Luis Alvarez

I am updating my analysis on GoodRx Holdings (NASDAQ:GDRX) in advance of Q2 2024 earnings, which will be released pre-market on Thursday, August 8th, 2024.

In my previous analysis, I rated GoodRx a sell for the following reasons:

- GoodRx was facing industry headwinds across every part of the business

- Cost growth was rapidly outpacing revenue

- The business needed a 10%+ growth rate just to justify the price at the time.

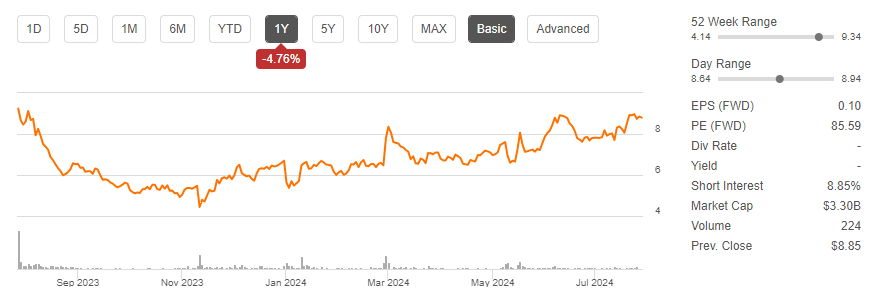

Since then, the stock has yielded 46% while the S&P 500 has yielded 18%.

GDRX Price Trend (Seeking Alpha)

I clearly missed the mark on the short-term performance, although I still believe the same long-term thesis.

As of now, I expect Q2 earnings to be in line with guidance and the results to be acceptable. However, I don't believe the long-term guidance supports the current price point. Even at the high-end growth rate of 12%, the price target is barely above current pricing, while the low-end of guidance suggests a 30% downside.

The business continues to face significant headwinds and isn't getting traction fast enough despite only having 2% market share for the core business. While there is upside potential from some initiatives that management has laid out but not counted in guidance such as GLP-1, I see this more as plugging gaps in growth based on how tight the current price target is.

With all of the above in mind, I maintain my sell rating at an average price target of $7.50, 13% downside from today's pricing.

Q2 Earnings Preview

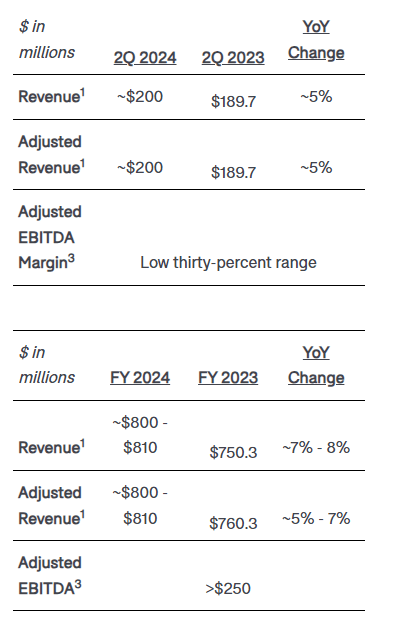

GoodRx is expected to announce EPS of $0.09 and revenue of $200.48M, both up sequentially.

GDRX Earnings Summary (Seeking Alpha)

Taken in combination with Q1, revenue is pacing in line with management guidance for the full year, although AEBITDA looks to be pacing slightly behind.

GDRX 2024 Guidance (GDRX Investor Relations)

