Mario Tama

Altria (NYSE:MO) is scheduled to announce Q2 earnings results on Thursday, July 28th, before market open.

The consensus EPS Estimate is $1.25 (+1.6% Y/Y) and the consensus Revenue Estimate is $5.42B (-3.2% Y/Y).

Over the last 2 years, MO has beaten EPS estimates 75% of the time and has beaten revenue estimates 50% of the time.

Over the last 3 months, EPS estimates have seen 3 upward revisions and 9 downward. Revenue estimates have seen 6 upward revisions and 2 downward.

The downward revisions to the EPS estimates reflect investor expectations of lower profitability for the tobacco giant in a quarter beset by legal troubles at e-cigarette maker business JUUL, overall weakening in traditional tobacco sales and macro uncertainties such as rising inflation.

Altria (MO) in late April reported a mixed set of Q1 numbers and reaffirmed its FY adj. EPS guidance.

Barclays in late June downgraded MO stock to underweight and called the company a declining business. "We see Altria as a melting ice cube, i.e. entering a decline that will be hard to reverse, similar to newspapers, cable companies and printers, so we believe it deserves a low multiple," Barclays analyst Gaurav Jain had said.

The U.S. Food and Drug Administration in June had ordered a ban of all JUUL products off the shelves in the country, but then temporarily stayed the order in July while it was being appealed.

Earlier in July, Altria (MO) reportedly raised cigarette prices in a move to support Q3 profitability.

Investors have also been attracted to MO stock due to its lush dividend yield.

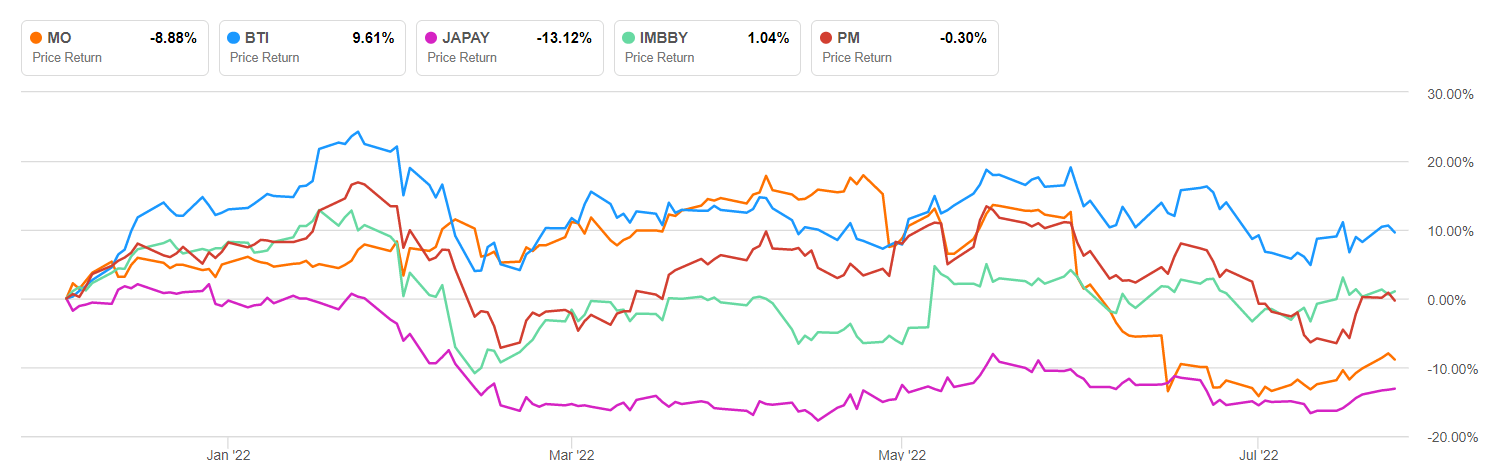

MO has been one of the worst performers in terms of YTD price return performance compared to rivals British American Tobacco (BTI), Japan Tobacco (OTCPK:JAPAY), Imperial Brands (OTCQX:IMBBY) and Philip Morris International (PM):