pkanchana/iStock via Getty Images

I wrote a bullish article on Whirlpool (NYSE:WHR) in March 2024, and back then it was trading for about $106 per share. It has bounced around since—however, in July, it surged up to about $115 per share on reports that another major appliance maker was considering a buyout offer for Whirlpool. Some of that buyout hope appears to have faded, as the shares have fallen back to around the $100 level. In addition to the potential buyout news, the company also recently reported Q2 earnings, so a lot has happened both to the company and to the economic and interest rate outlook since my last article. Here's my updated view and investment strategy with Whirlpool:

I want to start by saying that I still see all of the bullish catalysts that I laid out in the last article as still intact; however the Fed has delayed rate cuts and in my view this has delayed but not necessarily impaired my bullish thesis, which included the potential for interest rate cuts to boost appliance sales. I also was bullish about management's strategy to cut expenses, reduce debt and focus on smaller appliances. After reading Whirlpool's Q2 earnings call transcripts, I believe the company is making progress on all of these fronts, and it remains on track to increase profits significantly in the future with these strategic moves.

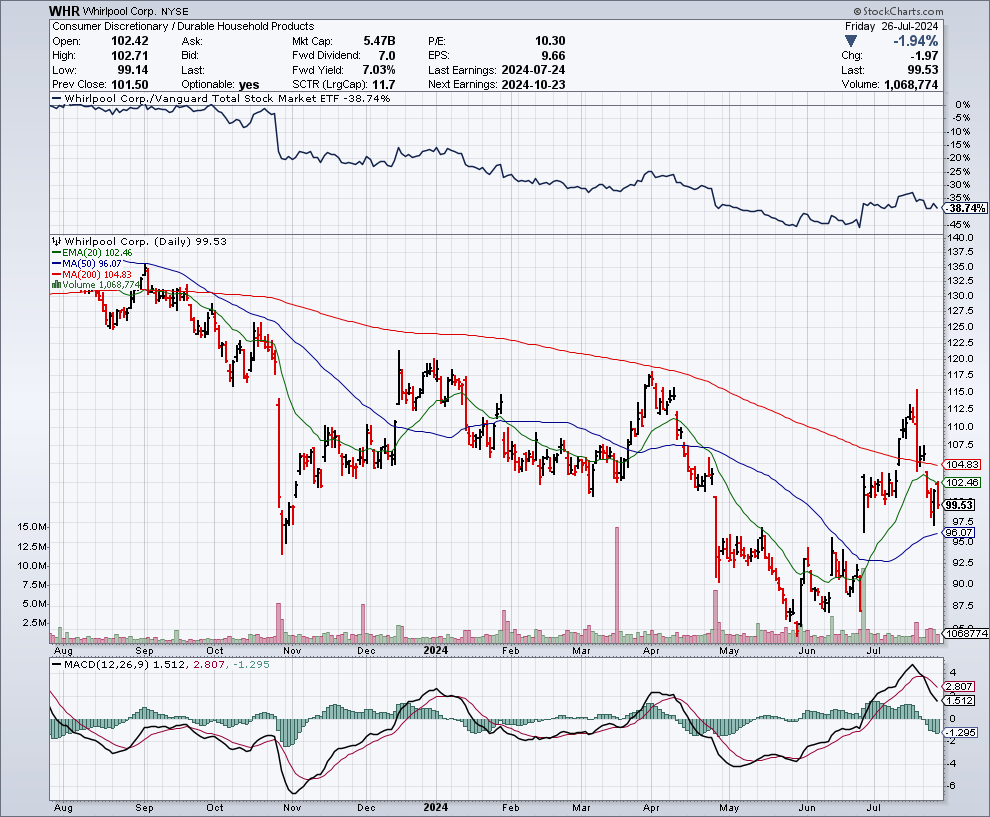

The Chart

As the chart below shows, Whirlpool shares hit the lows for 2024 in June at around $85, but then rallied to around $115 in July. The stock is back down to around $100 per share now, which I view as another buying opportunity. The 50-day moving average is just over $96 per share, and the 200-day moving average is nearly $105 per share. If this stock can generate a sustained rebound back over this $105 level, it would create a very bullish "Golden Cross" formation on the chart, and this could attract the buying interest of technical and momentum traders.