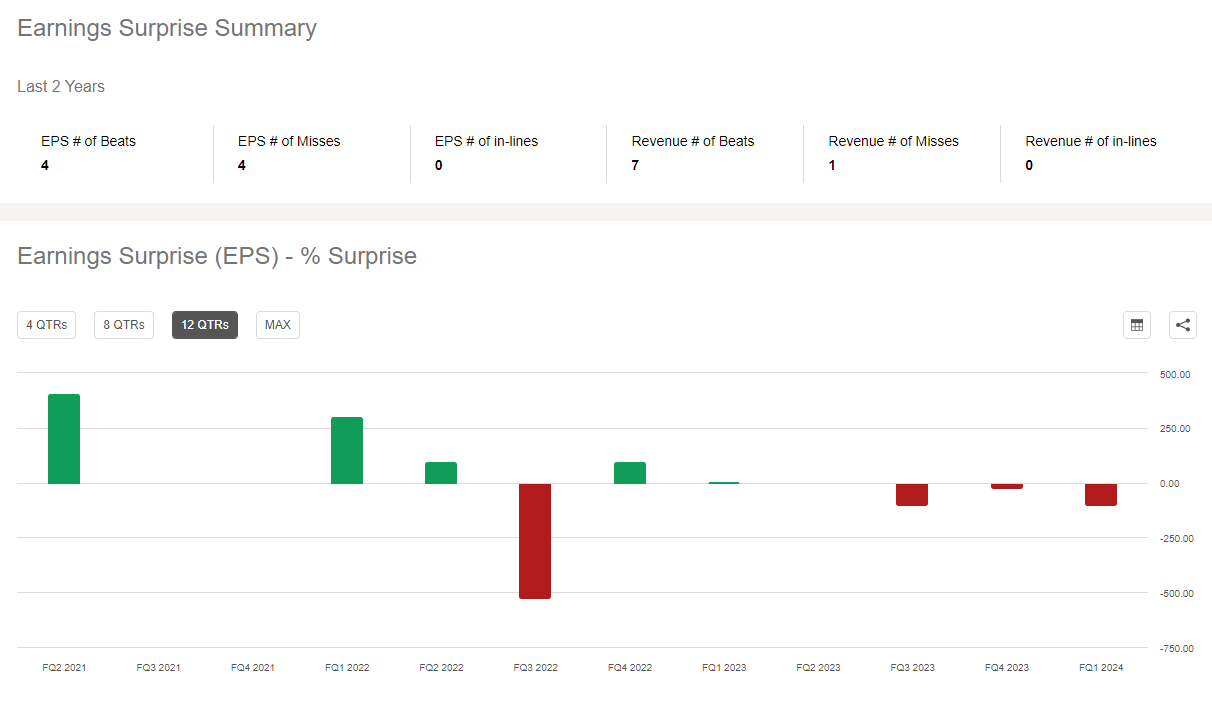

Management is consistent with revenue guidance, 7 beats, and 1 miss, but hit or miss with EPS guidance, 4 beats, and 4 misses. Coming out of the recent investor conference and with no major news, I don't expect huge swings from consensus.

GDRX Earnings Surprise (Seeking Alpha)

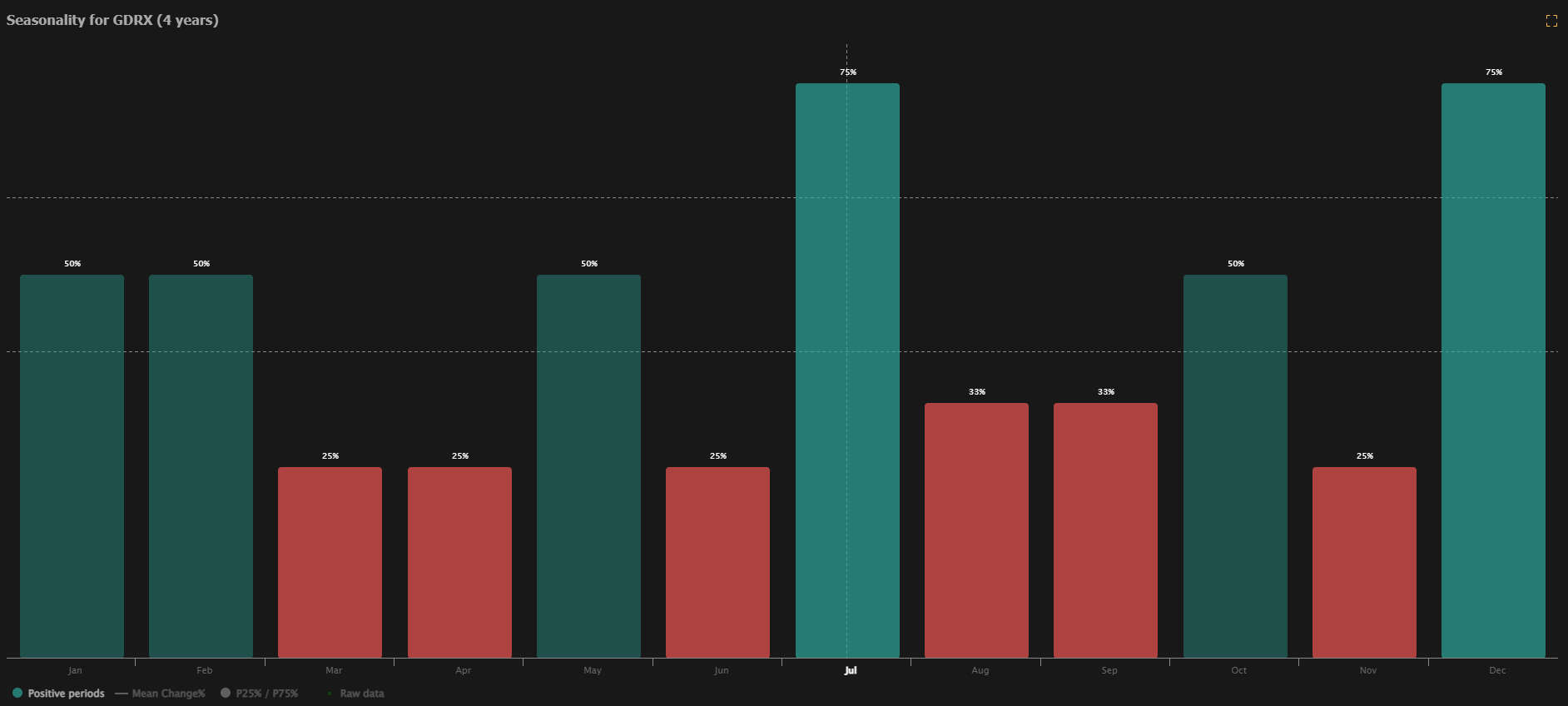

It is also worth noting that we are heading out of a historically strong trading month and into four historically weak trading months for the stock.

