Viacheslav Peretiatko/iStock via Getty Images

The market is being held hostage to a number of rattling ghosts that keep popping up like something out of a Charles Dickens novel. The pandemic, inflation, political turmoil in Washington, skyrocketing home prices, shipping problems, raucous tweets from Elon Musk as he's taking care of more urgent business - it's enough to make you hunt down your old copy of Stephen King's "The Stand" for something uplifting.

Speaking of Dickens, it sure seems as though the Ghosts of Christmas Past have paid 2021 a visit. The ghost of 1979, that is. Surging inflation, disasters in the Middle East, economic disarray, homes hard to buy, Georgia determining the direction of national politics, dogs and cats living together... Seems like old times.

Now, if we could just find a money market paying 12% interest like in 1979, we'd be in business!

While it gets a lot of grief, 1979 actually was a pretty good year to buy stocks. The S&P 500 was up 12.31%, and 1980 burnished those returns when it rose 25.77%. I'm probably one of the few people who have fond memories of 1979 even if the Yankees did miss the playoffs for the first time in four years.

What's different about 2021 is that back in the 1970s we didn't have some pestilence running amuck (well, if you set aside bell-bottom jeans). It has changed people's attitudes about a lot of things. When President Trump banned travel from infected Chinese cities in 2020, it was considered highly controversial and at the very least premature. Now, debating travel bans on entire world regions due to some new outbreak there is considered almost obligatory and not worthy of debate.

That change is an indication of how the world has mutated in just the last two years, and why the pandemic still has to be taken seriously when picking stocks. We may need the help of Optimus Prime before we conquer COVID-19 once and for all.

In this article, I talk about a stock I own that doesn't give me any worries even though it's been in some ways at the eye of the storm that has bedeviled the market since we first heard the ominous term "COVID-19." It keeps rewarding its shareholders almost as often as new Spiderman and Superman reboots. When you're looking for an old friend who just keeps ringing at the door until you stumble down, bleary-eyed, coffee mug in hand, to give you the latest gossip and fill you in on the latest, this is the company to consider.

Dividend Kings

| Company | Business | Years of Dividend Hikes |

| American States Water (AWR) | Utility | 67 |

| Dover Corporation (DOV) | Industrial | 66 |

| Emerson Electric (EMR) | Utility | 65 |

| Northwest Natural Holding (NWN) | Utility | 65 |

| Genuine Parts (GPC) | Consumer Cyclical | 65 |

| Procter & Gamble (PG) | Consumer Goods | 65 |

| Parker-Hannifin (PH) | Industrial | 65 |

| 3M (MMM) | Industrial | 63 |

| Cincinnati Financial (NASDAQ:CINF) | Financial Services | 61 |

| Johnson & Johnson (JNJ) | Healthcare | 59 |

| Coca-Cola (KO) | Consumer Goods | 59 |

| Lowe's (LOW) | Consumer Cyclical | 59 |

| Lancaster Colony (LANC) | Consumer Goods | 58 |

| Colgate-Palmolive (CL) | Consumer Goods | 58 |

| Nordson (NDSN) | Industrial | 58 |

| Farmers & Merchants Bancorp (OTCQX:FMCB) | Financial Services | 56 |

| Hormel Foods (HRL) | Consumer Goods | 55 |

| California Water Service Corp. (CWT) | Utility | 54 |

| Stanley Black & Decker (SWK) | Industrial | 54 |

| Federal Realty Investment Trust (FRT) | Real Estate | 54 |

| ABM Industries (ABM) | Industrial | 53 |

| Stepan (SCL) | Basic Materials | 53 |

| SJW Group (SJW) | Utility | 53 |

| Commerce Bancshares (CBSH) | Financial Services | 53 |

| Sysco (SYY) | Consumer Goods | 52 |

| H.B. Fuller (FUL) | Basic Materials | 52 |

| Altria Group (MO) | Consumer Goods | 51 |

| Grainger (GWW) | Industrials | 50 |

| Leggett & Platt (LEG) | Consumer Goods | 50 |

| PPG Industries (PPG) | Materials | 50 |

| Target (TGT) | Retail | 50 |

Source: Company Financials, Seeking Alpha.

Above is a table showing stocks that have paid dividends for at least 50 years. These are called "Dividend Kings." As honorable mentions, there are a few companies that are right on the cusp of making the list and almost certainly will do so in 2022. Those are Abbott Laboratories (ABT, AbbVie (ABBV), Becton, Dickinson & Co. (BDX), and PepsiCo (PEP).

