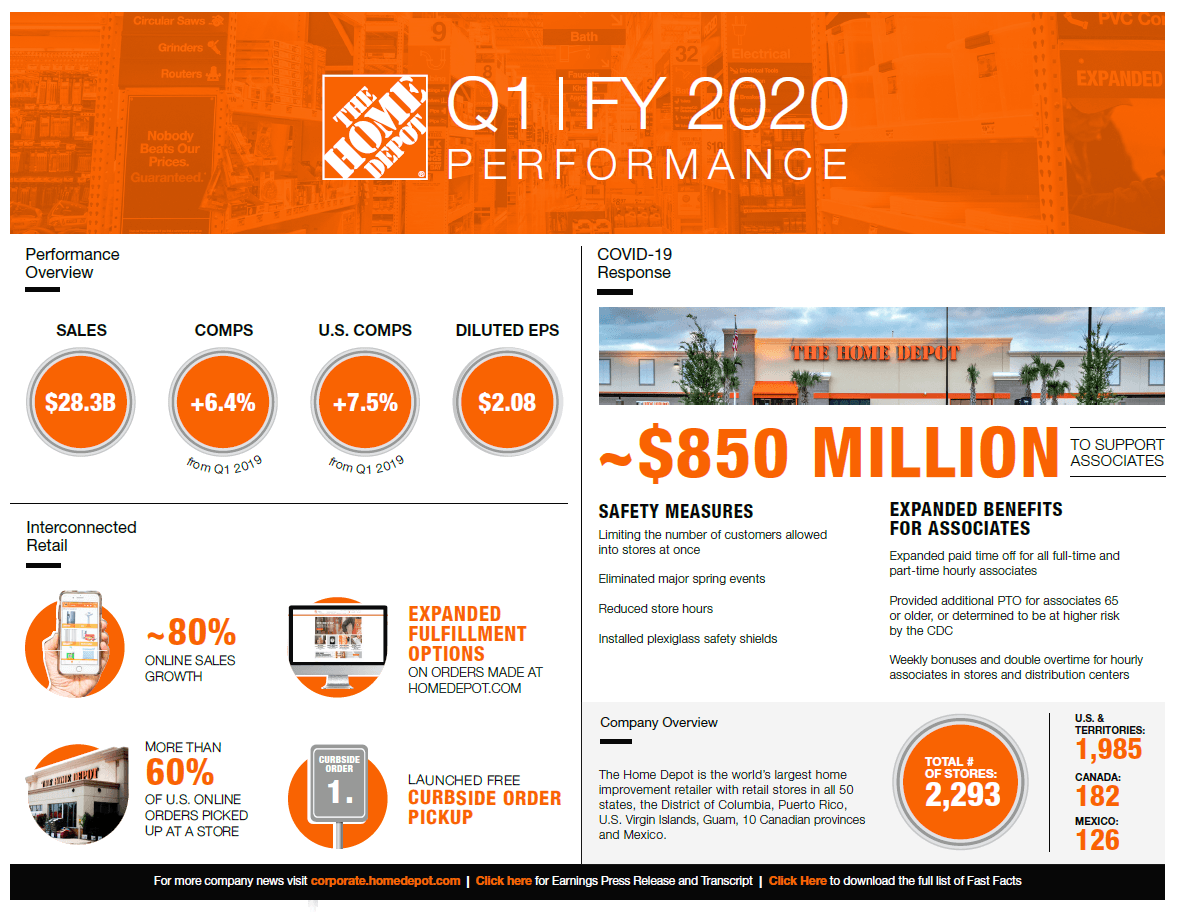

Strong Sales, Higher Costs

The Home Depot (NYSE:HD) reported stellar sales growth in Q1 of 7.1%, above original full year guidance of 3.5% - 4.0%. This was despite several actions taken to improve safety in light of the COVID-19 pandemic, including limiting customer occupancy in stores, reducing operating hours, cancelling some installation services, and eliminating promotions like Spring Black Friday. The retailer's earlier work on the One Home Depot project to improve the digital shopping experience paid off in a big way as the pandemic limited in-store traffic. Home Depot expanded order fulfillment options for online orders including delivery from stores and adding curbside pickup. Online sales grew 80% relative to Q1 2019, with the growth increasing from 30% in early March to over 100% by the end of the quarter. On the earnings call, management commented that traffic on homedepot.com was setting records during the last 3 weeks of April, with views consistently above Black Friday levels.

