Fenton Roman/iStock via Getty Images

Introduction

Opportunities like this rarely present themselves so clearly like the case of LL Flooring Holdings, Inc. (NYSE:LL). The company is one of the largest retailers of hard-surface flooring in America, with 435 retail stores and revenues hovering around $1 Billion per year over the last ten years. Gross profits have ranged from $418 to $284 million within that time. Revenues have fallen off precipitously in the past two years, while SG&A, ranging from $314 to $401 million, has increased steadily almost every year and remains high.

The company’s share price has cratered from a pandemic era high of $35 per share at the end of 2020 to the current $0.75 per share. While $35 was outlandish, so is $0.75, considering the changes that have just occurred in the boardroom, and those that I propose are about to occur to the company.

While at first glance, this could just be another story of a brick-and-mortar retailer suffering the fate of other retail chains as they fight in vain against the tide of online retail. But every so often it’s just a case of bad and/or apathetic management. I’ll argue that the typical failing brick-and-mortar story doesn’t apply to LL Flooring, because of what they sell. Flooring is one of those products that isn’t easy to sell online. It’s heavy. It’s costly. Digital images don’t accurately convey what it looks like, not to mention what it feels like.

Shipping is expensive and a pain, requiring specialized shippers rather than Amazon or UPS Ground. When you receive a shipment of flooring, it gets dropped off by a semi with a flatbed trailer, or box truck with a lift-gate on the street in front of your house. They don’t carry it in for you. It’s palletized in lengths up to 20 feet (ca. 6 m) or so. What, you don’t like it after seeing it in person? But you took delivery. They might let you return it, but returns are even more of a pain. Or it might sit in the street until you give up and accept that you bought 2,000 square feet (1.86 a) of what was billed as exclusive smooth European red oak online at $15/square foot that looks more like distressed hickory. (This may or may not be based on a tragic personal experience.)

No, for some goods, traditional retail (with a robust online funnel of course) is still the best approach. Flooring is a relatively high-dollar investment, unlike a shirt, for example, that can be easily sent back to the online store if it doesn’t look like it does in the photo online.

Thesis

LL Flooring was hit by rumors of an imminent Chapter 11 filing on Wednesday, July 3. This caused the stock to tank, hitting a low of about .53 on Friday, July 5. This could have been just another story amid the deluge of retail chains going belly up from a great migration of buyers to online stores. But what is different here is that the founder of the company, formerly known as Lumber Liquidators, who has been trying to buy the company for over a year through his company F9 Investments LLC, just won a proxy battle. He got himself and two associates elected to the board after the July 9 annual meeting. Those kicked off the board include the long-time Chairperson.