StockCharts.com

My Updated View On The Interest Rate And Economic Outlook

In early 2024, many market participants were hopeful that the Fed would have started cutting rates at least by June, but that has not worked out as the Fed has decided on a higher for longer interest rate policy. Unfortunately, inflation has remained more persistent, and this has caused the Fed to be cautious on moving forward with the first rate cut in years. I think interest rate sensitive companies like Whirlpool will benefit significantly from lower rates. Some consumers need to finance major appliance purchases and are less likely to replace a big ticket item when rates are so high. So lower rates would help take the edge off for these types of consumers, but lower rates will help Whirlpool the most as it could boost home sales activity.

When homes are bought and sold, it is an event that often leads to the upgrading and renewal of major appliances. The real estate market remains deeply impacted and seemingly frozen by high mortgage rates because current homeowners don't want to sell their current home if they have a low interest rate mortgage. In addition, new buyers are in many ways unable or unwilling to pay the high price of buying a home, coupled with mortgage rates that are more than double what they were just about 3 years ago.

There are signs that inflation is cooling rapidly, and there are also signs of looming economic weakness. Many market participants and analysts now believe the Fed is poised to start cutting rates in September. I am concerned that it might already be too late if the Fed waits until September because I don't believe the economy is going to show the full impact of the aggressive rate hiking cycle for a few more months due to the lag effect.

As I point out in this recent article, I see too many warning signs of a looming recession and I am also concerned that the Fed has historically missed projections for how high the unemployment rate will go at the peak of a rate hiking cycle, by about 2.5%. The unemployment rate is currently around 4.1%, and the Fed is expecting it to reach 4.5%. However, if history repeats and the unemployment rate goes 2.5% above the Fed's projections, this would suggest the potential for a 7% unemployment rate and that would not be good for the economy or for Whirlpool. I am increasingly concerned that the Fed has missed the mark once again in terms of lowering rates before the potentially worsening data shows up, and because of this, my bullish view on Whirlpool is more muted than it would be otherwise.

The main reason I have focused on the macroeconomic factors in this article is because I believe Whirlpool is deeply tied to the macro, way more so than most companies, as it depends on the housing market, interest rates, consumer confidence and the labor market.

Q2 Earnings Results And Highlights From The Earnings Call Transcripts

I was impressed with Whirlpool's Q2 earnings results, especially since I have seen some consumer spending weakness from other companies that sell less expensive products. For Q2, it earned $2.39 per share (non-GAAP), which was in line with estimates, and revenues came in at $3.99 billion, which was a beat of $30 million. The company also said it expects to earn $12 per share for the year.

In my view, some of the highlights from the earnings call transcript include: progress on cost reductions, progress, and continued plans in terms of paying off debt, and company management continues to see major potential for improved results in the future after the Fed starts to lower interest rates. I am happy to see the company expects to deliver additional cost savings in the coming quarters, which will help improve margins. The earnings call transcript details some of these positives, and management states:

"As we look ahead, we are confident in our strategy and the favorable long term fundamentals of our business. Our view of the housing market remains unchanged, given the well documented structural under-supply of houses in the U.S. and existing home sales at multi-decade lows, elevated home equity values which are near all time highs, and our strong position with eight of the top ten U.S. builders. We are very well positioned to benefit from the eventual housing rebound and we continue to innovate and have a strong line-up of new products this year that I’m personally excited about, which will support the strength of our brands."

"We took out $500 million of fixed costs since 2019, and with the organizational simplification delivering $100 million in cost savings alone in 2024, we are on track to achieve $300 million to $400 million of cost savings for the year. As we look forward, we continue to see significant opportunity to take additional cost out of our products through input costs, manufacturing, and supply chain."

Why I Am Bullish And Confident On Whirlpool's Earnings Going Forward

In its Investor Day presentation, Whirlpool set a goal for a 10% profit margin in 2026, based on earnings before interest and taxes. This would be up from a projected 6.8% profit margin this year and 6.1% in 2023. Going forward, these profit margin increases are expected to be driven by cost reductions. Based on company revenues estimates for 2026, I calculate that this could translate into more than $20 a share in annual earnings for 2026. The company earned about $16 a share in 2023 and nearly $20 a share in 2022, so there is historical precedence for this level of earnings.

I believe Whirlpool's updated guidance for 2024, projecting $12 per share in earnings, is attainable because we are already halfway through the year, and it is not a stretch for management to see forward for just two more quarters. In addition, the third and fourth quarters are typically the strongest for Whirlpool. Consensus estimates are $3.34 per share for Q3 and $4.11 per share for Q4. Furthermore, the second half of 2024 might turn out better than expected, as the Fed is widely anticipated to lower rates in September. This could start to boost appliance demand in the third quarter and beyond.