Home Depot took good care of its employees, compensating them for working in the hazardous pandemic-related environment. The company granted additional paid time off to all hourly workers with even more paid time off for those over 65 or at-risk according to CDC guidelines. The company also paid weekly bonuses and double overtime, and extended dependent care benefits and waived related co-pays. This added up to $850 million of incremental cost in Q1.

Source: Home Depot Q1 2020 Earnings Infographic

Source: Home Depot Q1 2020 Earnings Infographic

On the financing side, the company made moves to ensure liquidity during Q1. They suspended share buybacks after completing about $600 million worth of purchases. The company also increased its commercial paper program and revolving credit facility but did not issue any commercial paper or draw on the revolver during the quarter. Home Depot issued $5 billion of long term debt in the quarter with an average interest rate around 3%. After maturity of about $1 billion of debt in the quarter, net issuance was around $4 billion.

The company withdrew guidance for 2020 due to the uncertain environment. Initial signs are positive, with management noting comp sales now up double digits for the last three weeks of April and first two weeks of Q2. Still, it is difficult to predict if this growth will be sustainable or if some of it is being pulled forward from future quarters. I will show in the models below that sustaining growth for the full year at 7% can result in the company exceeding the original EPS guidance, even with the added employee compensation and interest expense. If the growth tails off in the second half to the original plan of 3.5-4%, or if sales were only pulled forward so that the full year averaged 3.5-4%, EPS will come in below the original guidance.

Home Depot shares traded around $245 prior to the earnings release, near the pre-pandemic high of $247. I noted in my February article, "Home Depot- Safe But Expensive" that the stock was fairly valued based on original 2020 guidance. Considering the extra employee and interest costs as a result of the pandemic, the retailer will need to repeat the excellent Q1 sales growth every quarter this year to deliver the original EPS guidance of $10.45/share. Since this seems like a best-case scenario rather than most probable, I am leaving my rating for Home Depot at Neutral.

Can The Strong Sales Continue?

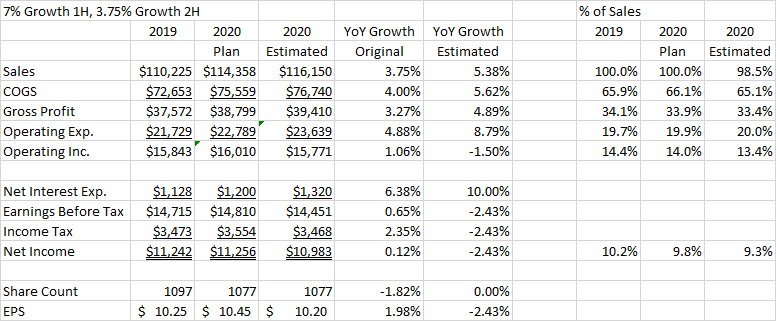

In the cases below, I add a column to the model that I used in my February article that showed 2019 actuals and the original guidance for 2020. The new column shows EPS under different sales growth scenarios. In all cases, I assume operating expenses increase by $850 million for the full year. Although the company spent $850 million in just Q1, CEO Craig Menear mentioned on the earnings call that about $700 million of this was for paid time off for the rest of the year and was accrued in Q1. The remaining $150 million for weekly bonuses and overtime was for Q1 only, so this expense will continue through May and June. Offsetting this, management noted that other operating costs were lower outside of the pandemic-related employee compensation. Given that offset I will assume the cost increase for the year will stay at $850 million. On the interest expense line, I also added $120 million for 3% interest on the incremental $4 billion of debt incurred in Q1. Assumed tax rate is unchanged at 24%.

