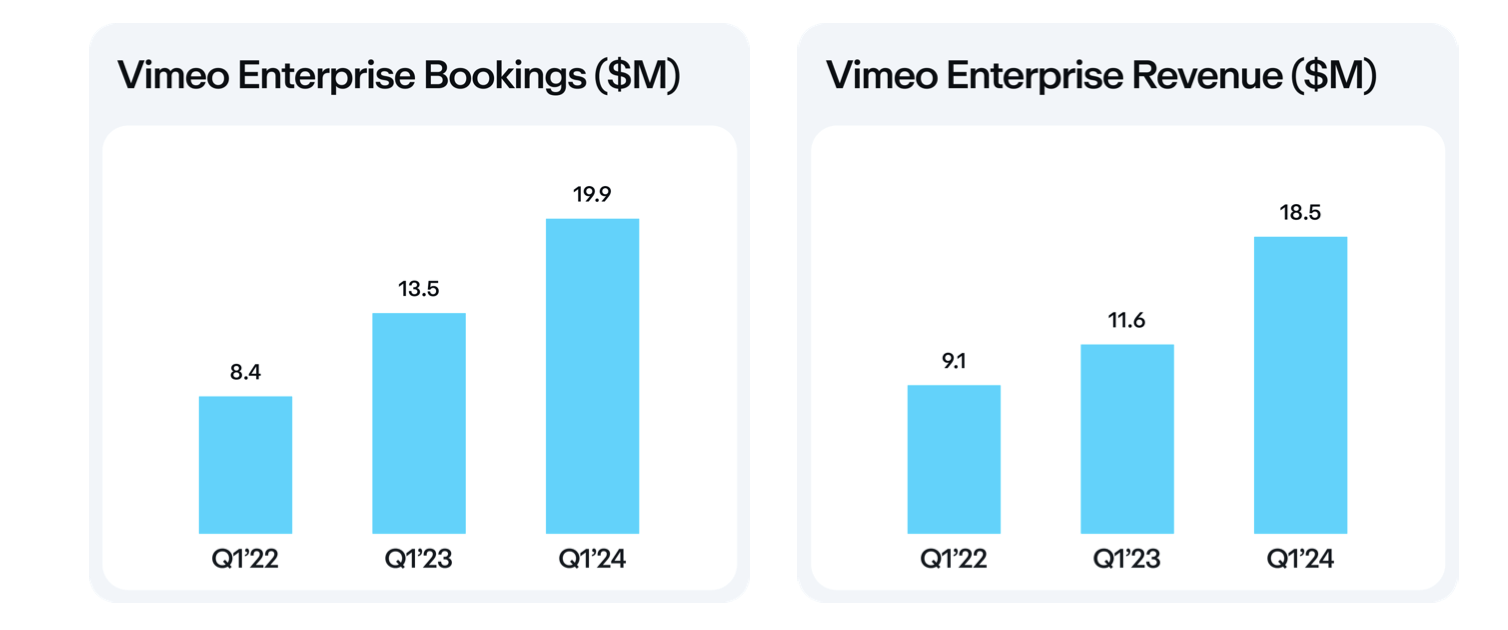

In Q1, Vimeo's enterprise revenue grew 59% y/y to $18.5 million, while enterprise subscribers clocked in at ~3,700, an increase of roughly 400 subscribers in the quarter.

Vimeo Enterprise metrics (Vimeo Q1 shareholder letter)

The enterprise business makes sense: think of universities or consumer product companies that want to post informational videos but don't want the YouTube logo hovering over the play button.

Here's what we need to recognize, however. While Vimeo touts blue-chip client adds like Deloitte, Banco Santander, Delta Airlines (DAL), and 7 Eleven among its customer base, Vimeo's enterprise revenue is still tiny. Enterprise ARPU (average revenue per user) itself is only ~$21k, indicating that enterprise deals aren't truly bringing in boatloads of revenue to be able to offset sharp consumer losses. Enterprise is still less than 20% of Vimeo's revenue, and the massive growth year is only able to just offset the consumer declines. Total company revenue in Q1 grew only 1% y/y.

