Investment Thesis

Work from home due to the well-documented virus issues is likely to cause a surge in PC sales, and perhaps also data center expansion. This, of course, will benefit Intel (NASDAQ:INTC). Intel had been struggling with shortages in 2018-2019 due to supply constraints, but new capacity has been ramping up, just in time to fill a (potentially) new demand surge in 2020 as PCs become vital to power the work from home paradigm.

In such economically uncertain times, people may also be more inclined to stick to their current suppliers, which may slightly slow AMD's (AMD) Ryzen and Epyc ramp down. In any case, I expect Intel to reach its 2021 financial targets this year already.

As a 'beneficiary' of the coronavirus, Intel is likely to recover faster than most others from the market sell-off.

PC, data center demand surging

PC

In its January earnings call, Intel had already predicted an unusually (record) high Q1 due to the cloud buying cycle as well as demand from the Windows 10 refresh. However, the company expected both factors to recede in the second half of the year. Intel expected the PC to be down slightly this year.

Nevertheless, there is now also the coronavirus factor. As for example this article cites:

"Demand for PCs is booming thanks to teleworking and remote learning measures introduced around the world to combat the coronavirus pandemic."

Intel so far has not adjusted its outlook. The company said it is operating on a relatively normal basis.

Data center

As people get more active on the internet, data center and memory/storage demand could possibly also further increase or accelerate. As these articles illustrate:

As Traffic Surges, Akamai Will Shift Gaming Downloads to Off-Peak Hours

As governments have limited public activity to promote social distancing, businesses have directed employees to work from home, and schools and universities are moving classes to online formats.

"The Internet is being used at a scale that the world has never experienced," wrote Tom Leighton, the CEO and co-founder of Akamai, in a blog post. "This increased usage is causing concern about whether the Internet will be able to continue handling the ever-increasing amounts of traffic. As a result, some major regulators, carriers, and content providers are taking steps to reduce load during peak traffic times in an effort to avert online gridlock."

DigiTimes: Server demand remains strong

The server and datacenter sector has been almost immune to the coronavirus, with demand being boosted by remote working and learning, online gaming and shopping in the wake of the pandemic.

Microsoft Cloud Use Soars 775 Percent Amid COVID-19 Social Distancing

Microsoft is one of the largest players in the market for data center services. It often builds its own data centers, but in recent years has begun leasing wholesale space from data center developers, who specialize in deploying new capacity quickly.

"We are expediting the addition of significant new capacity that will be available in the weeks ahead," Microsoft said.

Microsoft is not alone in accelerating plans to add data center capacity. Amazon Web Services, the largest cloud computing provider, has applied for fast track planning permission to build three more data centers in Northern Virginia, the focal point for its global cloud.

But the COVID-19 Coronavirus pandemic has created challenges for data center construction. Facebook has halted construction at many of its data center campuses following reports that workers at its Clonee, Ireland site were being tested for Coronavirus.

From Micron's (MU) recent earnings call:

In China, lower consumer demand was offset by stronger data center demand due to increased gaming, e-commerce, and remote-work activity.

Looking to the third quarter, as these trends also take shape worldwide, data center demand in all regions looks strong and is leading to supply shortages. In addition, we are seeing a recent increase in demand for notebooks used in the commercial and educational segments to support work-from-home and virtual learning initiatives occurring in many parts of the world.

Reports of opposite, though:

Risks

Not all may be too rosy. The world is getting in a recession, and this may offset partly, fully, or more than fully the increase in demand due to the work from home measures businesses are taking.

Moreover, supply chains have also been disrupted, which may hinder Intel's ability to capitalize on any increased PC demand:

"PC makers may also struggle to make the most of the short-term spike in orders as they grapple with supply chain disruptions."

In an 8-K filing, it warns that the COVID-19 outbreak could "materially adversely affect our financial condition and results of operations."