GDRX Seasonality (TrendSpider)

As earnings are released, I will closely be looking at revenue trends for each of the three businesses, as well as overall cost management and how they align with management's 3-year targets. This will signal the overall growth potential of the business and inform any adjustments to the valuation.

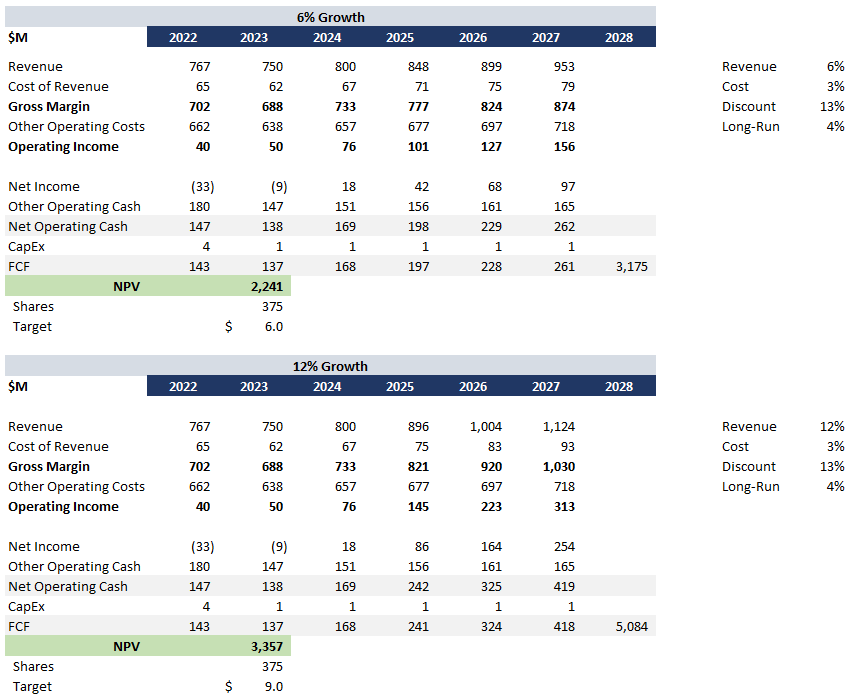

Valuation

I updated my ongoing valuation analysis based on new trends and guidance. In the first of two scenarios, I assume the bottom end of management's guidance at a 6% revenue growth rate. In the second, I assume a 12% revenue growth rate. I made the following overall assumptions:

- Discount rate of 12.5% based on current WACC.

- Revenue growth of 6 or 12% in line with low and high-end of long range guidance (slide 130).

- Cost growth of 3% in line with average inflation.

- Long-run growth of 4% based on overall market long-run growth net of cost growth.

This analysis yields a price target of $6 - $9 per share or 30% downside to 4% upside.

GDRX DCF (Data: SA; Analysis: Mike Dion)

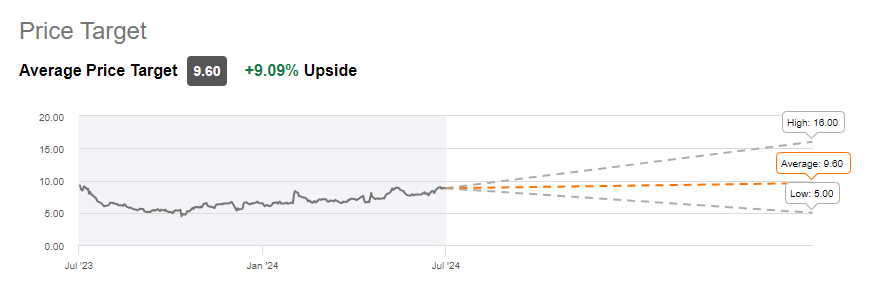

Wall Street has taken a higher price since investor day, $9.60 versus my high end of $9.00, although the full DCF range still sits within the overall price target range.