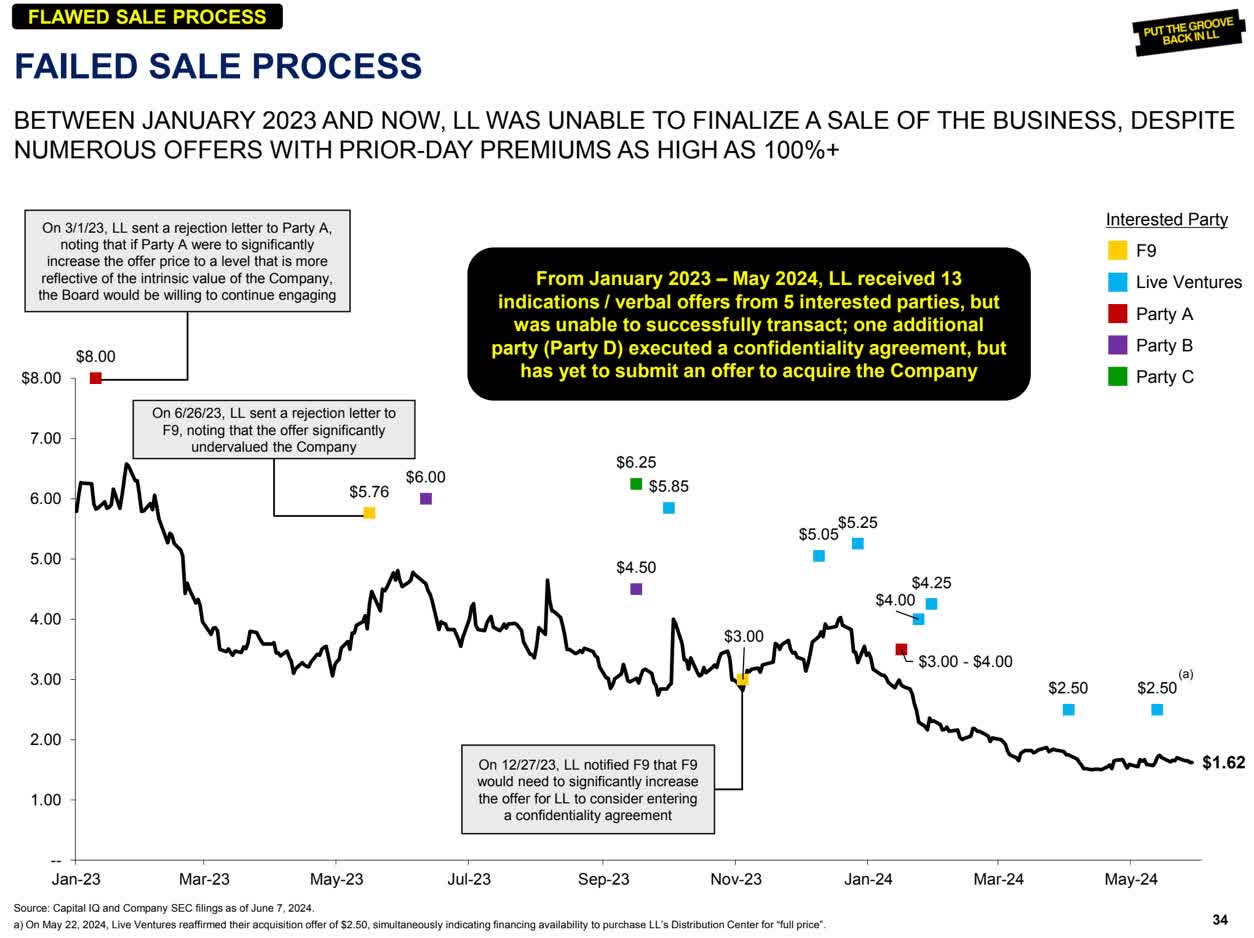

Failed Sale Process (F9 Investments Slide Deck)

The case for a change to the board could not have been more clear. I don’t think I’ve ever seen a public company board so out of step with the interests of the shareholders as in the case of LL Flooring. This is a board that rejected multiple recent offers from Sullivan’s company to take the company private at share prices ranging from $5.76 per share — which was a 100% premium to the share price at the time — to $3.00 per share. A previous attempt by Sullivan to buy out LL Flooring or merge it with Sullivan’s kitchen and bathroom remodeling company Cabinets To Go was rebuffed in 2019.

In fact, according to LL Flooring, there were five bidders for the company, including F9, with bid prices as high as $8.00 per share — about $2 higher than the stock price at the time — in January 2023.

Now with three new board members with relevant experience in the exact business environment and a history of success, I think a turnaround at LL Flooring is likely.

