Reinhard Krull/iStock via Getty Images

Introduction

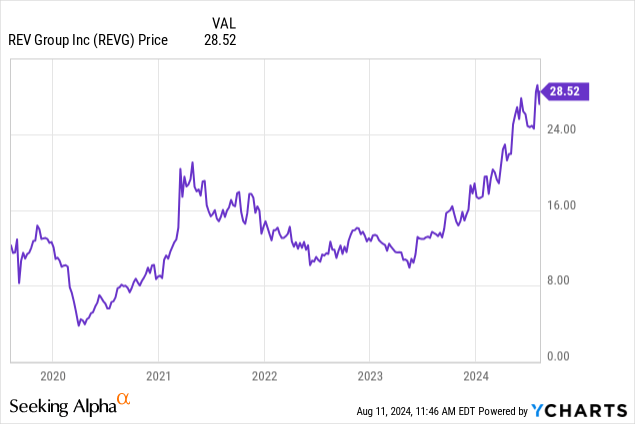

REV Group (NYSE:REVG) is a US designer, manufacturer, and distributor of speciality vehicles and other aftermarket services. Over the past 5 years, shareholders have seen a 172% rise in the share price, significantly beating the S&P 500. A significant proportion of this increase has occurred in the past year, with the shares up almost 144%. This raises the question of whether the shares have further upside. With a strong Speciality Vehicles segment with rising margins and the divestiture of its Collins bus business, the company is focused on providing value to shareholders. With this in mind, I give the shares a "buy" rating.

Company Overview

REV Group is a leading manufacturer of specialty vehicles, headquartered in Brookfield, Wisconsin. The company, established in 2010, has quickly become a key player in the niche markets it serves, which span across fire and emergency, and recreation vehicles. REV Group's diverse portfolio includes well-known brands such as E-ONE, and KME in the fire and emergency sector, and American Coach and Fleetwood in the RV segment.

Operating through two distinct business segments - Speciality Vehicles and Recreational Vehicles - REV Group's strength lies in its ability to cater to specific industry needs with high-quality, customizable vehicles. The company's fire and emergency division, which accounts for a majority of its revenue, benefits from long-standing contracts with municipal governments and other public agencies, ensuring a steady stream of demand.

With manufacturing facilities spread across the United States, REV Group maintains a strong production footprint, allowing it to leverage economies of scale while remaining responsive to customer requirements. Despite facing competition from both larger diversified manufacturers and smaller niche players, REV Group's focus on specialized vehicles has enabled it to carve out a strong competitive position. As the population of the US both grows and ages, demand for specialized vehicles is set to rise, placing REV Group in a favourable position.

At the end of January 2024, REV Group sold its Collins Bus division for $303 million in cash. This helped streamline the company's operating structure, allowing the company to focus on the divisions where its strengths lie, providing opportunities for improved margin performance, strengthening its balance sheet, and boosting shareholder returns in the long term.

Speciality Vehicle Strength

REV Group's largest sales category is speciality vehicles, in particular the sale of Fire and Ambulance vehicles. This division has grown following a series of bolt-on acquisitions since 2006. This has led REVG Group to become one of the largest suppliers in this segment, boasting an estimated 30% market share for fire vehicles and 50% for ambulances in America.

The Speciality Vehicles segment offers an attractive business for a number of reasons. Firstly, these brands tend to command local monopolies in their respective market, due both to customer loyalty and to ensure standardised training on the equipment. With fire and ambulance demand being consistent, this ensures that orders will always occur even during recessions. The overall market for REV Group's speciality vehicles is only growing because of increased demand from an ageing population and overall population growth. Following industry consolidation, REV Group has benefited from reduced competition, allowing greater control over pricing, and improved pricing power.

With a consolidated industry and consistent demand, REV Group is in a strong position for future profitability. However, an even bigger driver of margin expansion and future profitability is the large backlog in speciality vehicles. Following significant supply disruptions post-pandemic, vehicle deliveries were reduced, restricting potential revenue and profits.

Combined with a significant increase in orders as towns and cities emerged from pandemic austerity, this has led to a significant backlog in vehicles. This is not unique to REV Group, but is an industry-wide phenomenon, helping support margins across the industry. As of their quarter two results, REV Group had a backlog of $4.1 billion, up from $3.4 billion a year earlier. This underscores the order strength for vehicles in the Speciality Vehicles segment and the potential for REV Group to raise prices, helping to boost margins. With this increased backlog growth, the resulting improved pricing and higher margins will only be seen once vehicle deliveries occur in the coming quarters.