For the optimistic sales case, I assume sales growth for the full year increases by 7% over 2019. The company normally assumes flat sales at best during a recession, although this pandemic-induced downturn has some unique drivers. For this case to materialize, we would likely need consumers to shift a portion of their spending toward home improvement from other discretionary activities as a result of the pandemic. Another driver could be market share growth if Home Depot takes share from smaller hardware stores that do not make it through the downturn.

Data Source: Home Depot 4Q 2019 Earnings Release and author estimates

Data Source: Home Depot 4Q 2019 Earnings Release and author estimates

In this case, sales growth is enough to more than offset the cost increases, and 2020 EPS is predicted at $10.63, about 1.7% over the original guidance midpoint.

In the second case, I assume the 7% sales growth lasts for the first half of the year only, then slows to the original plan growth rate of 3.75% at the midpoint. In this scenario, the EPS forecast falls to $10.20, which is 2.4% below the original guidance.

In the third case, I assume 2H sales were pulled forward into 1H and the average growth rate for the year ends up at the original guidance of 3.75%. The added operating costs and interest expense would still exist though. In this case, 2020 EPS would fall to $9.77, or 6.5% below the original guidance.

Of these cases, only the most optimistic one suggests improved earnings over Home Depot's original guidance for 2020. As the company focuses on maintaining extra liquidity during this uncertain period, I would also not count on share buybacks to boost EPS this year. With the stock only about $2 below the all-time high headed into the earnings release, it was not surprising to see a 3% selloff on the day of the report. I considered the shares fairly valued ahead of the pandemic in February, and Q1 results have not provided any justifications to upgrade my view. The stock is still a hold. For some margin of safety, I would use a buy target of $195, or 20 times my low-end 2020 EPS estimate of $9.77. The 20 multiple is in line with the forward P/E of main competitor Lowe's (LOW) prior to its Q1 earnings release.

Of these cases, only the most optimistic one suggests improved earnings over Home Depot's original guidance for 2020. As the company focuses on maintaining extra liquidity during this uncertain period, I would also not count on share buybacks to boost EPS this year. With the stock only about $2 below the all-time high headed into the earnings release, it was not surprising to see a 3% selloff on the day of the report. I considered the shares fairly valued ahead of the pandemic in February, and Q1 results have not provided any justifications to upgrade my view. The stock is still a hold. For some margin of safety, I would use a buy target of $195, or 20 times my low-end 2020 EPS estimate of $9.77. The 20 multiple is in line with the forward P/E of main competitor Lowe's (LOW) prior to its Q1 earnings release.

The Dividend Is Still Safe

In my February article, I noted that in the last recession driven by a housing market collapse, free cash flow declined 40% from top to bottom of cycle. I also showed that a 40% decline from 2019's free cash flow would still cover the planned $1.50/share quarterly dividend if buybacks were stopped and capex dialed back to normal levels. As we have seen from Q1 results, this downturn is very unlike the housing crash with Home Depot's business actually improving. Free cash flow in Q1 was $5.15 billion and dividends were $1.61 billion for a FCF payout ratio of only 31%. Even ignoring free cash flow, the $8.7 billion of cash on the balance sheet is enough to pay off the $4.2 billion of debt coming due this year and have almost enough cash left over to cover the 3 remaining dividend payments.

Conclusion

Home Depot's efforts to improve the online sales channel really paid off during the pandemic as the retailer was able to meet surprisingly high demand even with safety restrictions on its physical stores. The company has also been a great employer, compensating its employees generously for their work during risky conditions. These added costs, along with higher interest expense, could result in below-plan earnings if sales growth goes back down to plan levels. Conditions are still too uncertain for the company to provide sales and earnings outlooks for 2020, so it would be highly optimistic to assume the strong 7% growth of Q1 can continue for the full year.

Home Depot share price recently got within $2 of the all-time high reached in February ahead of the pandemic-induced crash. Since I considered the shares fairly valued in February, they are still a hold at this time. HD is the third-largest holding in my portfolio, so I would not add here. Long-term holders need not worry about selling as the dividend is still well-covered by free cash flow. The shares would be more attractive to add at 20 times my low end EPS estimate for a margin of safety or $195.