BalkansCat/iStock Editorial via Getty Images

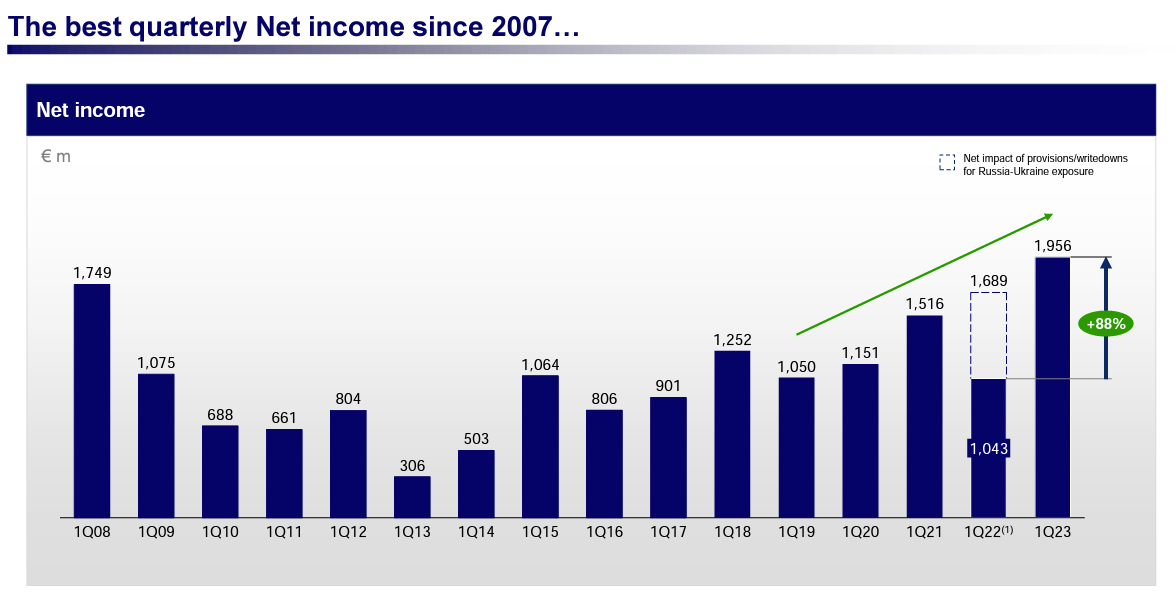

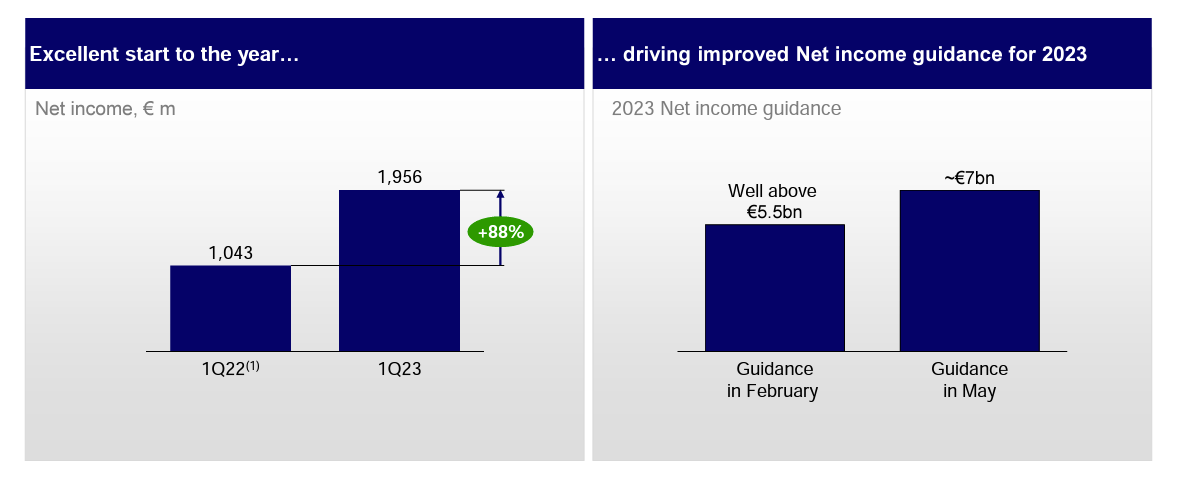

Intesa Sanpaolo (OTCPK:ISNPY) beats market forecasts with Q1 numbers which closed with a clean net profit of €1.96 billion, up from €1.04 billion recorded a year ago. This was supported by a strong boost in the interest margin development and lower loan losses. The cash payout was already set at 70% of the bank's consolidated net profit and the CEO is already open to "possible further capital distribution" on the back of these outstanding results (this was the best quarterly profit since 2007 - Fig 1). On the stock exchange, ISP is up by almost 3% and we are not surprised. As a reminder, in the Seeking Alpha community, we were the first one to buy-rated ISP, and since then (June 2022), the company's share price is up by almost 50%. With the banking turmoil, we recently published an analysis called "We Should Take Advantage" which again was a good entry point.