GDRX Wall Street Rating (Seeking Alpha)

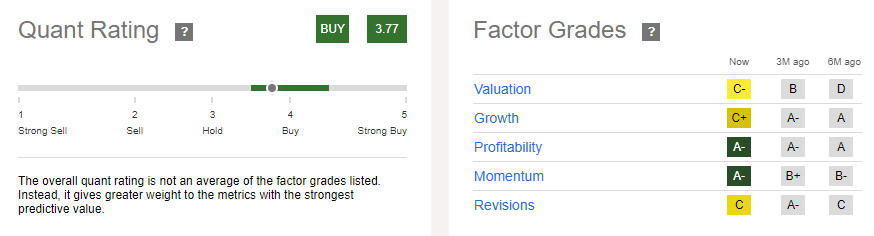

The quant rating is signaling a buy based on profitability and momentum. From a profitability standpoint, GoodRx is not directly comparable to other Health Care technology companies, so this is apples to oranges. Valuation and growth are (fairly in my opinion) signaling a hold.

GDRX Quant Rating (Seeking Alpha)

Headwinds Persist

GoodRx's primary role is to help consumers lower pharmaceutical costs. Other options for lower costs continue to expand. These other options also don't typically require the extra step of GoodRx.

- Cost Plus, CVS, and Amazon are moving to a fixed-price prescription model based on the price they paid for the drug plus a nominal markup.

- Medicare is being allowed to negotiate costs with drug providers.

- Bipartisan legislation targeting pharmacy benefit managers (PBM) is moving forward.

All of these trends undermine GoodRx's value proposition to some degree. As pharmaceuticals become more affordable or as discount options exist within existing care plans, consumers are less likely to add this extra step

GoodRx Is Struggling To Take Market Share

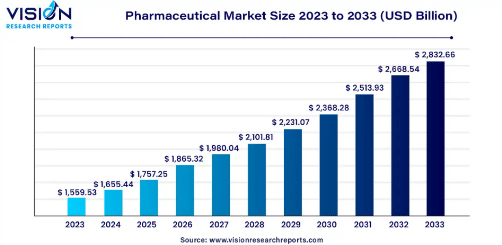

The overall pharmaceutical industry that GoodRx works within is expected to grow at an average CAGR of 6.15%. If GoodRx keeps up with the market and maintains its share, this should be the floor of its growth.

Pharmaceutical CAGR (Vision Research Reports)

Unfortunately, GoodRx's growth tapered off significantly starting in 2021. From 2021 thru 2023, revenue was essentially flat. From 2023 to 2024, revenue is forecasted to grow just over 6%, essentially in line with the market.

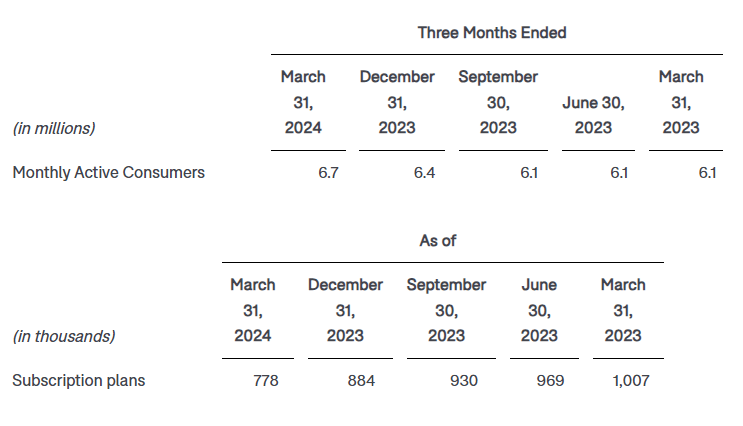

Year-over-year, monthly active consumers increased by 10%, but this was partially offset by a rapid decline in subscription plans, which provides much-needed stability for the business.

Operating KPIs (GDRX Investor Relations)

GoodRx is struggling to keep up with the market, let alone outpace it, but it needs to grow at least double the market rate to support the current price target. If the business can barely keep up with the market with all of their strategies in place, then I don't believe they are anywhere close to doubling the market.

Upside Potential

On the upside potential, GoodRx could sign a major corporate or insurance partner similar to the Kroger deal that would provide a pool of continuous customers. This would have to go hand in hand with strong execution on all current strategies, as they need to double the market and then grow on top of that.

As discussed above, upside potential is mitigated by industry headwinds that I don't believe management has fully considered in the long-term guidance range.

Verdict

GoodRx has struggled to keep up with the pharmaceutical market, but needs to double market growth to support the current price target. With regulatory and consumer focus on prescription drug prices, we are starting to see more and more initiatives targeting the industry that undercut GoodRx's core value proposition. At the highest end of management's guidance with 12% growth, DCF analysis suggests a minimal 4% upside. Keep in mind that GoodRx hasn't hit growth rates that high in years.

While there is upside potential if every part of the strategy hits, it is largely mitigated by the industry headwinds on prescription drug pricing. With all of the above in mind, I maintain my hold rating at an average price target of $7.50, 13% downside from today's pricing.