Introduction: $2bn in "Beyond Nicotine" Deals

Philip Morris (NYSE:PM) announced this morning (July 9) that it has agreed to acquire Vectura (VEGPF), a U.K. provider of inhaled drug delivery solutions, for £852m ($1.2bn) in cash. The offer represents a price of 150p per share, 10% higher than a previous offer of 136p from private equity firm Carlyle. The Vectura Board has agreed to recommend Philip Morris' offer, though a counterbid from Carlyle is still possible.

The acquisition followed a similar agreement last week (on July 1) to acquire Fertin Pharma, a Danish provider of oral delivery systems for active ingredients, for $820m in cash. The seller was EQT, a private equity firm, which has owned 70% of Fertin Pharma since 2016.

Together these represent more than $2bn being spent on "Beyond Nicotine" acquisitions in the past 2 weeks. While the targets are outside Philip Morris' current core competence and may have come as a surprise to some investors, we believe they make strategic sense and are positive to our investment case.

Philip Morris Buy Case Recap

We initiated our Buy rating on Philip Morris in June 2019, and have reiterated it regularly since. From our initiation, Philip Morris stock has gained 37.3% (including dividends) in 2 years, including 20.3% since the start of 2021:

| Philip Morris Share Price (Last Year)

Source: Seeking Alpha (09-Jul-21) |

We believe Philip Morris stock has one of the best risk/reward profiles in U.S. stocks, combining a strong, profitable existing cigarettes business and a high-growth, higher-margin new Reduced Risk Products business. Current management 2021-23 targets, outlined at the February investor day, include a revenue CAGR of at least 5%, an average annual EBIT margin uplift of 150 bps or more, and an EPS CAGR of at least 9% (excluding currency):

| PM Medium-Term Financial Targets

|

While the two new acquisitions are by nature less well-known to us, we believe there are a number of reasons why investors should be positive about them.

What Do Vectura and Fertin Pharma Do?

Vectura is a specialist in inhaled drug delivery solutions. It provides contract development and manufacturing services to pharmaceutical companies, including global large caps like Novartis (NVS) and Bayer (OTCPK:BAYZF), and generates revenues through a mixture of royalties, product supply and development fees. Example partners/licensees and products are below:

| Selected Vectura Partners/Licensees & Products

|

Vectura had £191m ($264m) of revenues and £61.5m ($85m) of EBITDA in 2020. 36% of its 2020 revenues were in royalties and milestone payments.

Fertin Pharma is a specialist in oral delivery systems for active ingredients, and also generated revenues by contract development and manufacturing. Its products include soluble tablets, gum, lozenge and pouch powder. Nicotine is one of the active ingredients it is involved with, and it describes itself as a "leading producer of nicotine replacement therapy solutions":

| Selected Fertin Pharma Products

Source: Fertin Pharma website. |

Fertin Pharma had approx. $160m of revenues and $55m of EBITDA in 2020.

Helps Strategic Goals and "Beyond Nicotine"

Both Vectura and Fertin Pharma possess technologies that can be developed into smoke-free nicotine delivery to complement Philip Morris' existing Reduced Risk Products in Heat Not Burn (IQOS) and E-Vapor (IQOS VEEV).

Fertin Pharma, in particular, is involved in nicotine replacement therapy solutions (primarily nicotine gum) and pouches. Philip Morris is currently the only Big 4 Tobacco company that does not have a nicotine pouch business, which is growing strongly in the U.S., led by Swedish Match's (SWMAF) ZYN. Philip Morris has been developing products that management stated at the February investor day "can be in the market towards the end of this year".

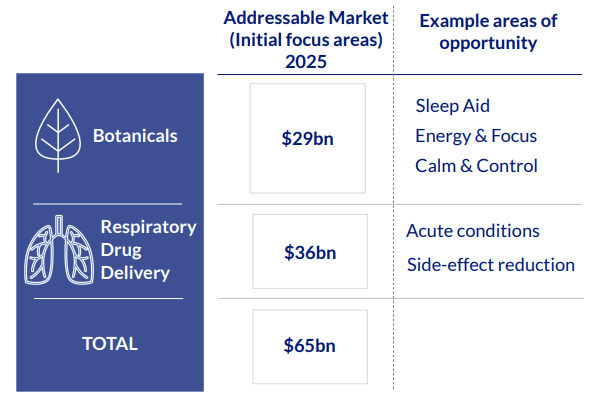

In addition, the acquisitions bring new technologies and products that can help fulfil Philip Morris' goal of generating at least $1bn of "Beyond Nicotine" revenues in 2025 (these are not included in the 2021-23 outlook). Vectura's inhaled delivery capabilities fit neatly into Respiratory Drug Delivery, one of the two initial areas of focus highlighted at the investor day:

| Philip Morris "Beyond Nicotine" Initial Areas of Focus

Source: PM investor day (Feb-21). |

At the investor day management also expressed an aspirational goal of a "natural long-term evolution into a broader lifestyle and consumer wellness company", building on the company's existing technology, manufacturing and marketing expertise:

| Philip Morris "Beyond Nicotine" Strategy

Source: PM investor day (Feb-21). |

We see the latest acquisitions as part of Philip Morris' continuing journey to develop a more broad-based and sustainable business. It has already led the sector in transforming from being just a maker of cigarettes to being also a provider of lower-risk but equally-satisfying nicotine products. Much of this success was due to management's foresight in investing $8bn+ into Reduced Risk Products since 2008, long before the returns on such investments were obvious to competitors. The latest acquisitions could prove similarly successful.