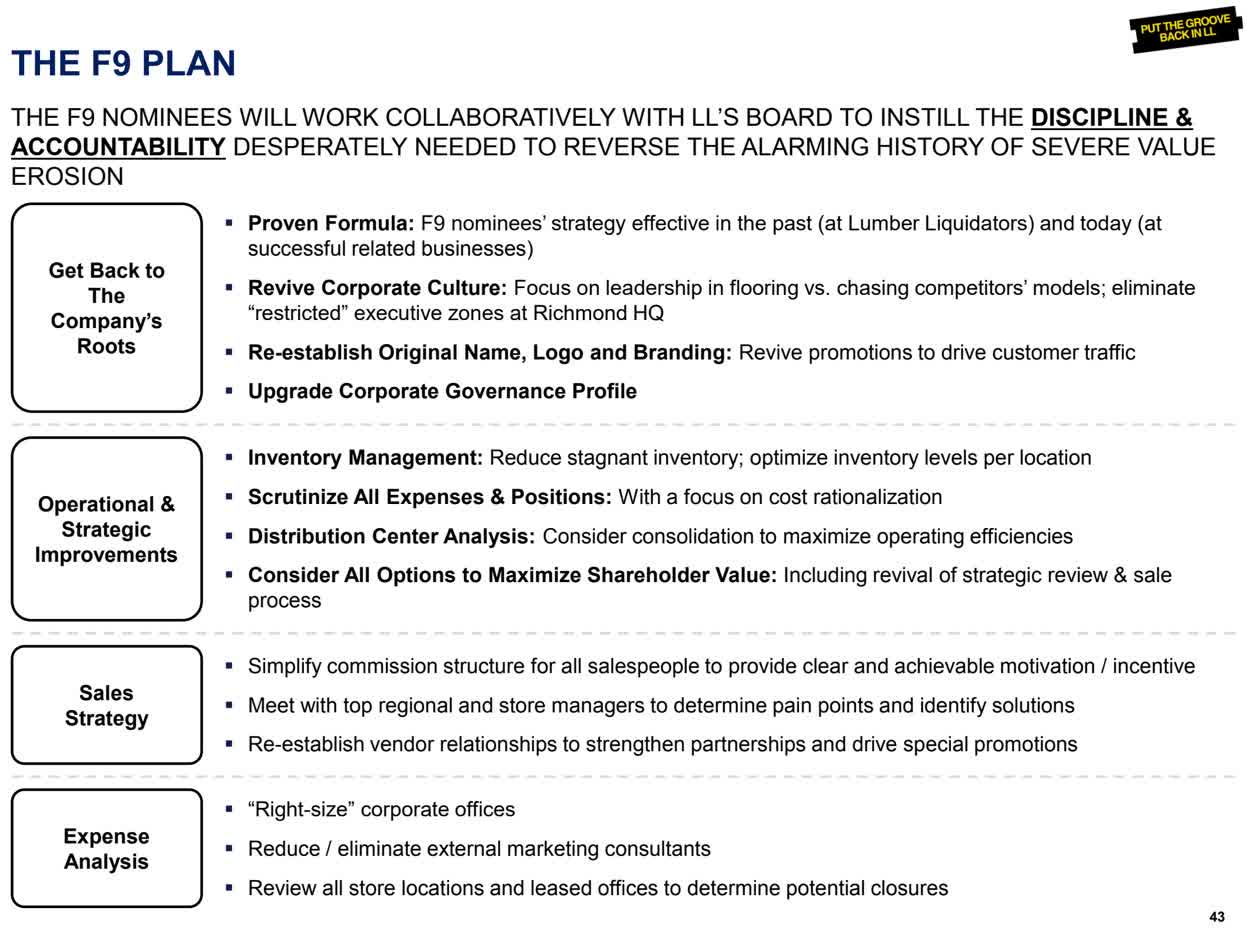

Sullivan and his F9 Investments spelled out the case for change in a June 13 slide deck, and I recommend reading at least Section III for an overview of the plan to right the ship at LL Flooring.

F9 Investments’ plan is detailed in the slide below:

F9 Investments Slide Deck

The core of the plan is a return to the company’s Lumber Liquidators roots, namely concentrating on providing the best deals in clearance flooring with immediate availability. It is a winning formula with decades of successful implementation. The original retina-scorching yellow logo reminded one of a markdown sale tag. The no-frills locations gave the perception of value while also keeping expenses low for the company.

Lumber Liquidators knew that they stood for value above all else, and outsold and undercut almost everybody. As many will recall, the company got into serious trouble when some of their imported flooring products were found to have excessive levels of formaldehyde. While this was a big scandal for them at the time, their sales recovered well before the poorly received name change to LL Flooring.

F9 Investments also want to return to the Lumber Liquidators brand name and logo, which I wholly support.

LL Flooring Website Lumber Liquidators Website Archive

Which storefront above communicates “flooring deals” better? Which name is more memorable? Which logo/sign is more visible?

I’ll argue that the hands-down winner of each of the above questions is Lumber Liquidators. Note that I’m not suggesting the original logo and color scheme is more refined, elegant, or understated. That’s not the point. LL Flooring leadership convinced themselves that the problem was the name’s association with past errors and ditched it all for a name that would be perfect for a mob front or a covert CIA operation — bland and forgettable.

LL Flooring would do well to return to the original value proposition, dispense with the directionless marketing, review all operations to remove excess costs and bottlenecks, and re-establish a connection with all the company’s store managers and salespeople on the floor.

Fortunately, the new directors include: Lumber Liquidators’ founder, Thomas Sullivan; John Delves, the President and CEO of F9 Brands and Cabinets To Go and a former supplier to Lumber Liquidators as the president of a flooring manufacturer; and Jill Witter, a Chief Legal Officer to a number of publicly held companies and also a past CLO of Lumber Liquidators. These are all people who know the operations of LL Flooring in great detail, and I think can quickly gain the confidence of suppliers, employees, and lenders as they seek to correct the company’s course.

Now that Tom Sullivan and his associates are on the board, I expect that changes are going to come rapidly. As those changes are communicated to investors, the share price will react positively.

