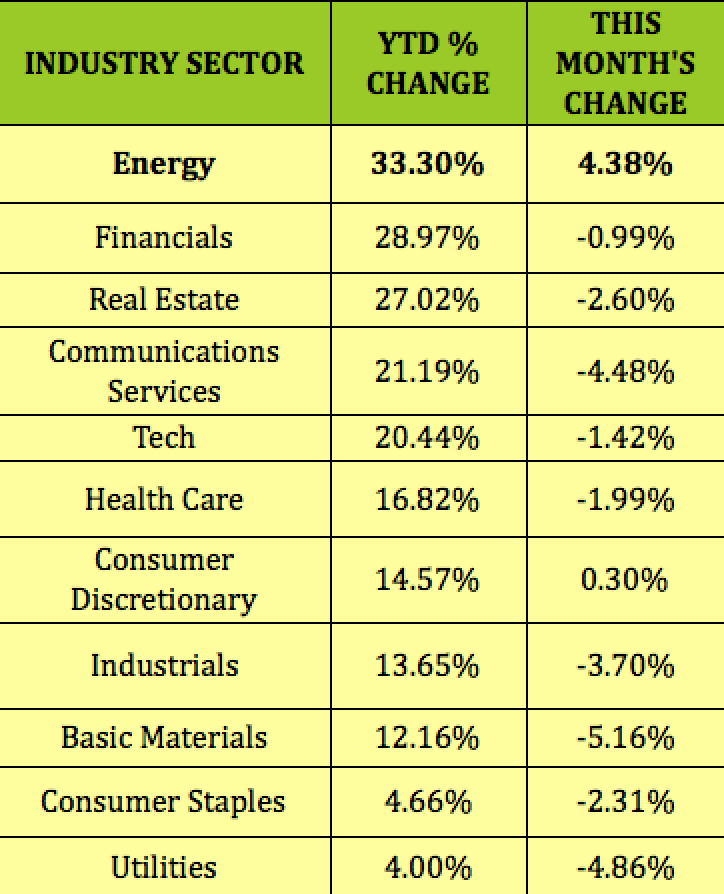

The energy sector has had a good ride so far in 2021, leading all other sectors, with a 33% gain, having gained 4.4% in September:

