PM Images

Investment summary

My previous investment thought for Paycom (NYSE:PAYC) (published on 20th May 2024) was a buy rating because I believed in the strong pricing power that PAYC has, given the value proposition it offers its users. In addition, the revision in sales strategy should yield more positive cross-sell opportunities. I stand firm in my view for PAYC (buy rating), as the new sales strategy seems to be working very well, and this should help drive growth acceleration in 2H24.

2Q24 results update

PAYC reported 2Q24 (results out on 31st July) revenue growth of 9.1%, with recurring revenue growth of 9.1% and implementation & other revenue growth of 7.5%. Total revenue came in at $437 million (of which $430 million was recurring revenue). Adj gross margin saw 81.8%, a 220bps decline vs. 2Q23, mainly due to increased hiring and an additional depreciation contribution from PAYC's fifth building. This impact also trinkled down to the adj EBIT line, which saw 330bps compression from 30.6% last year to 27.3% this quarter. Balance sheet-wise, PAYC ended the quarter with $346.5 in net cash (no debt).

Growth acceleration in 2H24 is possible

PAYC revised guide implies 10% y/y growth at the midpoint for FY24 (range between $1.86 and $1.875 billion), and the growth cadence assumption is that 3Q/4Q24 will see growth acceleration (3Q24 guided for ~10% growth, which means 4Q24 is implicitly guided for 11% growth). The problem with this guide is that PAYC has reported growth deceleration for most of the past two years (from 30.9% y/y in 2Q22 to 9.1% in 2Q24), and I believe many investors are skeptical that growth will reaccelerate, especially with the current macro uncertainty.

I am taking the leap of faith that PAYC will see growth accelerate to meet its FY24 guidance. And I say this because management has executed very well on the new sales strategy. To briefly recap (quoting from my previous post), the new sales strategy requires customer relationship reps [CRR] to make sure all modules sold to a customer are fully utilized before allowing any more cross-selling, and importantly, the CRR will not receive their commission payment until the module has been used for 30 days. This heavily incentivizes the CRR to see through the entire lifecycle of that sales process, which should improve customer satisfaction and, in turn, lead to customers wanting to adopt more PAYC solutions as they become more proficient.

In less than six months since launch, PAYC is already seeing very positive results from this change. Specifically, PAYC sold 24% more units in 2Q24 vs. 2Q23 and is seeing increasingly more returning clients (which ties back well to my point that as customers become more proficient, they will adopt more PAYC solutions). An important point to note here is that it takes time for the sales team to be “mature” on this strategy, which can be seen from the data that year-to-date sold 15% more units sold vs. 2Q24 that saw 24% more units sold (i.e., implies that 2Q24 improves significantly from 1Q24), and so 1H24 performance is not a good benchmark to think about 2H24 growth potential. Two additional data points that lend credence to my view are: (1) PAYC saw its top sales week in its entire operating history (in July, which is part of 3Q24); and (2) PAYC added the most number of new sales reps in July. There are two aspects to consider here. One is that the sheer increase in the number of sales reps means more capacity to win deals. The second is that as they mature (using the same timeline as what we see in 1H24—2Q24 saw better unit sales than 1Q24), 4Q24 is likely to perform better than 3Q24 (the same acceleration trend).

To top it off, 2H24 faces an easy growth comp given that 2H23 was relatively weak compared to 1H23; hence, growth acceleration is certainly possible in 2H24.

Capital return story gets better

In my previous model, I did not take into account capital returns, and this seems to be an area that deserves highlighting. If you look at the past few quarters, management has significantly stepped up its share purchase trend (4Q23 share count down 110bps y/y; 1Q24 down 230bps y/y; and 2Q24 down 250bps y/y). Management doesn’t seem to be scaling back on returning capital as they bought back a significant amount in 3Q24—574k shares since July 1, which is about a ~1% decline vs. shares outstanding in 2Q24. Looking ahead, the capacity for stock repurchases has been increased and extended, now with $1.5 billion available for repurchases through August 2026, up from the previous authorization of $676 million. This is massive, as the amount represents ~17% of PAYC's current market cap (~$9 billion).

There should be no issue with PAYC funding these share repurchases as the balance sheet remains strong with no debt (a net cash position of ~$350 million) and FCF margins have remained healthy at 20% for the past two quarters. As the economy gets better (more hiring activities, which drive more payroll activities), increased revenue size should drive FCF growth accordingly. For a quick comparison, as per consensus estimates, PAYC is expected to generate ~$1 billion in FCF between FY24 and FY26.

Yeah. No, I mean, as we mentioned on the call, I mean, we bought back a significant amount of shares and we actually bought back 574,000 just during Q3 in a large amount since July 1st. So really an opportunistic approach to the buyback.

We opportunistically took advantage of the low stock price to repurchase approximately 790,000 shares between April 1st and July 31st for $120 million. 2Q24 earnings transcript

Valuation

Redfox Capital Ideas

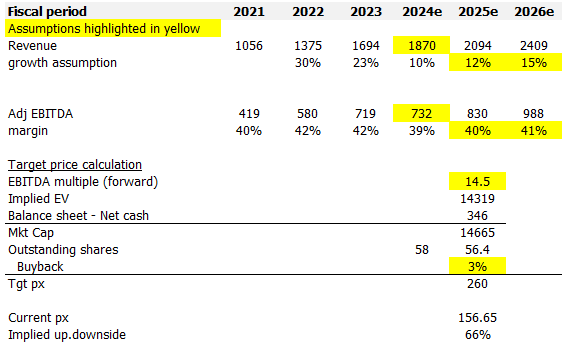

I model PAYC using a forward EBITDA approach, and using my assumptions, I believe the upside for PAYC’s stock is attractive. Like what I have shared previously, growth acceleration back to >20% is unlikely in the near term, but the path towards growth acceleration has certainly become more visible given the results from the new sales strategy. As such, I reiterate my growth assumption for FY24 (per guidance) and FY25: 12% growth (if I am right about the growth acceleration for 2H25, 4Q24 will exit at ~11% growth), followed by mid-teens growth in FY26 (assuming that growth gradually accelerates towards 20% over time). I also reiterate that I am not assuming massive price hikes for PAYC’s BETI module. I also expect the adj. EBITDA margin to improve back to >40% as PAYC’s sales reps become more mature and as growth accelerates.

The other leg that drives an attractive upside is multiples re-rating back up to 14.5x forward EBITDA (PAYC’s past 12-month average). Given that PAYC was valued at 14.5x in 4Q23 through 1H24, where growth was decelerating from a high-teen percentage (17.3% in 4Q23) to ~10%, I think this re-rating is possible as growth (as I modeled) is accelerating towards 20%.

The last leg is the capital returns, which I have reflected in the 3% share buyback rate for FY25.

Risk

I reiterate the risk I mentioned in March, in that near-term growth performance is still largely pegged to how the economy performs and how much any of the recovery will translate into additional hiring.

PAYC revenues remain linked to employment levels within the client base. In the event that there is a prolonged period of depressed employment levels (in a big recession), PAYC growth will be heavily impacted as: (1) companies reduce the number of employees; (2) companies shut down; (3) there will be less incorporation of new companies; (4) PAYC will not be able to cross-sell products as effectively as it has done so in the past.

Conclusion

My view for PAYC is a buy rating as the new sales strategy is showing tangible results, with increased unit sales and returning customers. This, combined with an easier growth comp base in 2H24, positions PAYC for potential growth acceleration. PAYC is also stepping up its share repurchase program, which is another plus point for shareholders.