Stefonlinton/iStock Editorial via Getty Images

In this extraordinary environment with portfolio rotations, inflationary pressure, an economic slowdown, a war, and an energy crisis, it is very hard to cherry-pick the right stock. Last time, we provided a deep-dive analysis on Air Liquide S.A. (OTCPK:AIQUF, OTCPK:AIQUY). As a brief recap, we were very positive for the following reasons:

- Favourable and supportive environment towards hydrogen opportunities;

- Our internal team was forecasting a strong volume recovery;

- We saw the REPowerEU plan as a positive catalyst over the long term;

- Having analysed the EV segment, we understand that EVs are almost 50% more gas-intensive than ICE, providing a long-term upside for Air Liquide;

- Strong pricing power will lead to margin recovery from the ongoing cost inflation pressure;

- A strong and solid balance sheet with potential room for further local acquisitions;

- Air Liquide's strength in realising new projects with significant headroom whilst simultaneously increasing shareholder remuneration thanks to DPS increases over time.

Q1 Results & recent project development

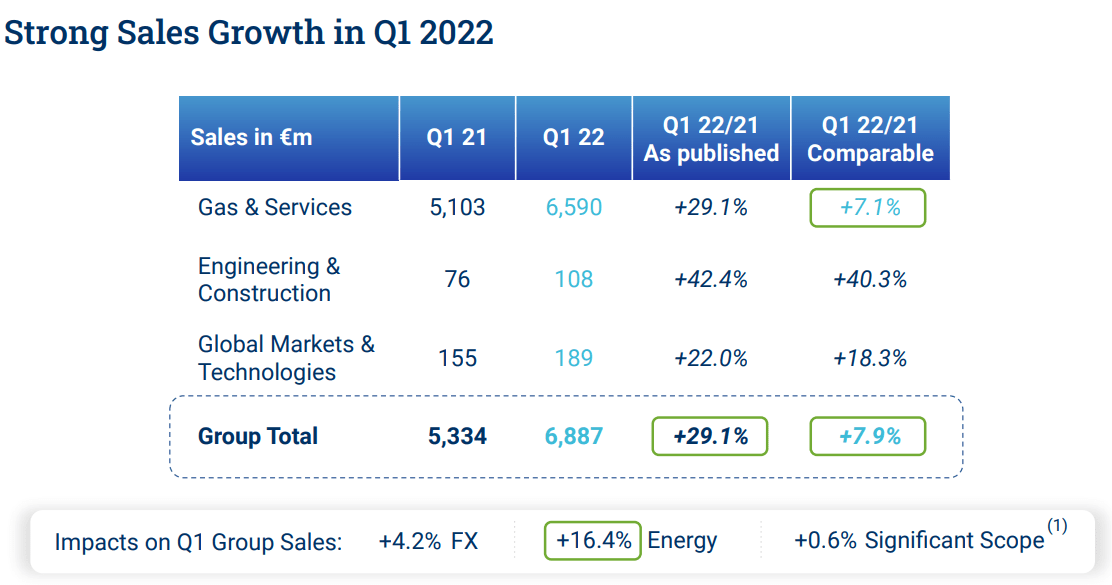

Over the first three months of the year, the chemical manufacturer's turnover amounted to €6.89 billion, up over one year by 29.1% in the published data and a plus 7.9% on a like-for-like basis. This increase reflects "in particular the significant rise in energy prices contractually passed on to Large Industries customers" indicated the company's CEO. This revenue figure is slightly higher than consensus estimates.

The energy price surge was fully passed on via contract and without any time lag to large industry customers (refining, chemicals, steel and cement) which represent more than a quarter of the company's sales.

From the results presentation, we understood that Air Liquide's exposure to Russia represented 1% of total sales and exposure in Ukraine was almost zero.

Air Liquide Q1 Revenue (Air Liquide Q1 Results)