I have written about a bunch of these companies, some recently such as ABT and FRT. I also own several of them. Just to be clear, because a company is on this list does not mean it is a "sure thing" or a great investment right now. However, the list is a great place to start looking for value. Young and old investors alike would do well to familiarize themselves with the list of Dividend Kings even if they aren't sending cars into space or regulars on meme boards.

The list of Dividend Kings shows some recurring themes. There are several industrials, consumer goods companies, utilities, and financial service companies. If you're looking for enduring quality, those are good sectors to think about, especially in a shaky market. These companies have been steady through wars, recessions, riots, and stagflation. Even Beanie Babies!

Today's topic is from the above list. It is property & casualty insurer Cincinnati Financial Corporation (CINF). It has paid a higher dividend for 61 straight years. That is longer than many of us have been alive, or longer than many of us wish we have been alive at least. It is one of the lesser-known Dividend Kings, but also one of the best in my estimation.

I have written recently about two other top insurers, Prudential (PRU) and Aflac (AFL). Both are excellent companies and, in my view, good investments. Despite these strong contenders, CINF stands out to me in this turbulent environment. It may not have the highest yield or the flashiest ads, but CINF is a reliable payer and gets the job done. In terms of financial management, it is one of the true elites. I will show you why I think that below.

You won't hear this company's name on the lips of the financial channel hosts, but CINF quietly works its magic behind the scenes without a lot of fuss. If you aren't looking for a stock that will get your pulse racing but instead help you build up that pile over time, you've come to the right place.

Let's begin our analysis, as usual, by looking at the numbers.

CINF's Core Business Remains On Track

CINF has multiple subsidiaries that divide its main insurance business. Groups within CINF include a standard market property casualty insurance group, the Cincinnati Life Insurance Company subsidiary, and the Cincinnati Specialty Underwriters Insurance Company. In addition, CINF owns the CFC Investment Company (leasing and financing services), CSU Producer Resources Inc. (excess and surplus lines brokerage), and MSP Underwriting (acquired in 2019). All of these subsidiaries reflect a common theme of complementing CINF's main insurance business. The company is very focused and does not go off on tangents.

While not one of the very largest insurers, CINF has an $18.9 billion market cap. Its total debt is a paltry $904 million. By comparison, Prudential Financial, Inc. has a market cap of $39.73 billion and a debt of $34.16 billion. So, CINF is big but not the biggest.

As always, I begin with a look at the company's five-year track record.

| CINF | Total Revenues | Net Income | Diluted Earnings/ Share | EBITDA | Net Debt | Shares Outstanding |

|---|---|---|---|---|---|---|

| 2016 | 5,449.0 | 591.0 | $3.55 | 913.0 | 69.0 | 164.5 |

| 2017 | 5,732.0 | 1,045.0 | $6.29 | 838.0 | 194.0 | 164.2 |

| 2018 | 5,407.0 | 287.0 | $1.75 | 367.0 | 82.0 | 163.2 |

| 2019 | 7,924.0 | 1,997.0 | $12.10 | 2,597.0 | 118.0 | 163.2 |

| 2020 | 7,536.0 | 1,216.0 | $7.49 | 1,634.0 | (1.0) | 161.2 |

| TTM | 9,001.0 | 2,525.0 | $15.53 | 3,281.0 | (181.0) | 161.1 |

TTM is Trailing Twelve Months as of September 30, 2021. Total Revenues, Net Income, EBITDA, and Net Debt in $millions. Shares Outstanding in millions. Source: Seeking Alpha.

The important thing when looking over the five-year financials is to get a feel for what the company is all about. CINF's figures tell an interesting story.

First things first. The company clearly has no problem making money. The Net Income, EBITDA, and Diluted Earnings per Share all have advanced greatly over the past five years. What is most interesting is how these columns have outpaced the Total Revenues column - which itself is no slouch, almost doubling since 2016.

Basically, CINF's management is wringing more profit out of its revenue as time goes by. That's the sign of some sharp cookies in the back offices.

Another thing we can see is that CINF's management is incredibly tight with its money. I like that in a company. Not only did management lower the Net Debt over the past five years, they actually reversed it and went net positive - during a pandemic! I haven't seen that with any other company I've looked at.

The final column also is instructive. Unlike other companies that make a big show about share buybacks and lower them in big gulps - then quietly inflate them back up later when they get in trouble or have a need for "general corporate purposes" - CINF quietly goes about its business of slowly whittling down the share count. It does this year after year without any fanfare. And management did this while they were eliminating the debt!

