johny007pan/iStock via Getty Images

Summary

Acomo N.V. (OTCPK:ACNFF) is an interesting niche business playing in a sector with very strong tale winds as plant-based food diets are a very strong rising trend. They have a shareholder-aligned management culture, a long-standing history, and expertise, prudent debt management, and solid asset allocation. Stock shares are undervalued. I recommend they add this name to their watch list, waiting for future pullbacks to start a position.

This article aims to provide readers with an extensive and comprehensive view of this company, including a review of the latest H1 2024 results that the firm published on the 23rd of July 2024.

Business Overview

Acomo N.V. or Amsterdam Commodities, is a Dutch company based in Rotterdam. The group provides key services along the food and beverage ingredients supply chain through its 5 different divisions: Spices and Nuts, Edible Seeds, Tea, Organic Ingredients, and Food Solutions. Some of the activities that the divisions carry out are sourcing, trading services, long-term pricing, market research, market intelligence, storage, blending, cleaning, heat treatment, processing, packaging, and vendor-managed inventory solutions.

Company Website

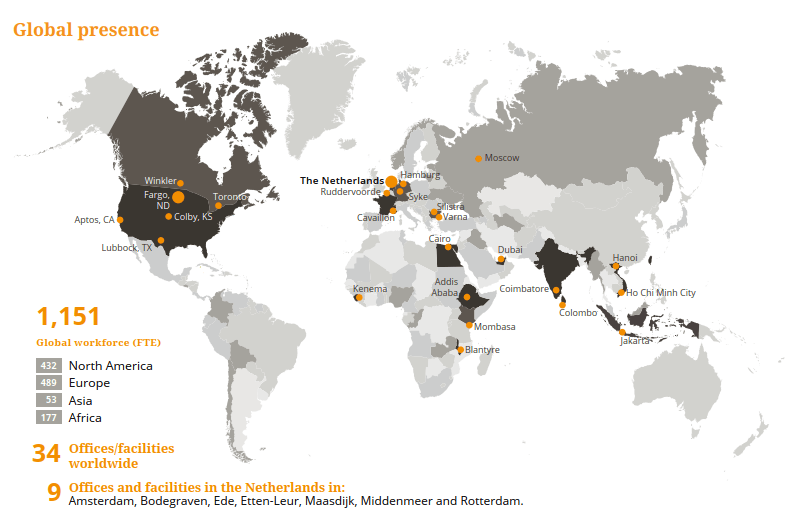

Below are shown the main operations Acomo's segments perform as core activities as well as the global presence of the company.