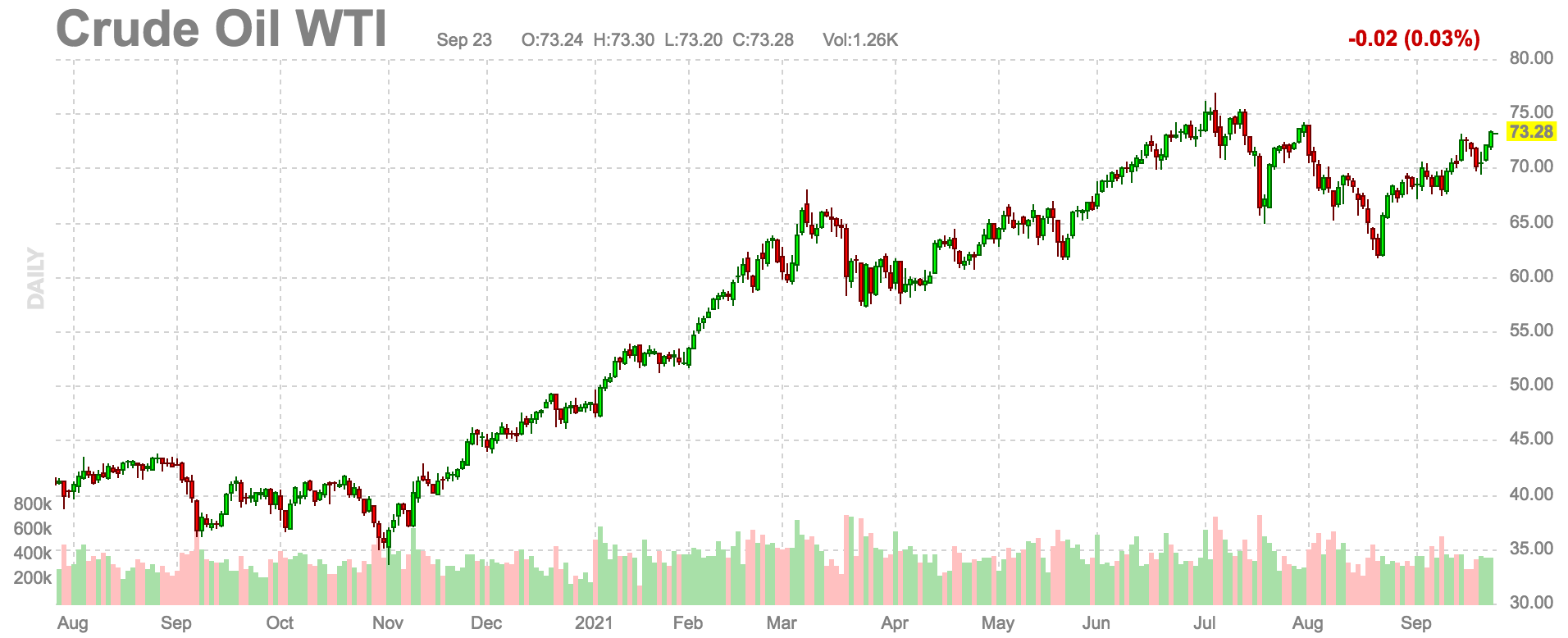

WTI Crude just hit its highest price since July this week, on dwindling supplies, after 2 Gulf hurricanes hampered production in that area. The EIA reported U.S. crude stocks in the week to Sept. 17 fell by 3.5 million barrels to 414 million - the lowest since October 2018.

WTI Crude just hit its highest price since July this week, on dwindling supplies, after 2 Gulf hurricanes hampered production in that area. The EIA reported U.S. crude stocks in the week to Sept. 17 fell by 3.5 million barrels to 414 million - the lowest since October 2018.

Demand has also risen, with East Coast refinery utilization rates in the US rising to 93%, the highest since May 2019, EIA data showed. Natural gas also has risen in 2021, more than doubling.

(finviz)

(finviz)