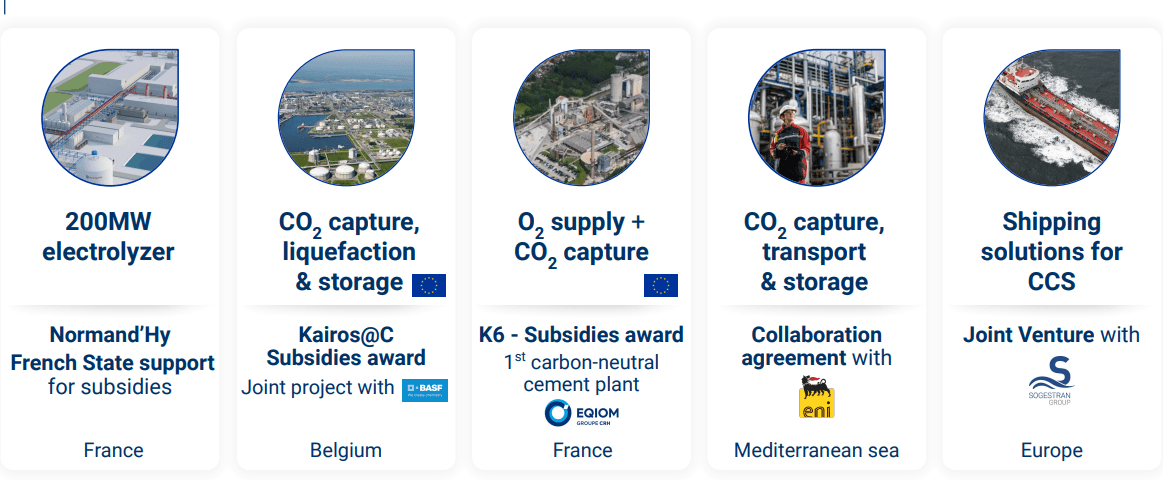

The group recently launched its new advance strategic plan for 2025, combining financial performance objectives with a major industrial decarbonisation project. To achieve this, it has signed a memorandum of understanding with the Italian energy conglomerate Eni (E) to decarbonise the most CO2-emitting industries in the Mediterranean basin and it has embarked on a cross-border carbon capture project with BASF (OTCQX:BASFY, OTCQX:BFFAF) around the port of Antwerp.

The group has also made a commitment with the building materials group EQIOM (formerly known as Holcim France) to make its cement plant in Lumbres in Pas-de-Calais one of the first in Europe to become carbon neutral.

Air Liquide New projects (Air Liquide Q1 Results)

Valuation & Conclusion

In 2022, "assuming no significant economic disruption, Air Liquide is confident in its ability to further increase its operating margin and to deliver recurring net profit growth, at constant exchange rates" reiterated group CEO Benoît Potier. After the Q1 results, our internal team reiterates the buy rating we previously gave with a price target at 190 euros per share that is based on the average between:

- A sum of the parts valuation with our 12-month forward estimates

- A DCF analysis in which we assume a WACC of 6% and a terminal growth rate of 2.5%.

We believe that Air Liquide's capital discipline and earnings power will sustain the stock price appreciation. Again, we find it difficult to understand the reason why the industrial gas specialist is trading at a discount compared to its US competitor Air Products and Chemicals (APD), with a P/E ratio and EV/EBITDA almost 20% lower, despite having achieved these past results.

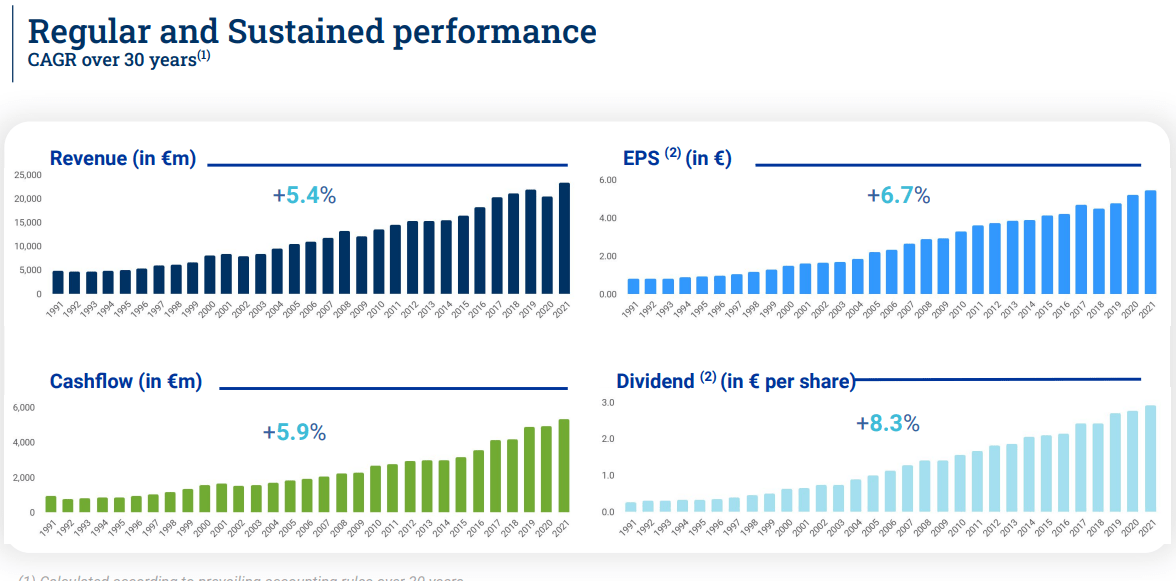

Air Liquide Past Performance (Air Liquide Q1 Results)