Company 2020 Presentation Company 2023 Annual Report Company 2023 Annual Report

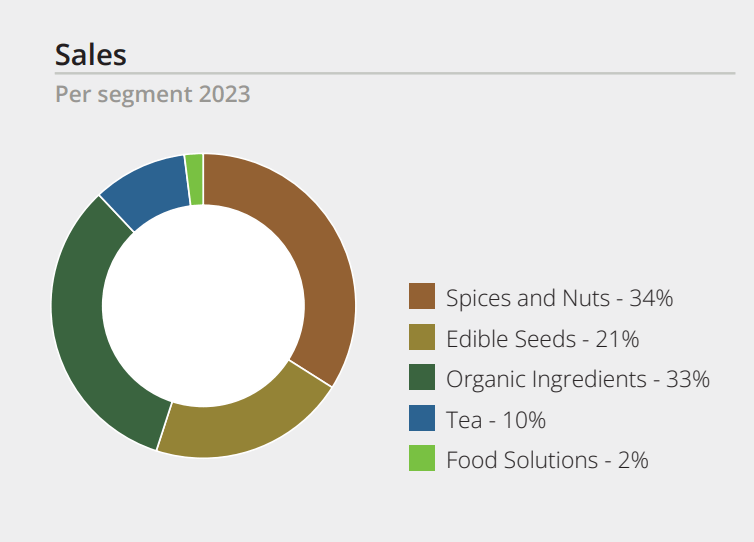

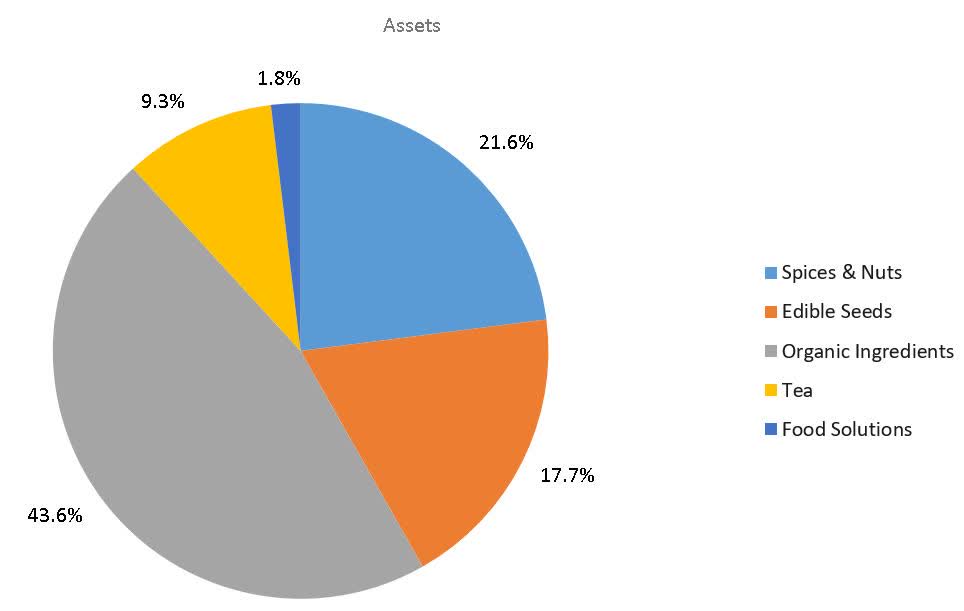

Below is shown the revenue and asset contribution by each segment in 2023:

2023 Company Annual Report Image created by the author with data from the company´s annual reports (Author's Own Analysis)

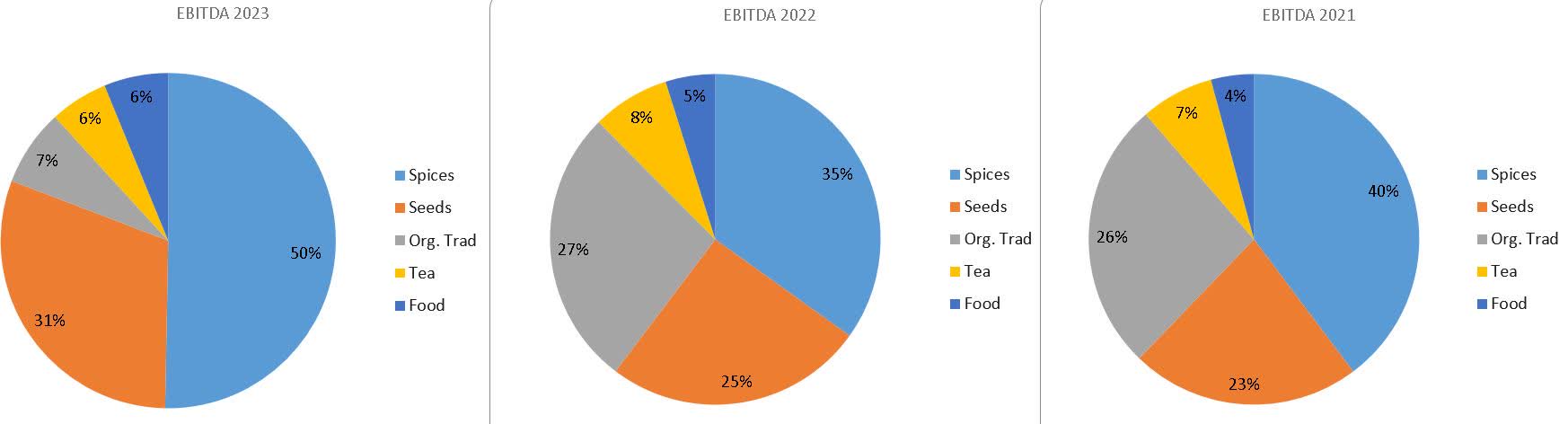

It is more interesting to see how this revenue per segment is translated into EBITDA for the last three years:

Image created by the author with data from the company´s annual reports (Author's Own Analysis)

In 2020, Acomo bought the company Tradin Organic from SunOpta Inc. (STKL) to open the group to the organic ingredient market. This segment's performance has not been stellar in the last three years. Although it has been affected by external events like extreme commodity volatility (cocoa), the company operates in a market with thin margins and low return on capital employed.