Intesa Sanpaolo Q1 net income

Source: Intesa Sanpaolo Q1 results presentation - Fig 1

Mare Evidence Lab's previous publication

Q1 update

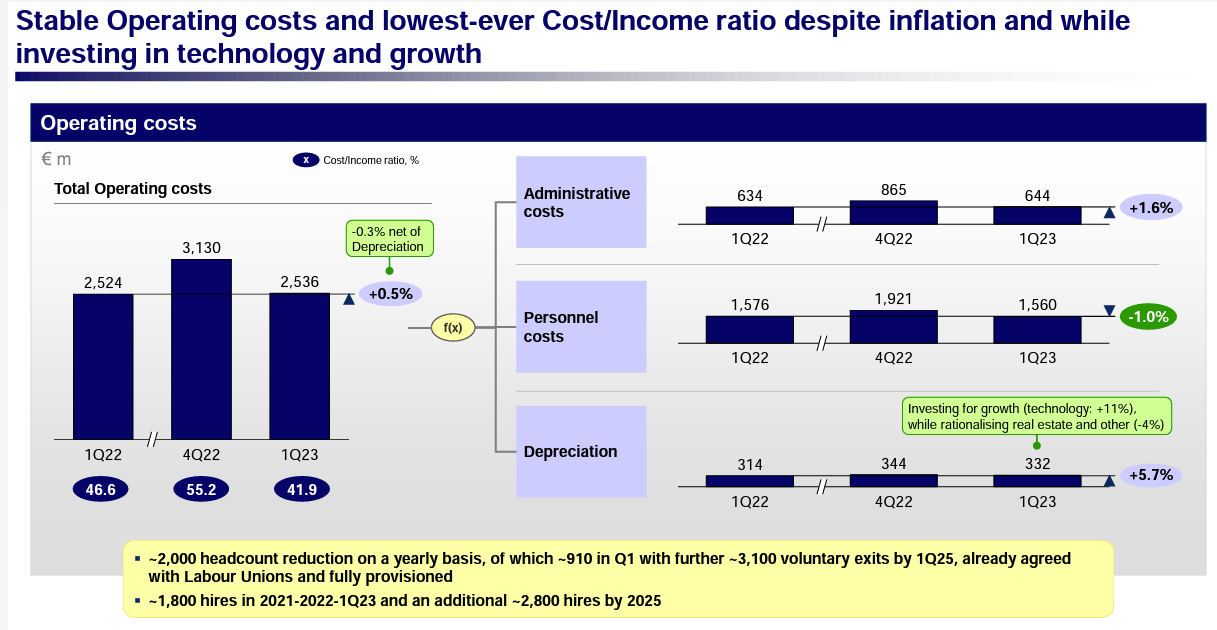

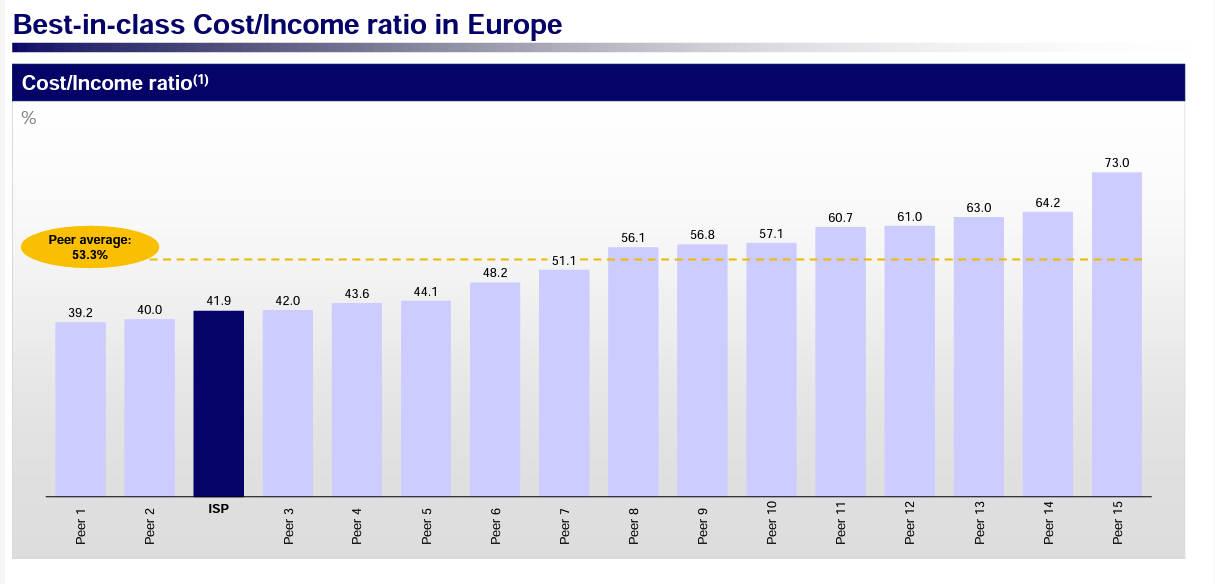

"The results for Q1 2023 confirm that Intesa Sanpaolo can generate sustainable profitability in a complex context thanks to its well-diversified and resilient business model". These were the first CEO's words and this is music to our ears and is very much in line with our investment thesis released almost one year ago. Analyzing the Q1 number, Intesa's operating income increased by 11.9% to €6.1 billion, with an interest margin evolution of +66% to €3.3 billion and net fee & commission income at €2.1 billion. As already anticipated, operating costs were substantially stable and signed a plus 0.5% at €2.5 billion (Fig 2). However, the company (once again) confirmed a solid cost/income ratio now down to 41.9%. As reported by the bank, Intesa continues to be a leading bank on a cost basis (Fig 3). With the recent banking turmoil, it is important to report that ISP delivered a solid LCR ratio, well above the regulatory requirements set at 125%. This is due to the large ISP's B2B clientele base as well as its B2C SME focus.

ISP operating cost evolution

Fig 2

ISP cost/income ratio evolution

Fig 3

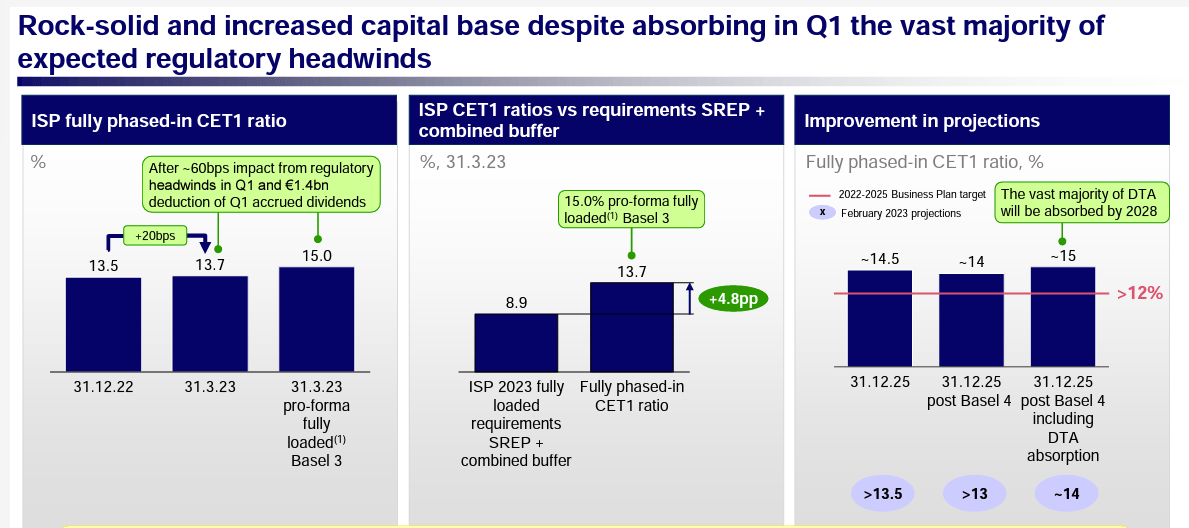

As for capital solidity and after deducting €1.4 billion in dividends accrued, the Cet 1 ratio reached 13.7%. Every quarter, the bank increased its ratio by 20 basis points, and on a fully phased target, the ratio is planned to be higher than >12%, again above the Basel 3/Basel 4 regulatory requirements. In addition, exposure to Russia was further decreased and is now down to approximately 70% versus H1 2022 with 0.2% of the group's total customer loans in the area. Furthermore, cross-border loans to Russia "are largely performing and classified in Stage 2".