REV Group's Speciality Vehicles segment is on a strong trajectory, with the potential for substantial growth in the coming quarters, driven by a significant backlog, favorable industry landscape, and strong pricing power. As this occurs, investors can expect to see continued improvement in margins, giving REV Group the potential for improved shareholder returns.

Q2 Results

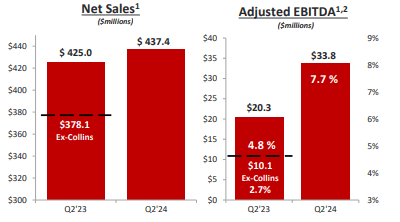

On June 5th, 2024, REV Group released its Q2 2024 results, showcasing a generally positive set of results. Revenues beat, coming in at $616.9 million, down 9.4% year-on-year. However, when we exclude the Collins Bus division which was sold earlier this year, revenues were only down around 3%. Despite this fall in revenue, net income excluding the Collins Bus division was actually up 18.3% to $37.5 million.

With a significant increase in net income with only a small change in revenue, this led to a jump in adjusted EBITDA margins from 5.0% to 6.1%, again excluding the recently sold Collins Bus division.

Performance by segment showed variation. The Speciality Vehicles segment which incorporates the fire and ambulance units led the way with both revenue and adjusted EBITDA growth, despite the sale of the Collins Bus division which was in this segment. Increased shipments of fire trucks and ambulances boosted revenues and, combined with higher price realisation, margins in this segment grew from 2.7% excluding Collins Buses to 7.7%. This underscores my thesis that significant backlogs for speciality vehicles across the sector will lead to higher price realisation, revenues, and boosted margins. Although REV Group posted higher deliveries in this quarter compared to the previous quarter, the backlog for speciality vehicles continued to grow, reaching $4.1 billion, up from $3.4 billion a year earlier, underscoring the positive future outlook for this segment.

(REVG Q2 2024 Earnings Presentation)

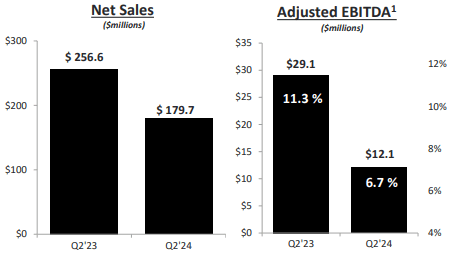

One area of weakness was the Recreational Vehicle segment. Sales fell 30% year-on-year to $179.7 million. This decrease in revenue resulted in a fall in adjusted EBITDA to 12.1 million, down almost 60% compared to the previous year. Adjusted EBITDA margins in this segment were down 40% to 6.7%. This was due to a significant fall in shipments and net sales, with only a small offset from labor efficiency improvements. With this division particularly sensitive to economic conditions and consumer confidence, the outlook remains mixed as the American consumer begins to falter. The RV segment made up around 30% of profits and revenues in this quarter; however, any further weakness should be offset by continued growth in the Speciality Vehicles segment.

(REVG Q2 2024 Earnings Presentation)

Management narrowed their guidance for this year's revenues to $2.4 billion to $2.5 billion, a slight decrease year-on-year, largely due to the sale of the Collins Bus division and weakness in the RV segment. Adjusted EBITDA is guided to be in line with last year, at around $151 to $165 million. Following the results release, a dividend of $0.05 was declared for the quarter.

Overall, REV Group's results were broadly positive, especially when considering the headwinds faced by the RV segment. The strong performance in the Specialty Vehicle segment, driven by increased demand for fire trucks and ambulances, and improved price realization, helped offset the challenges in the Recreational Vehicle segment. The growth in margins and net income, underscores the company's strengths and positive outlook for the Speciality Vehicles segment.