The group is seeking to strengthen the Spices and Nuts division, and in this line, Acomo's latest acquisition is the company Caldic Food Service & Retail Sweden AB. This company operates in the nuts and dried fruit business in Northern Europe. Acomo wants to strengthen the Spices & Nuts segment and establish a stepping-stone in the European Nordic markets. The company is mainly active in Denmark, Sweden, Norway, Finland and Germany. Caldic Food supplies a wide range of nuts, seeds, kernels, dried fruits, pulses, and marzipan to wholesale and retail customers, the food industry, and the Out-of-Home market.

It is worth mentioning that a new group's CFO will start in October 2024 as was announced by the CEO in the latest H1 2024 press release.

I am excited to announce that Mirjam van Thiel will join per 1 October as Group CFO of Acomo, bringing highly relevant business and financial experience.

Financial Position & Performance:

Units expressed in millions of euros. All the information shown has been extracted by the author directly from the annual reports of the company.

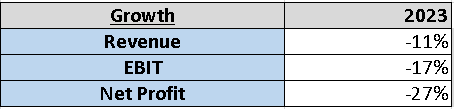

The company has struggled in 2023 to grow. Both the top and bottom lines have fallen year after year. 2023 has been the worst year since 2004 when the company experienced the second-worst decrease in sales, EBIT, and net profit.

Image created by the author with data from the company´s annual reports (Author's Own Analysis)

Taking a look at margins, in the last 5 years Acomo has managed to keep them in line although in the last 3 years due to external events and the debt service costs, the profit and net margin have decreased.

Image created by the author with data from the company´s annual reports (Author's Own Analysis)

H1 2024 Update

All the information shown has been extracted by the author directly from the H1 2024 results press release of the company.

Acomo has continued to suffer from extreme cocoa price volatility during H1 2024. In general, sales are flat compared with last year, thanks to spices and nuts, reducing the cost of sales by 0.32%, but administrative and personal expenses grew 11.43%, on top of this, the interest expenses grew a 6.5% due to the higher amount of debt. Shareholders end up with 19% less net income versus the same period in 2023. In the end, the results are in line with the H2 2023 numbers.

Company H1 2024 Results Press Release

H1 2024 - Gross margin: 13.34%, Operating Margin: 4.89%, and Net Margin: 2.66%

H1 2023 - Gross margin: 12.98%, Operating Margin:5.45%, and Net Margin: 3.29%

Image created by the author with data from the company´s annual reports (Author's Own Analysis)

Divisions performance: Spices and nuts: sales increased by 7%, and the segment kept good margins. This part of the business saw a 20% EBITDA growth, all thanks to a mix of increased prices and volume demand.

Edible seeds: this division has seen lower volume demand. The sales have decreased by 7%, but the company managed to partially offset this increasing price. The US is showing signs of a slowdown, instead, Europe saw double-digit growth in its demand. The segment has kept cost controls in place, improving processes that have ended with an improvement in margins.

Organic Ingredients: Floris Wesseling will be the new CEO for this segment starting next September 2024 to try to turn around the current situation as the CEO of the group announced in the press release. Excluding cocoa, the segment performance showed improvements. Again, the US and EMEA showed lower demand.

Tea: this part of the business saw higher sales and volumes, but lower margins as costs surged. The company has indicated that the EBIT and EBITDA values are similar to the 2023 ones.

Food solutions: lastly this division's results are in line with the 2023 ones, the management is planning to expand the facilities of this segment by renting new ones to increase the production capacity, and they expect this extra capacity to be online in 2025.

