imaginima

The Thesis

Packaging Corporation of America (NYSE:PKG) delivered positive topline growth in the first two quarters of 2024 after experiencing a decline throughout 2023, as volume was strong for the company's containerboard and corrugated products during the quarter despite weak year-on-year average pricing and mix. I expect this strong demand along with strength in the company's backlog should support the company's topline in 2024 despite sustained weakness in certain parts of the company's business due to headwinds from the challenging macroeconomic environment across North America.

The company's margins, on the other hand, should also remain under pressure in 2024 due to anticipated flat sales growth in 2024 and an increase in rail rates during the recent quarter. While the near-term prospects appear to be weak, the longer-term looks decent as the company continues to focus on capacity expansion by restarting mills to deal with an anticipated rise in demand in the future. The company's stock is currently priced at a premium to its historical levels, considering unfavorable near-term prospects, I would stay with a Hold rating on this stock.

Last Quarter Performance

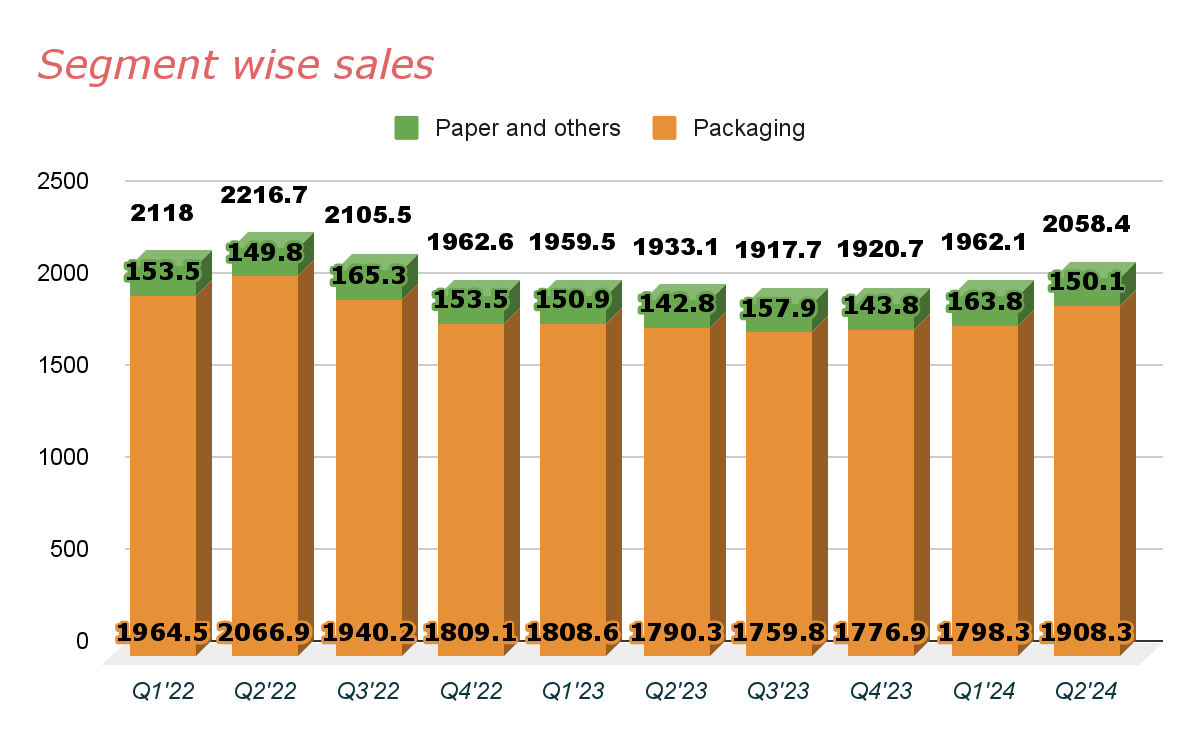

After five straight quarters of continuous decline in the Packaging segment, it turned positive in the second quarter of 2024 as the segment's revenue grew 6.6% versus the prior year's quarter. Positive growth in the Packaging business along with year-on-year growth in the Paper segment helped the company deliver a consolidated topline growth of approximately 6.3% to $2.08 billion during the last quarter. This growth was primarily a result of strong market conditions in the company’s packaging business for both the corrugated products and containerboard, which drove record containerboard production during the quarter. The paper segment, on the other hand, benefitted from a 12% volume growth, more than offsetting the impact of lower year-on-year price and mix.

PKG segment wise sales (Research Wise)

While the topline expanded during the quarter, the company’s consolidated adjusted EBITDA margin saw a decline of 190 bps versus the prior year, dropping to 19.5% during the quarter. This contraction was primarily a result of margin decline across both segments, which was impacted due to lower average price and mix during the second quarter of 2024. Decreased EBITDA also impacted the company’s bottom line as its adjusted EBITDA was down to $2.20 from $2.31 in Q2 2023, however, beating the consensus estimates by $0.05.

Outlook

After experiencing weakness across the business in 2023, the company’s topline saw positive growth in the first half of 2024. I expect this growth to continue further in 2024 as the order remains strong in the Paper segment, which along with the benefit from strength in certain parts of the Packaging business including containerboard and corrugated products should support the company’s sales in quarters ahead. The company also announced a $100 price increase in 2024 across all the paper grades that the company implemented in April which, in my opinion, should further result in volume growth in the coming quarters of 2024. The Backlog levels primarily in the Packaging segment also remained elevated during the quarter despite continuous demand-related challenges driven by factors such as elevated inflation and higher interest rates. This backlog should also fuel sales growth for the company in 2024.