Valuation

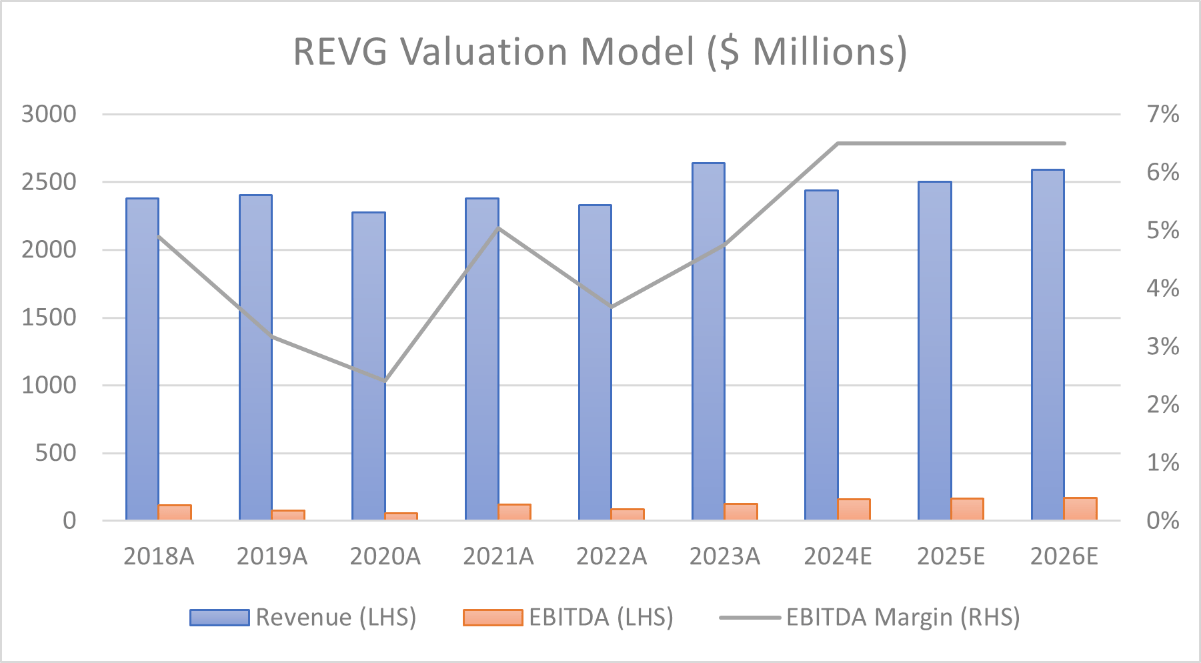

To value REV Group, I employed an EV/EBITDA methodology for the period to 2026. I assumed the share count would remain constant at 51.9 million and for purposes of simplicity, I assumed cash and debt levels remain constant.

Over the past 5 years, REV Group has had an average EBITDA margin of 4.8%. Over the past 12 months, this has increased to 5.5% due to strength in the Speciality Vehicles segment. With continued strength in the Speciality Vehicles segment due to a growing backlog, improved throughput, a positive industry outlook, and rising prices, I believe this can rise further over the coming years to an average of 6.5%. For future revenue, I used analyst estimates on Seeking Alpha, given their comprehensive industry insight and knowledge of market trends.

Created and calculated by the author based on REV Group's Financial Data found on Seeking Alpha and the author's projections

To determine an exit EV/EBITDA multiple, I took the midpoint of the company's 5-year average of 13.82 and the industry average of 13.36, giving an exit multiple of 13.36. This method to determine the exit multiple balances REV Group's historical valuation multiple, with that of similar companies in the wider industry. This takes into account both trends in the industry, REV Group's valuation compared to peers, and REV Group's historic performance.

Performing the calculations implies a market cap of $2.03 billion at the end of 2026. With an estimated 51.9 million shares outstanding, this corresponds to a price target of $39.18 per share, an upside of 37% from the current price of $28.52 per share, for a CAGR of 15.4% over the next 27 months.

Risks

When considering an investment in REV Group, there are several key risks I believe it is important for investors to consider which could impact the company's performance and, by extension, its share price.

Firstly, the thesis for investing in REV Group hinges significantly on the expected strength of the Speciality Vehicles segment to help drive margin growth. However, if this segment fails to perform as anticipated, it will have a detrimental impact on the company's margins and profitability growth. This segment is vital due to steady demand from municipal orders, but any downturn, whether from throughput issues or a decline in contracts, could undermine margin expansion.

Secondly, the company could face challenges in supply chain inflation and production inefficiencies. While REV Group has managed to pass higher costs to customers over the past few years by increasing backlog pricing, there is a risk these higher prices may not fully offset cost increases, putting pressure on margins. Given the nature of REV Group's business, if some parts are late or assembly is delayed, this will impact their vehicle production and profitability.

Additionally, the recreational vehicles segment is under strain, particularly as demand for recreational vehicles (RVs) has declined from the peak following the pandemic. Despite this, RV sales are set to be higher in 2024 compared to 2023, but with signs suggesting consumer demand may be weakening, RV sales could decline in the future. A prolonged downturn in these segments would not only weaken revenue and profitability but could also lead to a downward revaluation of the stock.

Conclusion

Despite the potential challenges that could face the RV division if the American consumer weakens, the positive outlook for the Speciality Vehicles segment more than covers for any weakness. With margin expansion taking place, evident from the company's latest quarterly results, the stock appears undervalued. Given these factors, I assign the shares a "Buy" rating.