Revenue outlook

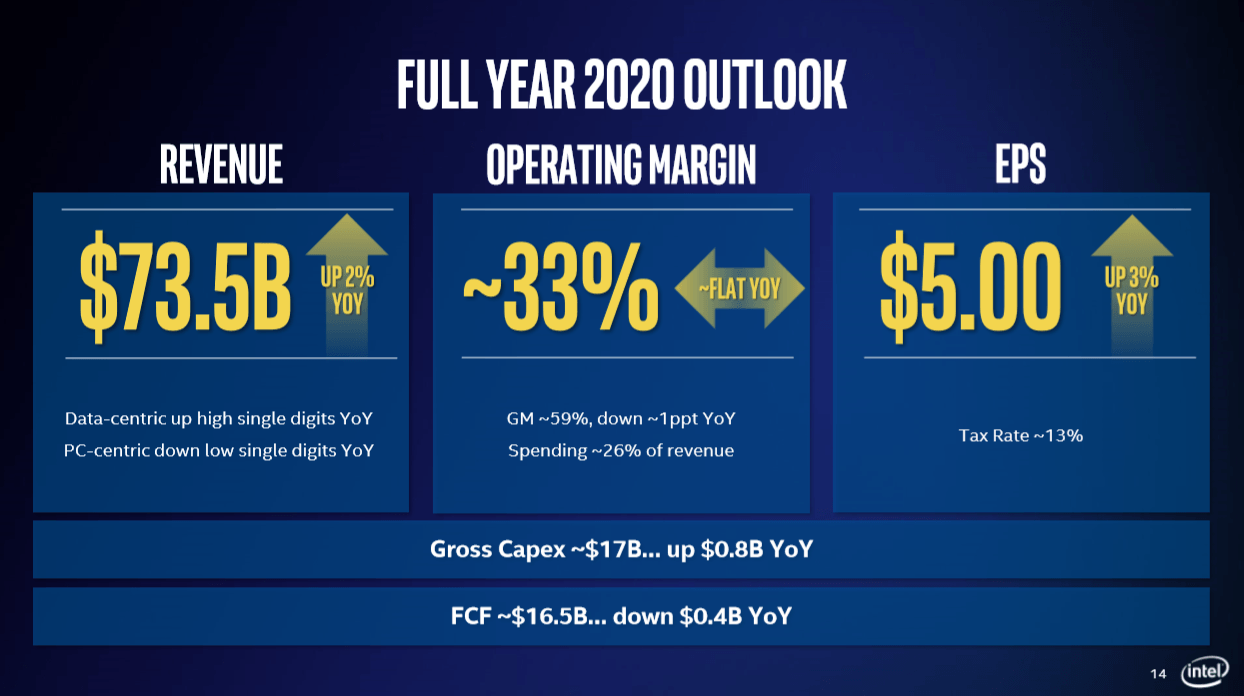

At last year's investor meeting, Intel guided to $76 to $78 billion in revenue in 2021 as part of a new three-year plan.

The company is already 2 billion ahead of this plan due to the higher-than-expected resurgence in cloud data center spending in the second half of last year: two large quarterly beats provided Intel with $72 billion in revenue vs. $69.5 billion expected.

Intel expects $73.5 billion in revenue this year, but this seems quite conservative - Intel in fact admitted it was being conservative in predicting cloud spending this year, and hoped to be wrong about that.

The above data points from Amazon (AMZN) and Microsoft (MSFT) only add to the bull thesis. Given this described coronavirus factor that is likely favoring PC and data center demand, Intel should therefore be able to beat those estimates comfortably, possibly on condition that the economy does not decline too much too long.