While the company’s topline has started to show some strength due to strong volume growth for certain products, the overall demand environment remains challenging. In addition, the company also faced a negative impact on volume during the last quarter due to a scheduled maintenance outage at the International Falls, Minnesota mill, which should significantly impact the company's topline growth for full year 2024.

Apart from this, the company acquired new customers mainly in its Paper segment, which resulted in incremental volumes for the company, which should benefit the company’s overall sales beyond 2024. During the quarter, as the demand exceeded expectations, the company was able to deal with it through the successful execution of the conversion outage at its Jackson mill and also restarted its machine earlier than anticipated. In October 2023, PKG successfully restarted the No. 3 machine, which operated efficiently through the end of 2023. This helped the company meet high demand and build essential inventory in the last quarter as well. In my opinion, these steps by the company, which aim, to ensure PKG can effectively meet market needs and maintain adequate inventory levels should support the company in meeting supply for growing demand which should drive the company’s sales in the longer term.

Now talking about the company’s margin outlook, as we discussed above, the company’s margin got hit significantly during the last quarter despite a slightly positive topline growth due to the impact of an outage and lower prices across both segments. I expect that the company’s margin growth should remain under pressure going forward despite the recent price increase in the Paper segment as the average prices and mix should continue to be on the lower side versus the prior year's levels due to the published decrease in index prices during the initial part of 2024.

In addition, the rail rate has also increased in six of the company's mills during the first half of 2024, which should lead to higher freight and logistics expenses in the quarters ahead, further impacting the company’s margin performance in 2024. However, the impact of scheduled maintenance, that occurred in the first quarter will be much lower in the upcoming quarter, which along with slightly lower operating and converting costs driven by improvement in seasonal weather and wages should partially offset the impact of the headwinds mentioned above.

Overall, I expect the company’s topline to continue to face headwinds from the outage impact and challenging macro in the near term. However, strong volume growth in certain parts of the company’s business and benefits from a strong backlog should support topline growth for the rest of the 2024. Margins should also remain under pressure due to the expected rise in freight and logistics costs in the coming quarter. However, the longer term remains favorable as the company continues to expand its capacity through restarting of its mill to address the expected rise in the longer term.

Valuation

Since my last neutral article on PKG in April, the company's stock has been up by mid-single digits and down in the low single digits. This was primarily due to the poor margin performance of the company in the recent quarter that led to bottom-line contraction. Currently, the company's stock is trading at a forward Non-GAAP P/E of 22.01 based on the FY24 EPS estimate of $8.78. When compared to the five-year average forward P/E of 16.89, the stock still appears to be at a significant premium.

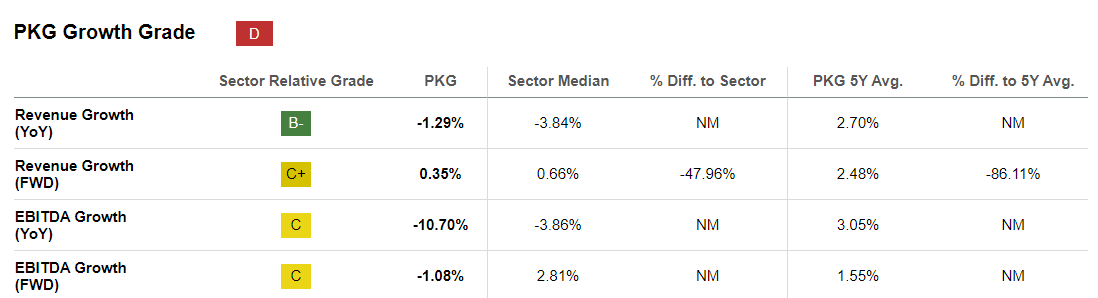

PKG Growth grade (Seeking Alpha)

Going forward, I expect the company's revenue to get support from strong volume across certain parts of the Packaging segment and the backlog strength, which should offset the negative impact of the overall weak demand environment due to higher interest rates. As we can see in the figure above, the company's margin is also expected to be under pressure going forward, possibly due to the impact of the expected rise in freight and logistics costs. The operational and conversion cost is also expected to be higher in the coming quarter, mainly in the company's paper business, due to seasonal electricity usage and slightly higher recycled fiber costs, further impacting the company's margin, which could potentially impact the company's bottom line further deteriorating the company's valuation in the coming quarter.

Conclusion

I last covered PKG in April this year and discussed that I thought the topline weakness would continue into Q2'24 due to expected volume declines. However, the demand environment remains strong, leading to single-digit growth during the last quarter. I was expecting margins to be stable due to the recent price increase, however, a decrease in index prices impacted the average price, which negatively impacted the margins during Q1'24. As we discussed above, the company's stock is currently at a premium to its historical average and sector average. The near term looks unfavorable due to continued weakness in certain parts of the business. The longer-term outlook, however, looks good, as the company is expanding its capacity to meet growing demand.

Margins should also benefit from this in the longer term, along with operational improvements and higher pricing, but the near-term margin prospects look weak, mainly due to slower topline growth and an expected increase in operational expenses. While the long term looks promising, I am concerned about the company's near-term headwinds and an elevated valuation, which makes the stock price unreasonable to me at the moment, making me stay with a hold rating for now.