This is expected to get worse in Q2, as guidance is calling for a -3% y/y decline - which the company is attributing to tougher y/y comps in the enterprise space. In the company's Q1 shareholder letter, management added the following context around its guidance:

We continue to believe that we are putting Vimeo on a path to return to profitable revenue growth, recognizing that the path to growth will not be linear. Looking ahead to Q2, we expect revenue to decline sequentially as it did in 2023. Additionally, we expect year-over-year bookings growth to decelerate due to some tougher comparisons for Vimeo Enterprise and Other and the continued impact of our move to more efficient marketing spending."

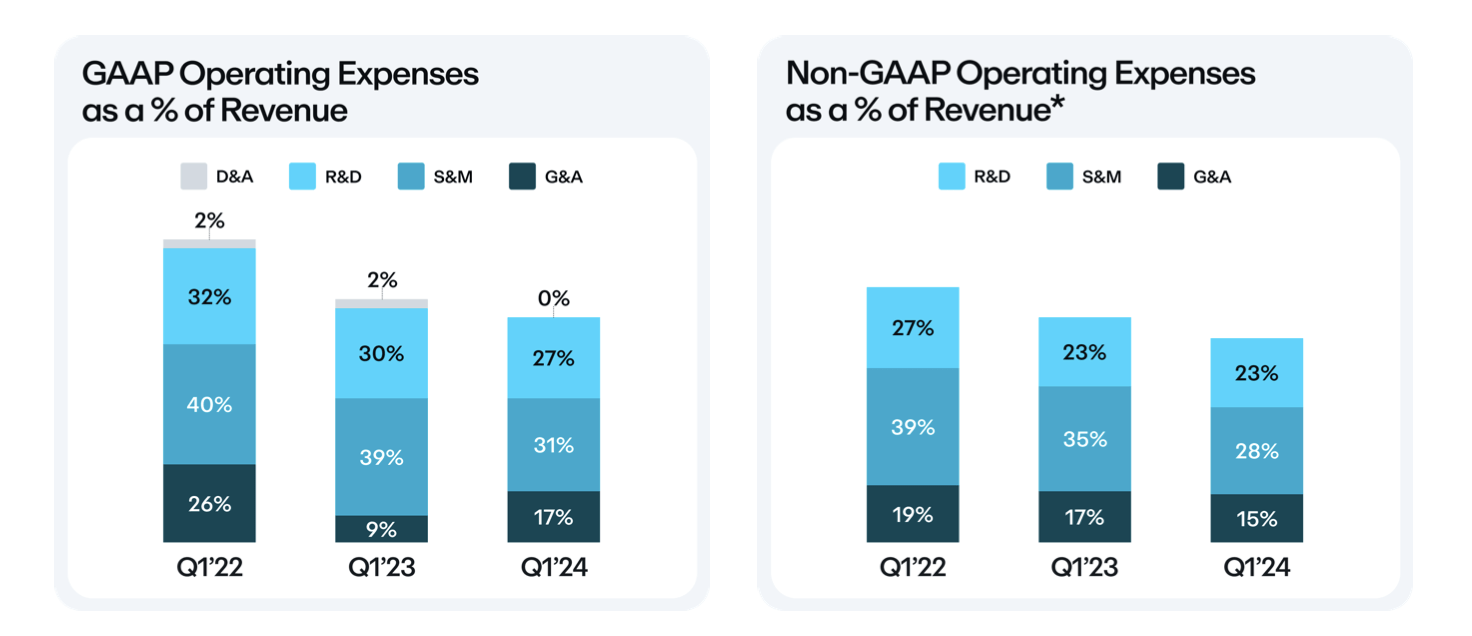

We should give Vimeo credit for its reduction in expenses. Pro forma operating expenses have declined sharply as a percentage of revenue, especially sales and marketing - which fell to 28% of revenue in Q1, from 35% in the year-ago quarter. This is driven by the company's intentional decision to pull back from advertising toward self-serve customers.