Reports Of A Potential Buyout Offer For Whirlpool

Just weeks ago, reports came out suggesting that the German appliance maker named Robert Bosch was talking to advisors about a potential buyout offer for Whirlpool. This pushed the stock up to around $115 per share, but the buyout hopes seem to have faded. Robert Bosch owns a number of brands and has made acquisitions in the past that became very successful under its management. I believe the idea is that the management at Robert Bosch thinks it could strategically improve Whirlpool faster than the current management. I also believe that executives at Robert Bosch must be viewing Whirlpool as undervalued and also seeing the potential for revenues and profits to rebound in the coming years as interest rates decline, and the housing market activity improves as a result of lower mortgage rates.

Whether or not a buyout occurs for Whirlpool, I believe any buyout interest suggests that this company is potentially deeply undervalued. I think this buyout interest is a potential signal to investors that it is time to buy Whirlpool shares at currently depressed and undervalued levels, before management gets earnings back to peak levels and before the housing market returns to a more normal level of activity.

I think a potential suitor could see the same level of undervaluation that I see. Based on $12 per share in earnings, this stock is trading for just over 8 times earnings. This is deeply undervalued, considering the average price to earnings multiple is over 20 times. Whirlpool also appears undervalued to me based on the dividend, which yields about 7%, while the yield on the S&P 500 Index (SPY) is just about 1.26%.

The Dividend

Whirlpool pays a quarterly dividend of $1.75 per share, which totals $7 per share on an annual basis. With the stock currently trading for just around $100, this dividend provides a yield of 7%. I view this yield as extremely attractive, especially when you consider that money market rates currently yield about 5%. Furthermore, a 7% yield will be even more attractive in the next couple of years because the Federal Reserve is projecting that the Fed Funds Rate could be as low as 3% in 2026, and that means money market rates could drop to about 3% as well.

With management expecting $12 per share in earnings, the dividend of $7 per share on an annual basis appears very well covered, and therefore I view it as secure. I also think it is worth noting that earnings for this company could grow significantly from the $12 level in the coming years. This could be fueled by cost reductions and a rebound in the housing market.

In 2022, Whirlpool reported earnings of nearly $20 per share. I believe additional cost cuts will expand margins, the housing activity will rebound after rates drop, and these factors could lead to Whirlpool getting earnings back up to the $20 per share level. If and when this happens, the $7 per share dividend would have a payout ratio of just over 30%, which is very low, and the dividend could be increased significantly.

Potential Downside Risks

I think the potential downside risks for Whirlpool shares are limited at current levels (unless a recession occurs), in particular because I think the recent reports of a potential buyout offer for this company has sent a signal to the market that this stock is potentially deeply undervalued. I think the dividend which provides a yield of 7% is also very supportive of the share price. However, there are macro risks that are increasingly concerning me, and this includes geopolitics, the potential for increased trade tensions and tariffs, and more. We are getting into a less favorable time of year for the stock market in terms of seasonality, and we have what could be a volatile Presidential election coming up in November, all of which could cause a market correction.

As stated earlier, I am also concerned about many signs that the U.S. consumer and the economy are weakening, and perhaps that we could even be going into a recession in the coming months. In this scenario, unemployment could rise significantly and reduce demand for major appliances, leading to downside for Whirlpool shares and the stock market in general.

In Summary

I think Whirlpool shares are deeply undervalued, and the dividend yield is extremely attractive at 7%. The possible buyout interest for this company only confirms the beliefs I had when I wrote the last article on Whirlpool. I think some very savvy industry executives in Germany were possibly seeing this as an ideal time to buy a company that has significant earnings upside potential that could be fueled by strategic improvements and the increasing odds of lower interest rates which would boost the housing market and appliance sales in the years to come.

With everything I see at Whirlpool in terms of potential, I want to buy a significant stake, but what will keep me from getting carried away is my concern for a recession. So, my plan is to buy more shares now at around $100, and I will add on weakness, and get paid a very generous dividend while waiting for a higher share price.

No guarantees or representations are made. Hawkinvest is not a registered investment advisor and does not provide specific investment advice. The information is for informational purposes only. You should always consult a financial advisor.