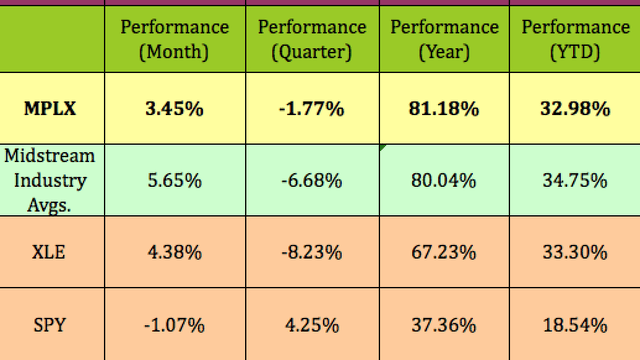

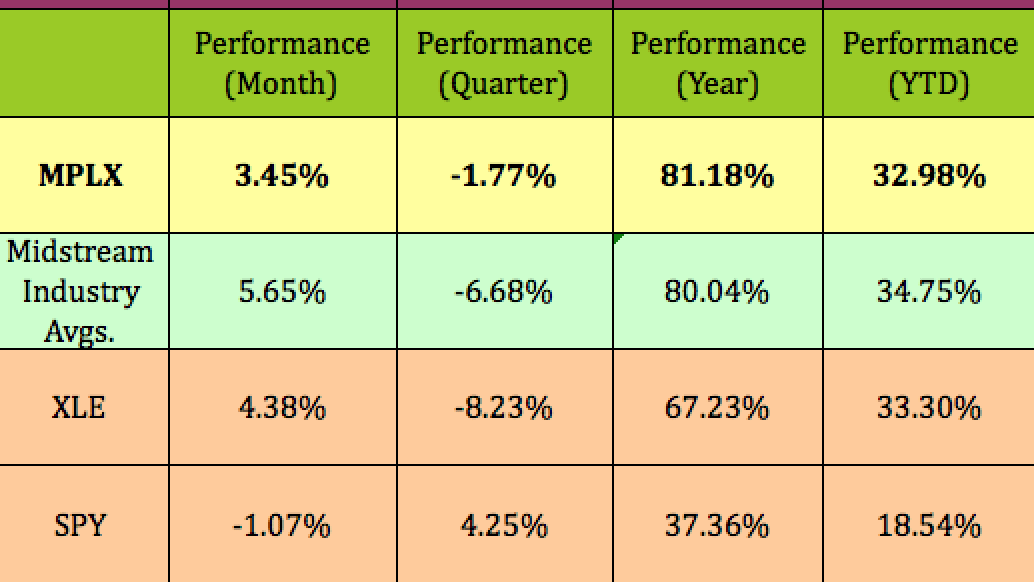

MPLX LP (NYSE:MPLX) has been a beneficiary of rising energy prices, rising 33% in 2021, and outperforming the market by a wide margin. It's also up 81% over the past year, vs. 37% for the S&P, slightly ahead of the midstream industry's 80% rise, and eclipsing the Energy sector's 67% rise.

Profile:

Profile:

MPLX LP is a diversified, growth-oriented master limited partnership formed in 2012 by MPC to own, operate, develop and acquire midstream energy infrastructure assets.

It's engaged in the gathering, processing and transportation of natural gas, the gathering, transportation, fractionation, storage and marketing of NGLs, the transportation, storage and distribution of crude oil and refined petroleum products, as well as refining logistics and fuels distribution services.

MPLX provides services in the midstream sector across the hydrocarbon value chain through its Logistics and Storage and Gathering and Processing segments. (MPLX site)

Earnings:

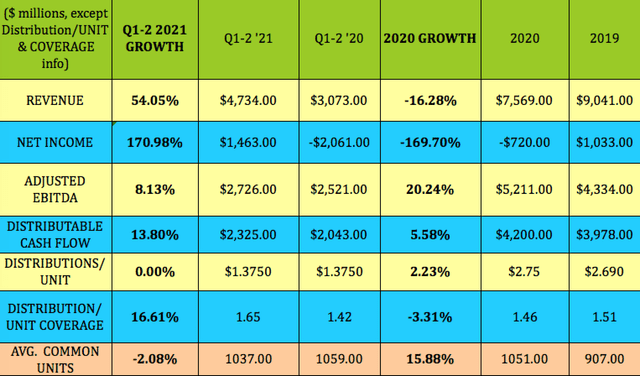

2020 was a mixed bag for MPLX with revenue down -16% and net income down -170% due to a -$3.4B non-cash impairment charge in Q1 '20. Still, EBITDA rose 20%, and DCF was up over 5%.

Q1-2 2021 has seen revenue bounce back, rising 54% vs. Q1-2 '20, while net income reversed course and rose 170%. Adjusted EBITDA was up 8%, and DCF rose an impressive 13.8%, improving distribution coverage by 16.5%, to 1.65X.

Segments:

Segments:

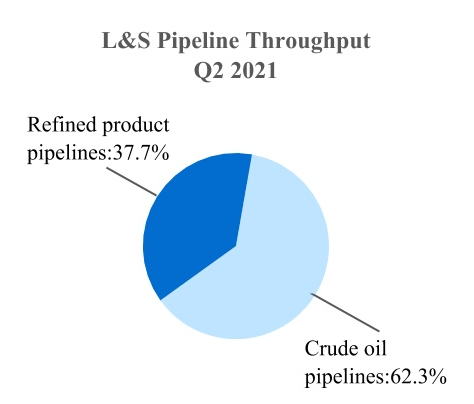

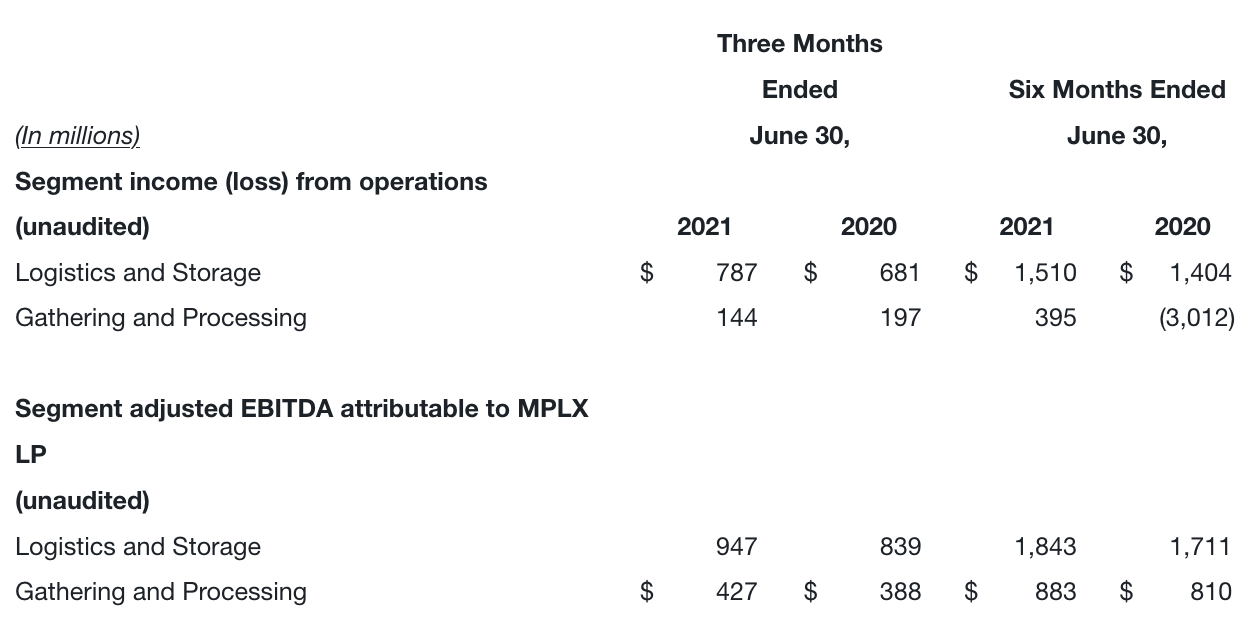

Logistics & Storage segment income from operations for Q2 2021 increased $106M vs. Q2 2020, while segment adjusted EBITDA increased by $108M.

Pipeline throughputs were 5.6 million barrels per day (bpd) in the second quarter, 29% higher than the same quarter of 2020. The average tariff rate was $0.88 per barrel for the quarter, a decrease of 6% vs. the same quarter of 2020. Terminal throughput was 3.0 million bpd for the quarter, an increase of 23% versus the same quarter of 2020.

(MPLX site)

(MPLX site)

Gathering & Processing Q2 '21 segment income decreased by $53M, primarily due to non-cash impairments related to minor changes in the portfolio. Adjusted EBITDA rose by $39M vs. Q2 '20. as a result of higher natural gas liquids prices and lower operating expenses. These benefits were partially offset by lower gathered and processed volumes. Gathered volumes averaged 5.1 billion cubic feet per day (bcf/d), an 8% decrease vs. Q2 '20. Processed volumes averaged 8.4 bcf/d, a 1% decrease, and fractionated volumes averaged 545 thousand bpd, consistent with Q2 '20.

(MPLX site)

(MPLX site)

Growth Projects:

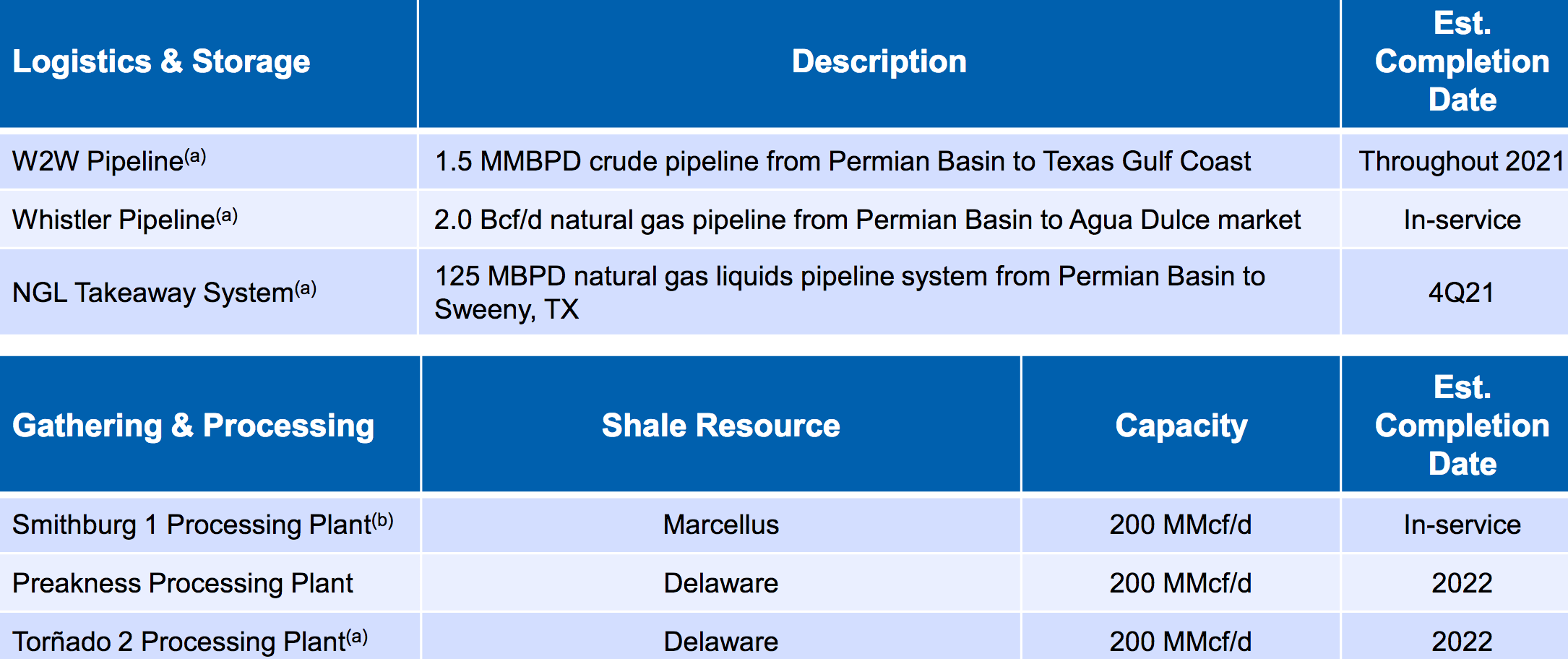

The L&S segment has three growth projects coming online in 2021. The Wink to Webster crude oil pipeline in the Permian basin is coming aboard throughout 2021.

The Whistler natgas pipeline already is in service, earlier than expected, and the NGL system is expected to start in Q4 '21. Both are backed by long-term minimum volume commitments and management expects EBITDA contributions to ramp up through 2022.

The G&P segment's Smithburg plant, in the Marcellus basin, is in service, with a 200 MMCF/day capacity. The Preakness and Tornado plants in the Delaware Basin will come online in 2022:

(MPLX site)

(MPLX site)

Profitability and Liquidity:

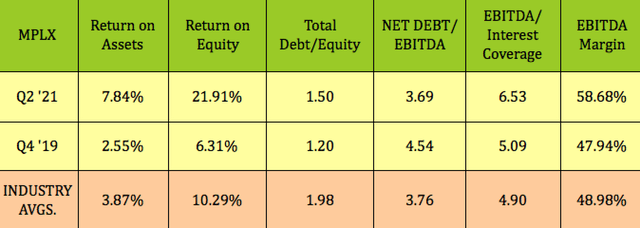

MPLX's ROA and ROE are now both much higher than its pre-pandemic figures from Q4 '19, as are its EBITDA margin and interest coverage. Net debt/EBITDA leverage has decreased to 3.69X, vs. 4.54X in Q4 '19, while debt/equity is higher, at 1.5X.