Balance Sheet:

At the end of H1 2024, the balance sheet shows how the acquisition growth model of the company has changed the composition of its books as the intangible assets and Goodwill now represents 27% of the total assets against the 17% in 2014. The board has been able to grow the equity value at an 11% CAGR in the last 10 years.

In 2023, the interest rate that Acomo paid yearly on its outstanding debt was 8.55%. This translates into expenses of almost 17 million euros last year, which corresponded to 24% of the EBIT. In 2023, the EBIT/Interest payments coverage was only 4.

Instead, in H1 2024, the interest expenses represented 25.3% of the EBIT, which translated to an EBIT/interest coverage ratio of 3.95.

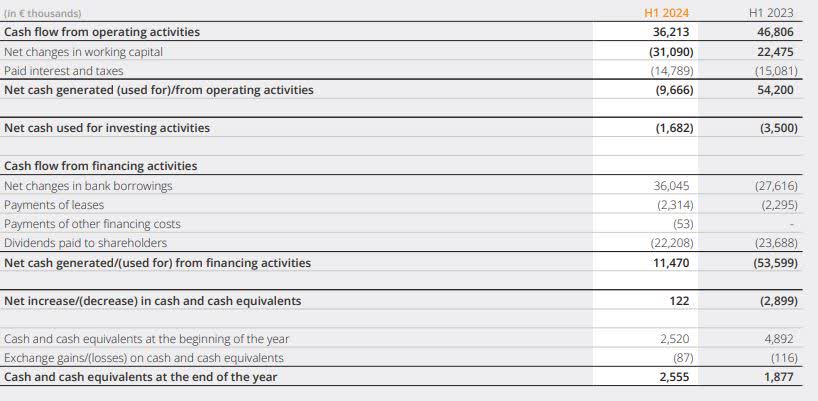

At the end of H1 2024, the outstanding debt amounts to 195.6 million euros. In the last 3 years, the company has done a great job reducing its debt from 337 million euros in 2020. But at the end of H1 2024, this value has grown 18.9% to 232.5 million euros, mainly due to the changes in working capital that usually affect Acomo's first half of the fiscal year.

In my opinion, the group management needs to continue to reduce the amount of debt in 2024 at the current pace to return to its historical net debt/EBIT values of around 2 or even 1.5.

Cash Flow Statement

The operating cash flow has grown at a CAGR rate of 10.7% for the last ten years. In 2023, the company registered a record FCF value due to the positive changes in inventory and working capital. This should be normalized during 2024 and register around 70 million euros in free cash flow, very similar to 2022. If we take last year's FCF as a reference, it has grown at a CAGR of 13% from 2004 to 2023.

The CAPEX shows an asset-light business model that requires a contained CAPEX during the business cycle. On average, from 2014-2023, only 5.6 million euros have been allocated yearly to CAPEX. And, in the last 10 years, Acomo has invested into the business a total of 280.7 million euros in acquisitions and 54.2 million euros in CAPEX.

Acomo shareholders have been rewarded with a dividend growing at a CAGR of 4.94%, and with an average payout ratio of 68% in the last ten years. The number of shares in circulation has increased at a CAGR rate of 2%.

The group's free cash flow has been heavily affected by the net change in working capital. The group has reduced the CAPEX during this period, and to cover the last May dividend, the company took 36.045 million euros in debt.

Company H1 2024 Earning Press Release

Company's Key Financial Information

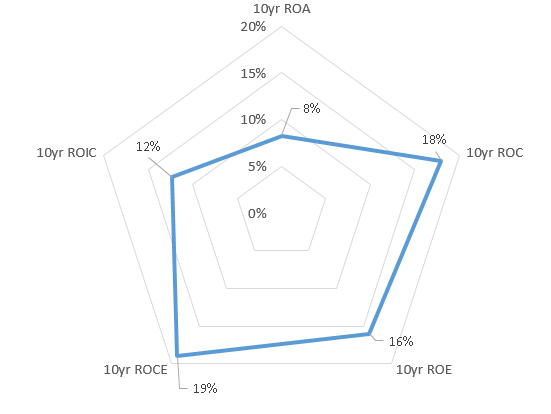

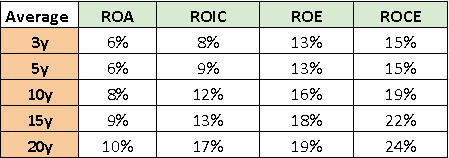

Radar Chart of the 10-year average key return ratios:

Image created by the author with data from the company´s annual reports (Author's Own Analysis)

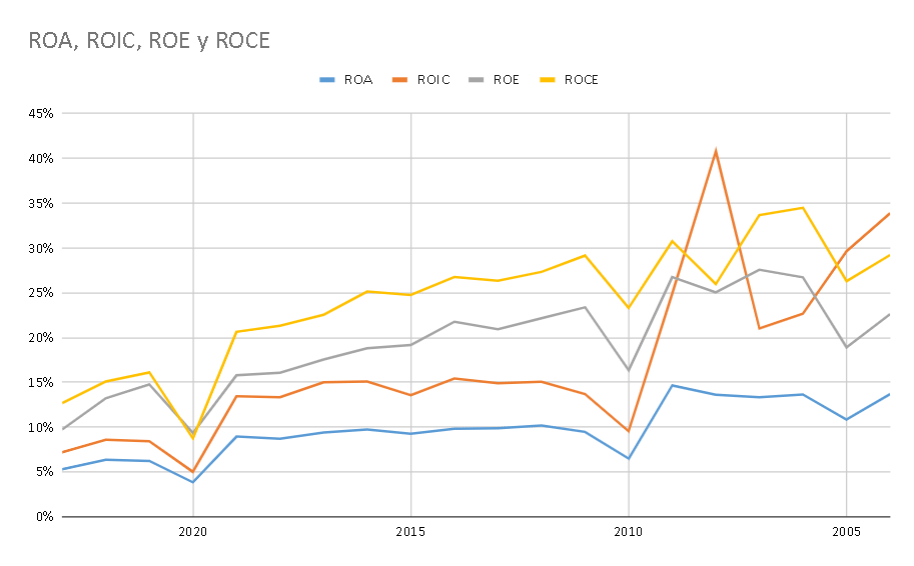

Acomo has seen in the last 20 years how their business profitability and returns deteriorate as they look for further growth by opening new business lines and segments. For example, its ROCE since 2004 has decreased at a CAGR of 4.5%.

Image created by the author with data from the company´s annual reports (Author's Own Analysis) Image created by the author with data from the company´s annual reports (Author's Own Analysis)

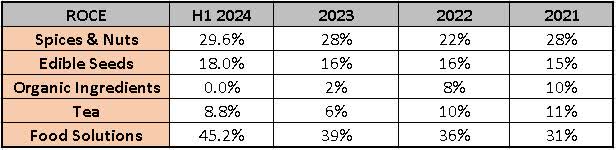

Taking a look at the return on capital employed for each division in the last three years and the data from the H1 2024 press release, we can see the quality of each of these segments and their evolution in time. One thing to be mentioned is that the worst-performing segment is Organic Ingredients. Instead, the two most profitable segments are Food Solutions and Spices & Nuts.

Image created by the author with data from the company´s annual reports (Author's Own Analysis)

Growth Metrics

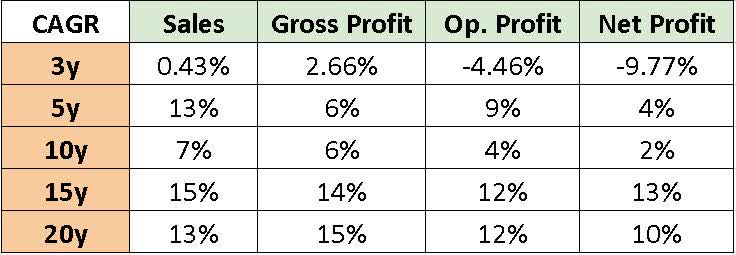

Worth mentioning that 2023 has been a special year with very strong external shocks and events causing the bottom line of the company to be hurt a lot:

Image created by the author with data from the company´s annual reports (Author's Own Analysis)

Regarding growth quality, the company has been able to have stable growth. They have managed to grow 68% of the time on average in the last 10 years and 74% in the last 20 years.