Vimeo opex trends (Vimeo Q1 shareholder letter)

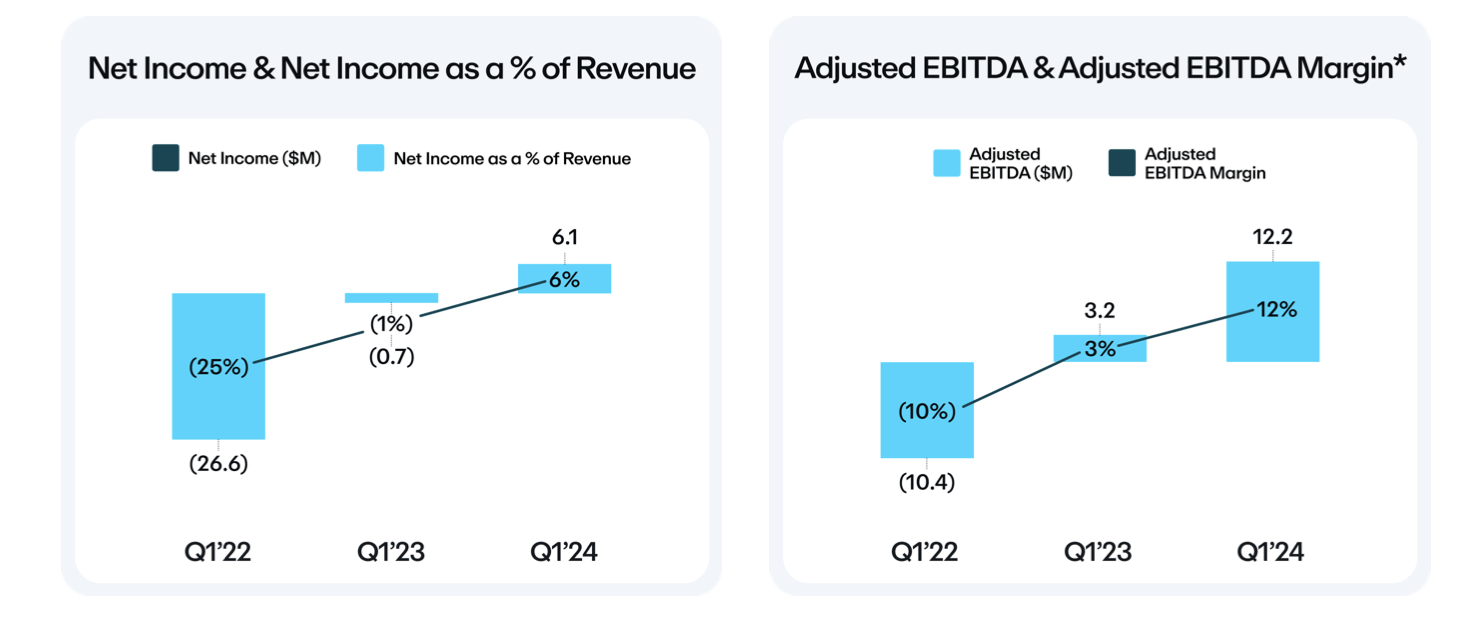

As a result, adjusted EBITDA margins did grow to 12%, and the company has been free cash flow positive in each of the past six quarters.

Vimeo adjusted EBITDA trends (Vimeo Q1 shareholder letter)