MPLX's ROA, ROE, and EBITDA margin are all higher than midstream averages. Its debt/equity is more conservative, at 1.5X vs. the industry's 1.98X average, while its EBITDA/interest coverage factor of 6.53X is much stronger than the 4.9X industry average:

Debt and Liquidity:

Debt and Liquidity:

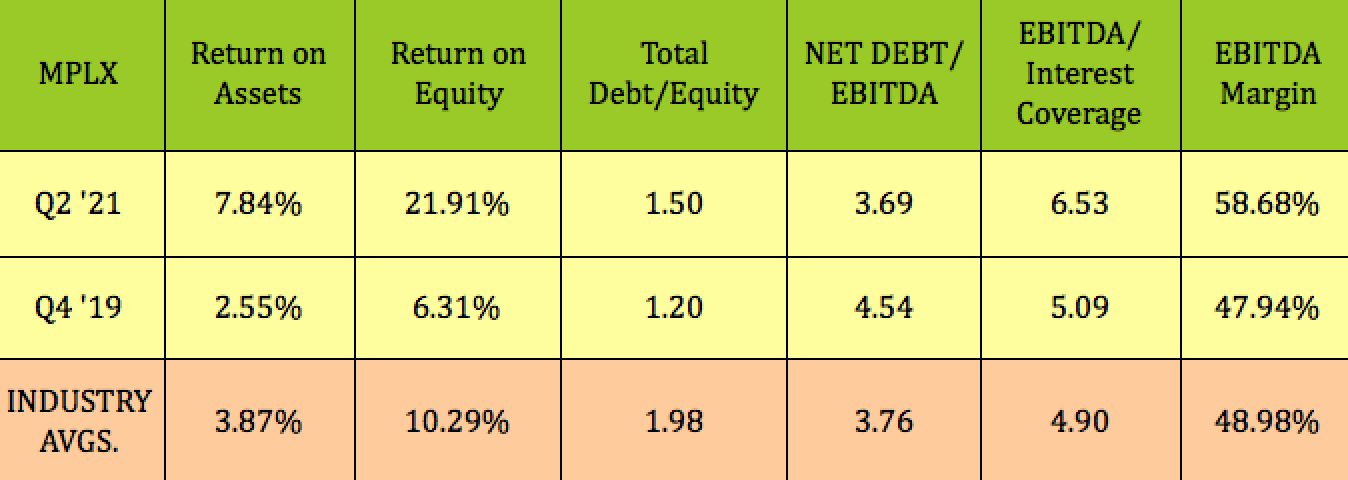

As of 6/30/21, MPLX had ~$4.5B in liquidity, with its $3.5B credit revolver untapped, and ~$1B available on its $1.5B MPC credit agreement.

(MPLX site)

(MPLX site)

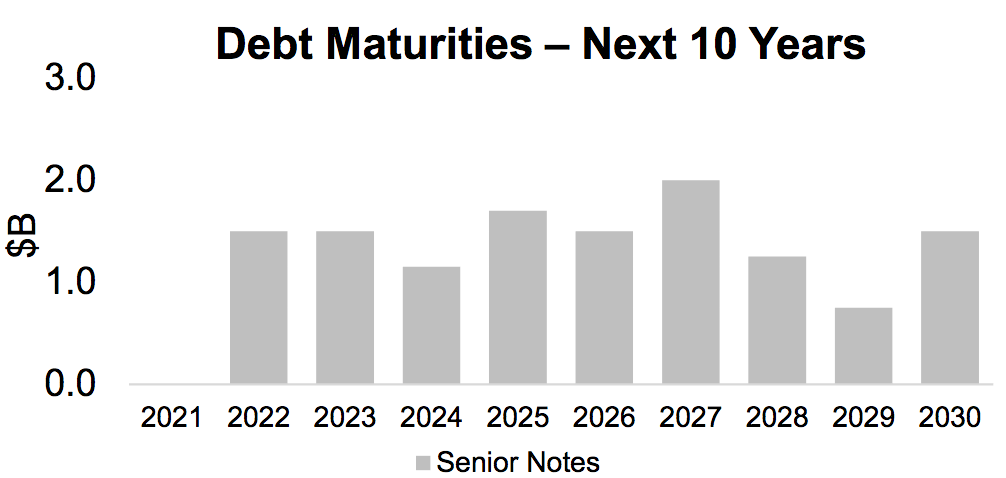

On Aug. 4, 2021, MPLX announced the intent to provide notice of the redemption of all of the $1B outstanding aggregate principal amount of MPLX's LIBOR plus 1.1% per annum floating rate senior notes due Sept. 9, 2022, which clears up the majority of its 2022 debt maturities:

(MPLX site)

(MPLX site)

MPLX's debt is rated investment grade by these three rating agencies:

(MPLX Q2 '21 10Q)

(MPLX Q2 '21 10Q)

Valuations:

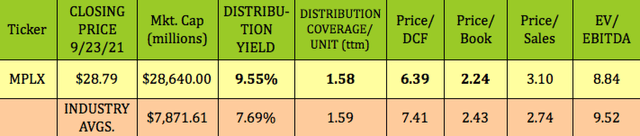

MPLX looks most undervalued vs. industry averages on a price/DCF basis, at 6.39X vs. the 7.41X average. Its P/book is roughly in line with the industry average, while its 8.84X EV/EBITDA is lower than average.

Meanwhile, the market is demanding a higher 9.55% yield from MPLX, vs. the 7.69% industry average, with trailing coverage in line.

Distributions:

Distributions:

At its 9/23/21 $28.79 closing price, MPLX yielded 9.55%. After putting together a long string of quarterly dividend increases, management has kept the quarterly payout at $.6875 since Q1 '20.

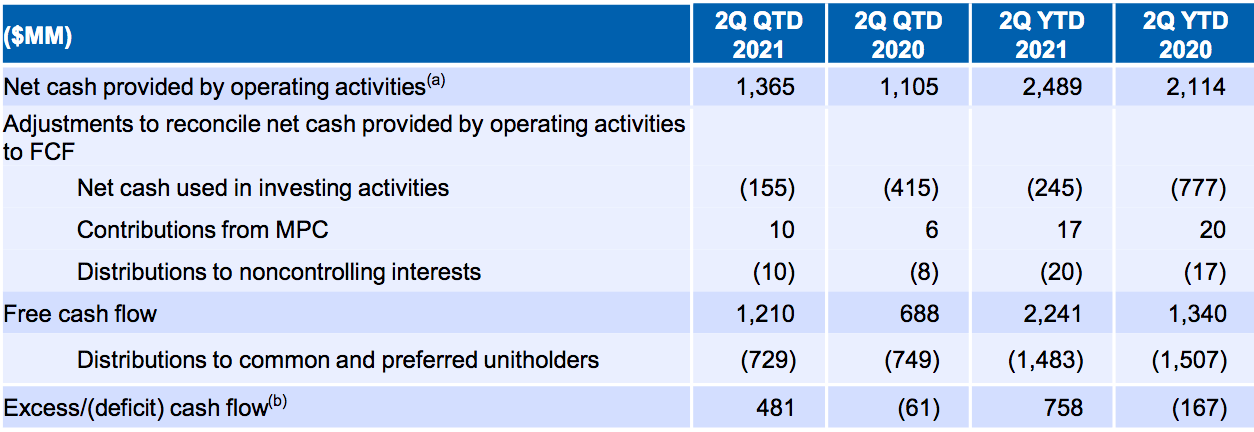

DCF/distribution coverage rose to 1.73X in Q2 '21, vs. 1.56X in Q1 '21. On a free cash flow basis, distribution coverage was 1.66X in Q2 '21, vs. just .92X in Q2 '20. Q1-2 '21 free cash flow distribution coverage was 1.51X.

DCF/distribution coverage rose to 1.73X in Q2 '21, vs. 1.56X in Q1 '21. On a free cash flow basis, distribution coverage was 1.66X in Q2 '21, vs. just .92X in Q2 '20. Q1-2 '21 free cash flow distribution coverage was 1.51X.

(MPLX site)

(MPLX site)

Taxes: MPLX issues a K-1 at tax time.