Valuation

Relative Valuation Metrics

Trailing Multiples

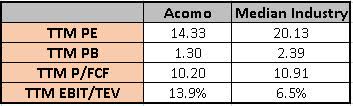

Including the latest H1 2024 results, the stock is currently trading at a TTM price to earnings (P/E) of 14.33 and has a dividend yield of 6.68%. The current price-to-book value is 1.3. If we look at the normalized FCF, the TTM Price to Free Cash Flow (P/FCF), it is currently around 10.2.

The 10-year average PE is 15.04, the dividend yield of 4.82%, the price-to-book value is 1.67 and the P/FCF is 12.22 this means that currently, the stock is trading below its historical valuation.

The market is skeptical about how Acomo is going to turn around this situation. Investors are no longer willing to pay the higher multiples they used to invest in Acomo.

Forward Multiples

Currently, analysts forecast an annual growth CAGR rate of around 6.9% until 2026. The expected P/E ratio for the period from 2023 to 2025 is 10.67, 10.42, and 10.13 respectively for the current share price. Analysts expect a big jump in Acomo earnings for 2024 and then a solid growth rate.

Relative Valuation against Industry

The market is only focusing on last year's bad results, margins, and reduced company profitability. Maybe also the market sees the problem Acomo is having digesting the big 2020 acquisition and the very high cost that comes yearly to service its debt. The market could see this as a more permanent potential threat or deterioration of the business.

Image created by the author with data from the analysts forecasts (Author's Own Analysis)

I believe this level of punishment is unjustified, as the company is taking the right steps towards improving and turning the situation around. The troubles for Acomo are centered on a division that represents 26% of the group's EBITDA in a normal year. Also, the company keeps its core segments firing on all cylinders with historically great profitability and high returns.

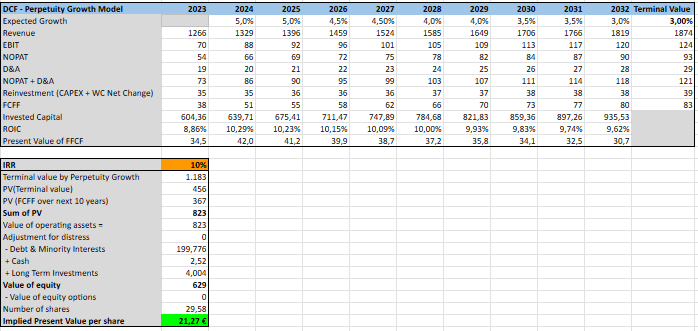

Discounted Cash Flow Valuation

Calculation assumptions:

Revenue growth: looking at the historical data, over the last 10 years, Acomo managed to grow its revenue by an average of 7%. To reflect that the group is now a mature company, I take the 5% rate as the most probable growth rate and, I consider the perpetual rate of growth to be 3%, which, I think, will be the average growth rate of the global markets in the longer term.

EBIT Margin: historical data indicates a margin of 6.6% on average for the last 10 years. Using this period, the business cycle and the last acquisitions can also be reflected in the calculation.

Tax Rate: 25%, is the 2024 Netherlands corporate nominal tax rate.

Reinvestment Rate: in the last 10 years, the firm has re-invested an average of 35 million euros back into the business, with a growth rate of less than 1%.

Investment Rate of Return, IRR: I am not going to use the WACC as I look for a minimum IRR in my positions of at least 10%, and I believe this should be the standard rate of return for an international investor.

DCF Calculation (Author´s Own Analysis)

The DCF calculation gives a target share price of 21.27 EUR for investors looking to get a 10% return on their investment.

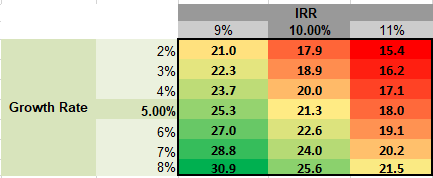

Sensitivity Analysis

To add an extra layer of precaution, I ran a sensitivity analysis to understand the impact of changing the IRR and the rate of growth.