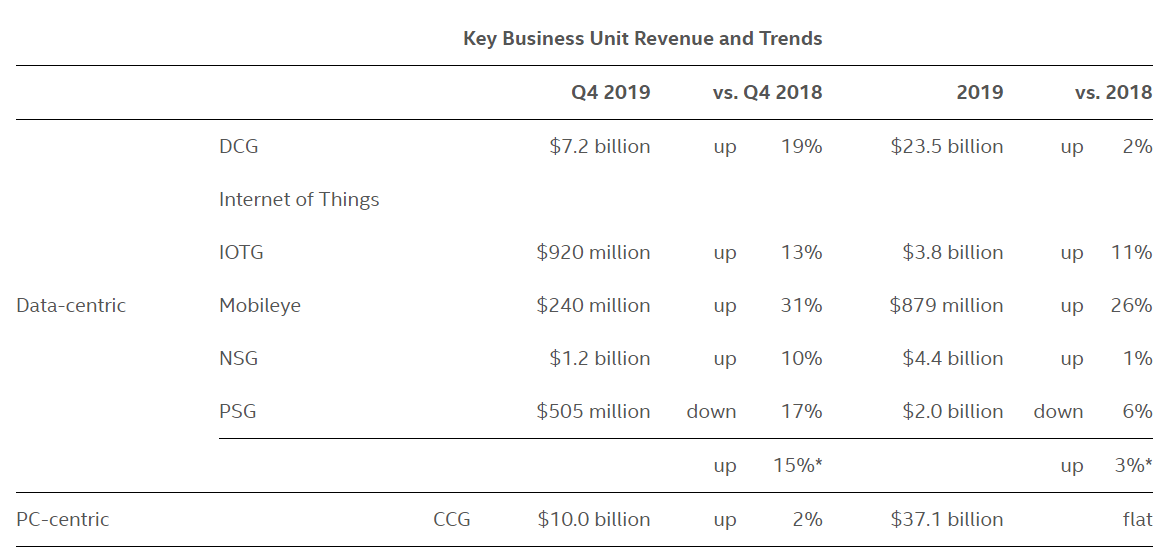

To recap, 2019 results:

I currently expect Intel to reach its 2021 target this year already and achieve over $76 billion in revenue (estimates):

- PCG: 36.0 (vs. 37.1 in 2019)

- DGC: 27.3-28.3 (vs. 23.5)

- NSG: 5.4

- IoTG: 4.3

- PSG: 2.0

- MOB: 1.2

After a flat data center year in 2019, I am expecting double-digit growth for the data center in 2020. The PC will see a decline from Intel's modem exit, but should be offset by increased demand as outlined in this article; my $36.0 and $27.3 billion number was a rough estimate before reports of increased PC demand, which basically assumed a ~$1.0 billion modem hit and a flat PC market. I further expect secular (double-digit) revenue increases from Intel's other groups. IoT may be a bit more of wildcard than usual.

Suspending buybacks, 5G iPhone delay

Intel, like other companies, has announced it is suspending buybacks. The company had announced in Q3 it would buy $20 billion worth of shares over the next 15-18 months. Less than half a year into this, the company reported it had spent $7.6 billion on buybacks already.

It has also been reported that Apple (AAPL) might delay its 5G iPhones, with a decision yet to be made. This could provide a further $1 billion tailwind for the PC Group this year (offset partially by lower demand), as the modem revenue decline would be delayed.

Takeaway

Intel's shortages have just barely been solved, and the next (although much broader) challenge is arising.

The coronavirus is resulting in major (at least temporary) changes in society. To stay connected during this period given work-from-home and other policies, people need PCs, and PCs need data centers. This benefits Intel.

Summing up the tailwinds:

- Increased PC demand due to work-from-home, social distancing, etc.

- Increased data center demand, too (which includes 3D NAND)

- 4G modem demand due to possible 5G iPhones delay

On the other hand, the economic recession this seems to be causing may (or may not) prove to outweigh PC and data center demand - but even then, likely to a lesser extent for Intel, similar to other companies such as Zoom (ZM) and Slack (WORK).

However, given some of the reports I have cited, I think the net impact will be firmly positive, and expect an increase in data center revenue by several billion dollars. I expect Intel to reach its 2021 target this year.

Like many companies, Intel likely experiences much uncertainty, but might have some more clarity by the time of its earnings call. Given Intel's conservative January guidance and the sell-off, I do not expect much financial or stock downside.