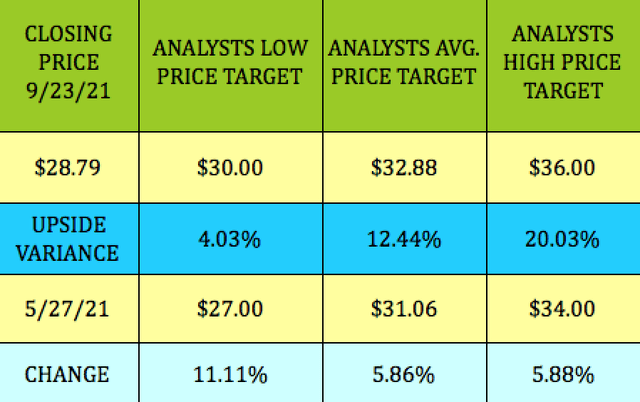

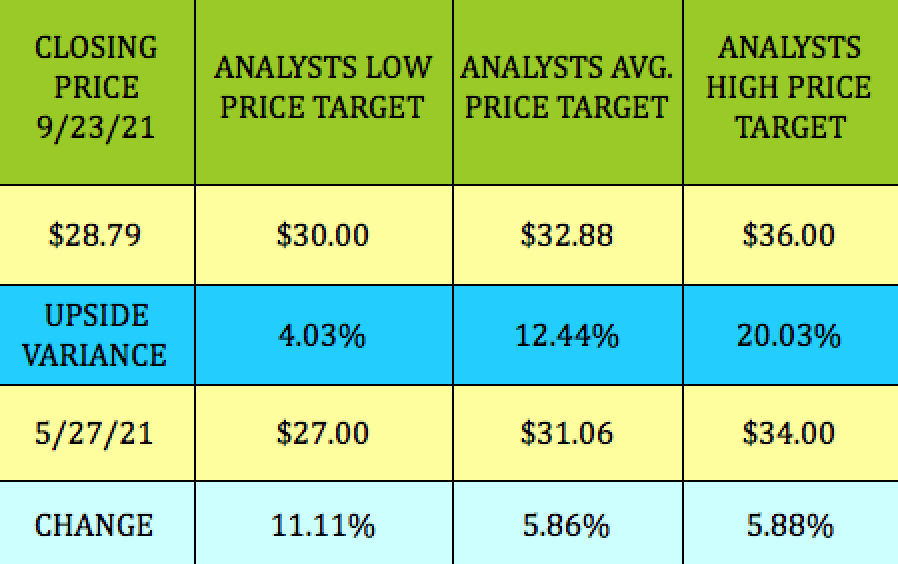

Analysts' Price Targets:

Analysts' price targets for MPLX have risen across the board since late May, with the low price target up by 11%, and the average and high targets up by nearly 6%.

At $28.79, MPLX is 12.4% below the $32.88 average price target.

Options:

Options:

Like many of the other stocks we cover in our articles, MPLX has attractive options-selling premiums .We updated the following two trades to our Covered Calls Table and our Cash Secured Puts Table, where you can see more details.

Covered Calls -If you're looking to embellish MPLX's yield, or to hedge your position, this strategy can help.

MPLX's January 2022 $30 call option pays $.75, slightly higher than its $.6875 quarterly payout, allowing you to more than double your dividend.

Conversely, if you want to achieve a lower breakeven, and get paid to wait, selling cash secured puts below a stock's price/share can accomplish that.

Conversely, if you want to achieve a lower breakeven, and get paid to wait, selling cash secured puts below a stock's price/share can accomplish that.

MPLX's January $28.00 put option pays $1.40, a 5% yield in ~4 months or 15.34% annualized. Your breakeven is $26.60, which is 11.3% below the $30.00 lowest price target:

NOTE: Put sellers don't receive dividends, we include them in our tables so that viewers can compare them to the options premiums. We use annualized yields in our options tables, so users can compare trades of varying lengths.

NOTE: Put sellers don't receive dividends, we include them in our tables so that viewers can compare them to the options premiums. We use annualized yields in our options tables, so users can compare trades of varying lengths.

All tables furnished by DoubleDividendStocks.com, unless otherwise noted.

Our Marketplace service, Hidden Dividend Stocks Plus, focuses on undercovered, undervalued income vehicles, and special high yield situations.

There's currently a 20% discount, and a 2-Week Free Trial on offer.

We publish exclusive articles each week with investing ideas for the HDS+ site that you won't see anywhere else.

We offer a range of income vehicles, with yields ranging from 5% to over 10%, and one outlier yielding 15%-plus.