The Right Kind of Diversification

We prefer the expansion into Respiratory Drug Delivery over the expansion into cannabis pursued by other tobacco companies.

Tobacco companies' efforts in cannabis have been mixed. Altria's (MO) $1.8bn (CAD 2.4bn) acquisition of a 45% stake in Cronos (CRON) in 2019 has lost about 25% of its value. British American Tobacco (BTI) has taken a 20% stake ($177m) in Canada-listed OrganiGram (OGI) in March 2021, and is trialing of CBD E-Vapor products in Manchester, U.K. Imperial Brands' (OTCQX:IMBBY) has had a 16.9% stake in Oxford Cannabinoid since 2018, likely worth tens of millions.

We believe the Respiratory has at least as strong synergies with Philip Morris, and is also more likely to be developed into a defensible, IP-rich and profitable business. Smokeable cannabis remains a fragmented, commoditised market with low barriers to entry. With Philip Morris' global operations, including in many countries where cannabis is still illegal, a major move into cannabis will complicate relations with many governments. There is also a tail risk of significant health complications from cannabis products, as long-term clinical data is still lacking, for which Philip Morris has expressed caution in the past.

The Acquisitions Are Easily Affordable

The Vectura and Fertin Pharma acquisitions are also easily affordable for Philip Morris, and should not jeopardise its dividend and buyback plans.

Philip Morris generated $9.2bn of Free Cash Flow ("FCF") in 2020, despite the negative impact of COVID-19 on its Duty Free and Emerging Markets businesses, and its guidance implies a 2021 FCF of $10.2bn:

| PM Net Income, Cashflow & Valuation (2016-20)

NB. Canada was approx. 5% of EPS in 2018. Source: PM company filings. |

The current dividend of $4.80 per share requires approx. $7.5bn of cash annually, or 74% of 2021 guided FCF. Net Debt / EBITDA has already been reduced to 1.92x at Q1 2021 (with actual Net Debt at $25.5bn). Management was sufficiently confident in June to have announced the resumption of share buybacks after Q2 2021 results, with $5-7bn to be spent over 3 years.

Both Vectura and Fertin Pharma are profitable businesses and should add to group cashflows. Even without this contribution or further growth, Philip Morris' FCF is already expected at $10bn+ this year and can easily cover the cost of the acquisitions, the dividend and the buybacks simultaneously.

The Acquisitions Will Likely Be EPS-Accretive

Philip Morris has stated that both Vectura and Fertin Pharma will be "immaterial" to its EPS in 2021. We believe this is the result of their relatively small size (their combined EBITDA was $140m in 2020, compared to Philip Morris' $12.6bn), and how the deals will close relatively late in 2021.

Longer-term, we expect both deals to be accretive to Philip Morris' EPS (but likely too small to make a material difference in the next few years). Even without any further growth or synergies, the deals make financial sense. The acquisition prices imply multiples of 14x and 15x 2020 EBITDA respectively, meaning a higher return than Philip Morris' own average cost of debt of 4.3%.

The multiples are also roughly in line with Philip Morris' own valuation of approx. 14.5x EV / 2020 EBITDA, so should be neutral to the current Enterprise Value.

Valuation - Is Philip Morris Stock Cheap?

At $98.37, with respect to 2020, Philip Morris shares are trading at a 19.0x P/E and a 6.0% FCF Yield; with respect to the mid-point of 2021 guidance, shares are trading at a 16.4x P/E and a 6.7% FCF Yield.

Does Philip Morris Pay Dividends?

Philip Morris stock currently pays a dividend of $1.20 per quarter ($4.80 annualized), which represents a Dividend Yield of 4.9%. The dividend was raised 2.6% in September 2020 despite the ongoing disruption from COVID-19, and we expect further increases in the future.

Philip Morris Stock Forecasts

We keep our forecasts unchanged from our last update:

- 2021 EPS of $6.00, mid-point of the management outlook

- From 2022, Net Income grows at 7.0% p.a., implying an ex-currency growth of 9.5%, less 2.5% in currency impact

- Share count to fall by 1.0% in 2021, then 1.5% each year from 2022

- Dividends to be based on a 75% payout ratio

- P/E at 16.0x at 2024 year-end

With Philip Morris stock at $98.37, we expect an exit price of $123 and a total return of 45% (12.3% annualized) by 2024 year-end, in 3.5 years:

| Illustrative PM Return Forecasts

Source: Librarian Capital estimates. |

Is Philip Morris a Good Stock to Buy?

PM agreed to acquire Vectura for $1.2bn this morning; including Fertin Pharma last week, PM has spent $2bn in the last 2 weeks.

Vectura and Fertin Pharma specialize in drug delivery solutions development and manufacturing, in oral and inhaled respectively.

The acquisitions help PM's long-term strategic goals, including its "Beyond Nicotine" aspirations; they are likely to be slightly EPS-accretive.

PM's Free Cash Flow can easily afford the acquisitions, while still paying dividends and buying back shares as already planned.

At $98.37, the stock is expected to generate a total return of 45% (12.3% annualized) in 3.5 years. The Dividend Yield is 4.9%. Buy.

We reiterate our Buy rating on Philip Morris stock.

Note: A track record of my past recommendations can be found here.