Renewer

Heineken (OTCQX:HEINY) (OTCQX:HINKF) released the 2024 half-year results report earlier this morning. At the time of writing, the company stock price is down by more than 7%. Here at the Lab, we firmly believe this decline is unjustified. That said, before reporting our findings and presenting our forward-thinking view, it is crucial to express our unwavering interest in the Heineken investment equity story.

Our long-term overweight target is supported by the company's EverGreen strategic plan, 2) a beer premiumization and EPS growth acceleration backed by a Margin Recovery Story, 3) a solid shareholder base, and 4) a recession-resilient industry with upside in the No-alcohol category division and on the Emerging Market exposure.

H1 Results Earnings

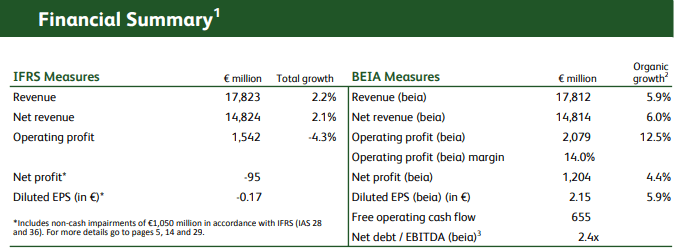

Starting with the Q2 analysis, Heineken had a volume miss compared to Wall Street average estimates. In numbers, the company delivered a Q2 organic revenue of 3.4% compared to the consensus expectation of +6.4%. Looking at the details, this was due to weaker organic volume. However, we should report a stronger-than-anticipated price MIX effect and flat volumes following an adverse weather impact in May and June. In addition, we should also report that Q2 growth was lower as Easter fell in 2024 Q1 compared to Q2 in 2023. In total, the company delivered H1 sales of €17.8 billion, up 2.2%. This is better than our sales forecast. As a reminder, we forecasted a minus 0.6% in Q1 and a plus 1.7% in Q2. Regarding the volume and GEO analysis, Europe and APAC lagged in consensus estimates. In Asia, performance was partially offset by Vietnam's lapping destocking and mid-single-digit growth in India. On the EM, Brazil's shipments were down mid-single digits, with underperformance in the sell-out. Mexico volumes were up, and Africa/Middle East had a positive volume contribution in Nigeria that offset declines in Ethiopia, an area impacted by social unrest.

Going down to the P&L, on a negative note, we take into account the following: 1) net interest expenses were up by 18.5% to €295 million. This was due to a higher net debt position, and 2) a higher income tax expense, mainly driven by a significant one-off benefit in Brazil included last year. This was classified as an exceptional item. Looking at the details, the effective tax rate was 80 basis points higher than last year. In addition, we should report that Heineken reported a net loss of €95 million. This was due to the impairment of CR Beer.

Heineken H1 Financials in a Snap

Source: Heineken H1 press release

Negative one-off apart, Heineken's EBIT grew by 12.5% in H1. However, the company guides for a 4-8% organic core operating acceleration, below the Wall Street average of 8.2%. This implied higher marketing spend and probably higher COGS per hectolitre in H2.

Why are we positive?

Our investment thesis is progressing well. In detail, Heineken delivered:

- Premium beer volume is up by 5.1%, ahead of the total company's beer portfolio in aggregate.

- Further consolidation of Heineken's leadership in the Low & No-alcohol category, which was up by 14% in volume.

- Higher market share penetration despite poor weather conditions.

- A positive confirmation to reach €500 million in gross savings initiatives in 2024. This will enable the company to invest in marketing and new growing categories.

On the financial side, the company Q2 prime MIX was supportive despite an unfavorable channel MIX. In addition, Heineken will pay an interim dividend of €0.69 per share on 8 August 2024, with an ex-dividend date of 31 July 2024. That said, the key to the report is the company's CR Beer non-cash impairment. This negative one-off is reported to be minus €874 million. As a reminder, the company has a 40% equity stake in the Hong Kong listed China Resources Beer. The acquisition price was set at $3.1 billion in 2018. CR Beer's stock price significantly declined; however, the stock price trajectory has deviated from the subsidiary's strong operational performance. In the four years, CR Beer's sales grew by 17%, and its net profit increased by triple-digits. Heineken's premium portfolio backed this. In detail, Heineken received royalties from CR Beer, representing almost 7% of the diluted EPS.

Valuation and Earnings Change

After the H1 results analysis, our 2024 top-line sales, set at €32.56 billion, have not changed. We take into account the fact that the company's volume was sequentially down in Q2. In the Q1 trading update, there was no visibility on Heineken's operating profit, and we are surprised by the H1 performance. However, the company guides higher marketing expenses up by 15% and higher COGS. For this reason, we decided to lower our core operating profit estimate to €4.9 billion from €5.2 billion. The company guidance was unchanged, implying a minus of 2.6% in the H2 EBIT. Last time, we incorporated higher financial charges due to higher taxes in Brazil. Therefore, there is no change in our corporate tax, estimated at 28%. We also slightly increased the company's interest expense, and our EPS reached €5.04.

Looking at our estimates, the company trades at a P/E of 16.4x, with a 22% discount to the Consumer Staples sector. On our twelve-month estimates, valuing the company aligned with its peers at a projected P/E of 20x, we confirmed a buy rating with a value per share of €100.08 versus a current price of €83 per share. There is also a mismatch in YTD performance; the S&P 500 Consumer Staples was up by 5%, while Heineken shares are down by 9%. Heineken's valuation is also not aligned with its five-year historical average (a P/E of 22.27x).

S&P 500 Consumer Staples P/E Projected

Source: S&P Corporate Website

Risks

Here at the Lab, we report our previous risks section (Fig below). Additionally, we should include 1) economic and political stability in the countries where Heineken operates and 2) higher corporate tax from local governments. In addition, we report risks of potential higher excise duty increase or advertising restrictions, highlighting a risk on regulation. The company's Q2 was impacted by poor weather, which impacted beer seasonality consumption. Another downside is the shifts in consumer preference for other competing products, namely spirits and wine.

Mare Previous Risks section

Conclusion

The company has an advantaged footprint, with ample room for growth from beer premiumization and the no-alcohol category. Heineken is improving its market share trends and trades at a discount compared to the Consumer Staples sector. Here at the Lab, we have a long-term view of the company and confirm our buy rating.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.