Sensitivity Analysis (Author's Own Analysis)

But, It is very plausible that the stock will touch the big support at 17 euros again until the results reflect that the firm is back on the growth path and the 2020 Tradin Organic acquisition has been completely digested.

Looking Forward

Risks

Commodity Prices Volatility: the company's results are sensible to raw material cost fluctuations as the firm trades multiple commodities such as spices, nuts, dried fruits, edible seeds, tea, cocoa, coffee, and others as a core activity. These products are subject to price fluctuations due to external reasons or events. These changes can potentially impact profit margins if, as in 2023, these costs cannot be passed on to customers.

FX Volatility & Hedge Risk: Acomo operates globally, and one of its main activities is to source and sell products in multiple currencies. Fluctuations in exchange rates affect Acomo's profitability. In addition, FX volatility needs to be managed with hedging strategies to mitigate risks. These hedging activities can incur additional costs and may not fully protect against extreme currency fluctuations, impacting Acomo's financial performance.

Weather Dependency: Acomo activities are quite exposed to weather conditions and climate change. They depend on the yearly crop quality, supply chain disruptions, geographical vulnerabilities, sustainability, etc... Source scarcity is one of the threats that the company could face if climate change continues its progression. All these reasons require Acomo to perform important risk management in their sourcing and trading activities, to invest in adaptive, resilient, and sustainable practices, and to strengthen their collaboration with producers and other supply chain actors to build strong and weather-resistant supply chains.

Future Growth

I believe that future growth will come from the plant-based diets rising tendency, and even governments have started to support this industry. The global shift and promotion of healthier and sustainable eating habits is driving already higher demand for plant-based products. Nowadays, more and more consumers are becoming more health-conscious and environmentally aware regarding food habits. This means, that the market for plant-based food ingredients and solutions will grow significantly in the upcoming years. Acomo, with its extensive range of plant-based, organic, and healthy product portfolio, is well-positioned to successfully navigate this trend.

Another leg that could drive future growth could be the expansion of the business into new geographic markets, providing access to a wider customer base and reducing dependency on specific regions. The entrance of the group into emerging markets with growing middle-class populations can offer significant growth potential. Strategic partnerships and acquisitions can facilitate the entry into one of these new markets. If Acomo enters new markets, I believe the group could materialize higher growth rates in the future.

Conclusion

In conclusion, Amoco N.V. is an interesting niche business playing in a sector with very strong tale winds as plant-based food diets are a very strong rising trend. They have a shareholder-aligned management culture, a long-standing history, experience, and expertise. They execute prudent debt management and solid asset allocation.

On the other hand, I also think that new investors should bear in mind a management business update in the press release of the H1 2024 results that included the following comment from the CEO:

Again, our Organic Ingredients segment was heavily impacted by the cocoa market developments. Although 2023 already showed a sharp increase in market prices, this development became even more extreme in H1 2024. Despite the dedication of our people and all measures taken, the impact of the sharp price increase could not be eliminated. Cocoa market prices remain very volatile, although prices have lately eased somewhat. The cocoa market outlook for H2 2024 remains uncertain, but we may see some improvement in the second half of the year

The management sees some difficulties during 2024, this highlights the dependency of the firm on weather, global supply chain conditions, and commodity price volatility. This is especially true for the Organic ingredients division. All these factors need to normalize for Tradin Organic to get traction again and recover its historical profitability.

I expect Acomo to continue deleveraging, unlocking available cash flow to reward shareholders via higher dividends, and continue growing at its historical pace. In line with this, the CEO mentioned during the H1 2024 conference call that buybacks are not considered as the group is centered on further business expansion. Also, I believe that the group will be able to turn around the situation of its Organic ingredient segment with the new CEO arriving in 2024 Q3. This also would act as a short-term catalyst to enable the stock price to reflect the full value of its business model and future growth potential.

Until then, I recommend readers add this name to their watch list. I think an appropriate entry point under 17 euros will provide a good margin of safety to add this name to the reader's portfolios.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.