Cet 1 ratio evolution

Fig 4

Conclusion and Valuation

The 2022-2025 business plan was confirmed and the related industrial initiatives are well underway, with a clear and strong upside prospect for the 2025 target of €6.5 billion in net profit. However, already in the current year, Intesa is estimating a significant increase in the margin with net interest at over €13 billion. Here at the Lab, we anticipated this positive outcome from a previous publication called 'Net Interest Income Development Is Not Priced In'. With a continuous focus on cost management initiatives and a sharp drop in net value adjustments on loans, the company has revised upwards the 2023 target for a net profit of approximately €7 billion. Last time, we said, "Intesa Sanpaolo will fully benefit from rising interest rates with an expectation of 2023 net interest margin at €12 billion against a consensus of €11 billion". Over the week, the BCE increased its rate by 25 basis points (this was already anticipated in our estimates", and ISP raised the bar with a €13 billion announcement with a potentially higher shareholder remuneration. We already increased our target price to €2.6 per share and there is support from a higher yield, therefore we decide to reiterate our buy. On the negative side, the CEO spent a few words on the project for an extra profit bank tax that the Italian Government plans to implement. This is a potential risk that we are not considering. However, having analyzed the extra profit tax on utility players, we believe it might be decremental for a maximum amount of €300/400 million (related only to ISP).

Intesa 2023 higher guidance

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.