Financials

I expect one of the first things the new board members will want to do is engage with LL Flooring’s lender to get a bit of breathing room. Currently, LL Flooring has an asset-backed revolving credit facility that requires a certain threshold of available liquidity. In the latest 10-Q, LL Flooring stated that they had:

cash and cash equivalents of approximately $6.0 million, $89.0 million outstanding under the Revolving Credit Facility, a net loss of $29.0 million, and $57.3 million of borrowing availability under the Credit Agreement for the quarter ended March 31, 2024. The Company’s ability to continue as a going concern is dependent on its ability to generate sufficient sales, profitability, and liquidity to meet the Company's obligations and maintain the minimum borrowing availability to prevent triggering its fixed charge coverage ratio covenant. Under terms of the Credit Agreement, the fixed charge coverage ratio is only required when specified availability under the Revolving Credit Facility falls below the greater of $17.5 million or 10% of the Revolving Loan Cap (as defined in the Credit Agreement). The Company believes that its projected levels of liquidity will not be sufficient to maintain compliance with this covenant in the fourth quarter of 2024.”

This projection required a Going Concern warning, as LL Flooring believes the covenant will be triggered in Q4 of this year.

Management’s plan was to sell and leaseback the company’s distribution center, the proceeds of which they state

are expected to be sufficient to fund the Company's operations and prevent triggering its fixed charge coverage ratio covenant for a period of at least twelve months subsequent to the issuance of these unaudited consolidated financial statements.”

The Q1 10-Q filing came on May 8, and then LL Flooring provided an update on June 28 in the form of an 8-K filing. The update relayed that the sale transaction of the Sandston, Virginia distribution center is well underway, with:

a number of preliminary bids and several second-round bids in connection with such sale process and expects to move forward with negotiating with certain bidders for the possible sale of the Distribution Center.”

The company also stated that it is

in discussions with representatives of the banks that are party to the Credit Agreement regarding an additional liquidity reserve requested by the banks and additional modifications to certain provisions of the Credit Agreement.”

Before F9 Investments’ slate being elected to the board, but after this filing, Sullivan also submitted a filing indicating a willingness to consider acquiring the distribution center if selling it becomes necessary. It therefore seems that there are interested parties available to purchase the distribution center that will alleviate the near-term financial pressures.

A key point here is that F9 Investments owns 8.85% of the common stock of LL Flooring (see page 5 of the F9 slide deck). It was acquired at a substantially higher price per share than the current share price, and therefore F9 has a strong incentive to see the company succeed in its turnaround.

Industry Tailwinds

The home renovation market was flying high during the pandemic, as many people stuck at home chose to upgrade their surroundings. As the high point of the pandemic subsided and the Fed worked on tamping down runaway inflation, they raised rates rapidly. The high rates led to a decline in home sales as people with lower-rate mortgages decided to stay put rather than sell their homes and be faced with a doubling of their mortgage interest rate on their next home. Since the primary customers of flooring are people who just purchased a home or people who are selling their homes, the flooring market has contracted with the steep rise in interest rates.

As the Fed lowers rates in the coming year, this should lead to a large wave of home sales as mortgage rates drop. This will in-turn prompt an increase in flooring sales. Even LL Flooring made a profit during the main pandemic years, despite poor management, marketing, and expense control. Now, with a re-invigorated Board and much greater accountability, LL Flooring stands to benefit from the tailwinds that I’m expecting.

Risks

While I believe the risk/reward ratio is in LL Flooring’s favor, it is still now a microcap stock that faces big financial hurdles and should be considered high risk. One of the biggest risks is if the company is forced to raise money at a distressed valuation, causing inordinate dilution, or if the company has to file for bankruptcy. Fortunately, there are only about 30 Million shares outstanding, and with significant owned property valued at $246 Million and inventory valued at $248 Million on the books, and there is still plenty of room on the company’s credit line. In addition, the company estimates that loan triggers won’t be tripped until Q4, which leaves plenty of time to negotiate a path to stability. I find dilution to be a big risk when insiders don’t own shares. Sullivan and his investment company own almost 10% of the outstanding shares, however, so an overly dilutive raise would affect him, too.

LL Flooring’s recent financial performance has been poor, and were it not for last week's significant changes and injection of new vision onto the Board, I would not be positive about the company’s stabilization and potential for recovery.

LL Flooring has many opportunities to continue to screw up in relation to its peers, but the fact that there are peers that are performing well in the current environment means that there is a place for LL Flooring too. I agree with the founder that getting back to their roots is the best way to succeed.

Conclusion

Winning a proxy campaign against incumbent board members is not easy, yet shareholders have spoken resoundingly that change is needed at LL Flooring. The market concluded that LL Flooring was destined to become another victim of the vast shift to online purchasing, without realizing that what caused LL Flooring’s troubles was largely poor management decisions rather than anything intrinsic to retail flooring chains. Now, with new experienced management joining the Board, with a significant number of shares and a clear vision to restore LL Flooring’s fortunes, this stock provides an excellent near-term turnaround opportunity.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.