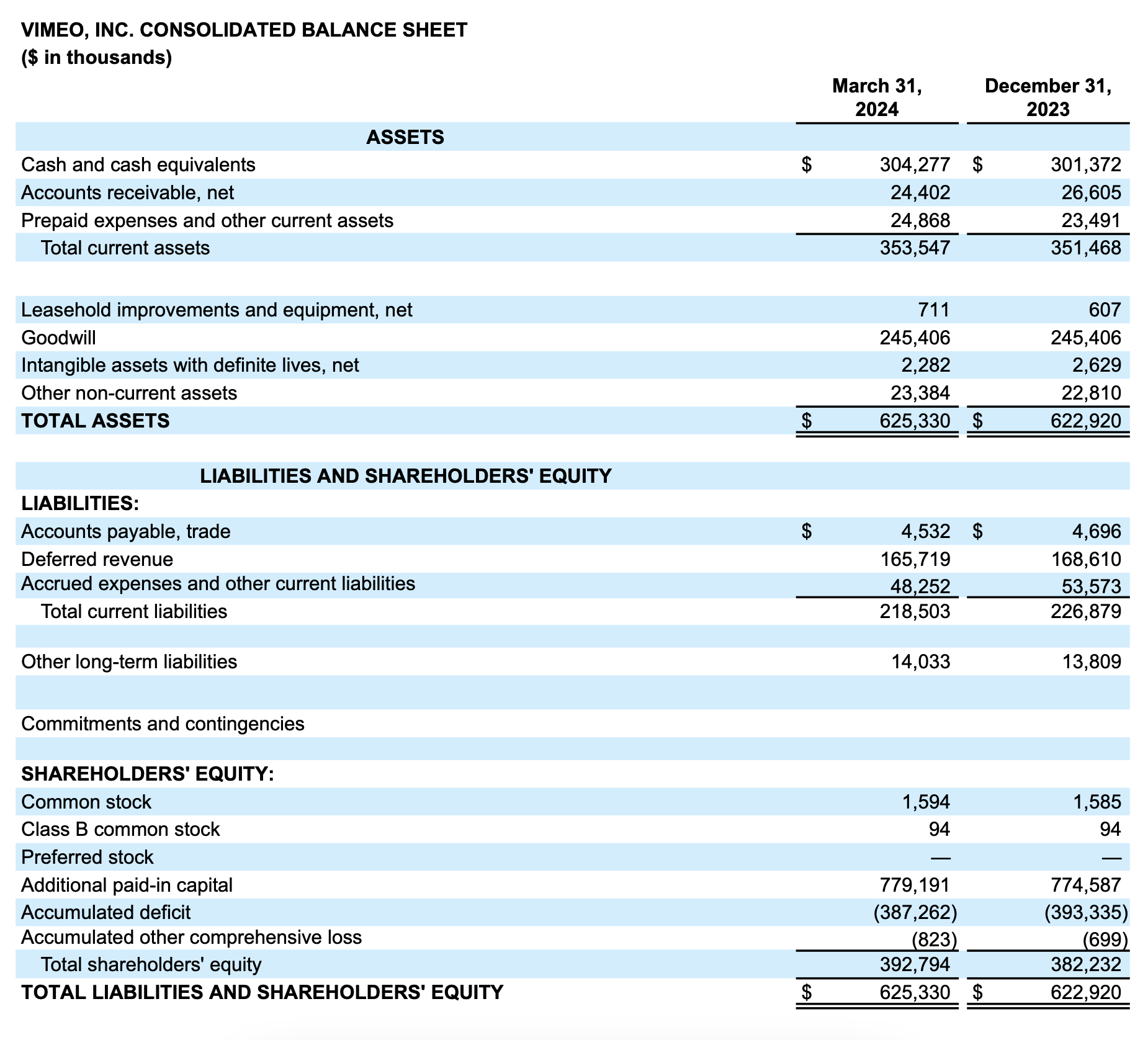

With positive FCF on top of ~$300 million of cash on the company's latest balance sheet (see below), Vimeo is stable for the moment.

Vimeo Q1 balance sheet (Vimeo Q1 shareholder letter)

But major question marks remain. Specifically, if Vimeo's consumer business continues to decline faster than its enterprise segment is growing, the profit equation could shift considerably toward losses. It's worth noting that Vimeo has been losing subscribers in each quarter for the past two years, and there's very little indication that this trend will cease.

Valuation and key takeaways

Yes, Vimeo is quite cheap, but still quite unattractive given its myriad of risks. At current share prices just under $4, Vimeo trades at a market cap of $609.4 million. After we net off the $304.3 million of cash on Vimeo's balance sheet, its resulting enterprise value is $305.1 million.

Against Wall Street's revenue consensus of $400.6 million (-4% y/y) for FY24, Vimeo trades at just 0.7x EV/FY24 revenue.

Given Vimeo's weak competitive position versus YouTube, and an enterprise business that is still far too small to offset self-serve user losses, I'd say Vimeo's opportunities to rebound to a more normalized valuation will be limited. Steer clear here and invest elsewhere.