Good financial management at CINF. These folks know their business.

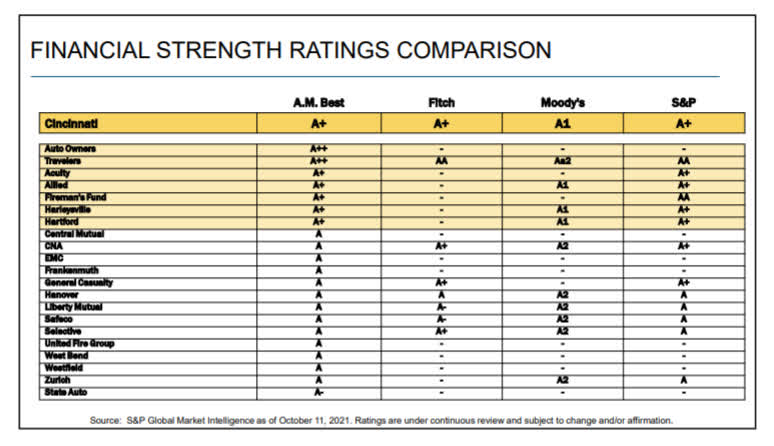

I had a feeling of what to expect from these numbers when I checked CINF's credit rating and I was right. Fitch rates CINF at A+ on 17 November 2021, S&P rated it at single-'A'-plus on 6 November 2021, and AM Best has CINF at "A+."

These ratings compare favorably with others in the industry, which admittedly is a sector with high credit ratings in general.

Cincinnati Financial Corporation's credit scores compared to other industry participants. Source: CINF Investor Handout 11-15-21.

I don't think we have to worry about CINF repaying its debts. Oh wait - it has no net debts. It's in the happy position of a homeowner who has the money to pay off the mortgage but chooses not to because it can get better returns by investing the money. If you're in that position yourself, you know it's a good feeling.

The only conceivable downside I could see to being virtually debt-free is that it signals a lack of opportunities for the company, perhaps being a little too tight with money and passing up other ways to make money. However, all things being equal, I'd rather see a debt-free company than one making a lot of gambles and piling up its debt to take advantage of them. Mergers and acquisitions aren't always positive. Risk-averse, that's probably the best way to describe CINF management.

Let's look a little closer at CINF's performance since the beginning of the pandemic.

| CINF | Total Revenues | Net Income | Diluted EPS | EBITDA | Free Cash Flow per Share | Revenue per Share |

|---|---|---|---|---|---|---|

| Q1 2020 | (99.0) | (1,226.0) | ($7.56) | (1,541.0) | $1.00 | ($0.61) |

| Q2 2020 | 2,714.0 | 909.0 | $5.63 | 1,179.0 | $2.74 | $16.88 |

| Q3 2020 | 2,227.0 | 484.0 | $2.99 | 647.0 | $3.10 | $13.84 |

| Q4 2020 | 2,694.0 | 1,049.0 | $6.47 | 1,349.0 | $2.29 | $16.74 |

| Q1 2021 | 2,227.0 | 620.0 | $3.82 | 804.0 | $2.17 | $13.83 |

| Q2 2021 | 2,295.0 | 703.0 | $4.31 | 908.0 | $3.47 | $14.25 |

| Q3 2021 | 1,785.0 | 153.0 | $0.94 | 220.0 | $3.71 | $11.08 |

Total Revenues, Net Income, and EBITDA in $millions. Source: Seeking Alpha.

Scanning over CINF's quarterly numbers that it had one poor quarter at the very beginning of the pandemic. Everything went negative that quarter and nothing went negative after that.

After that quarter, everything returned to normal. The third quarter saw catastrophe losses higher than expectations. However, on the bright side, other key metrics showed good growth over the year-ago period, including earned premiums, agency renewal written premiums, and net written premiums.

During the third quarter earnings conference call held on 28 October 2021, CEO Steve Johnston addressed the relatively poor that quarter:

Net income for the third quarter of 2021 fell $331 million compared with the third quarter of last year due to $457 million less benefit on an after-tax basis in the fair value of securities held in our equity portfolio.

Insurers have to maintain very up-to-date values on their holdings due to financial regulation. So, CINF had a bad quarter with its investments. Those changes tend to even out over time assuming prudent management.

CINF's cash flow has been strong. As CFO Mike Sewell said during the call:

Cash flow from operating activities for the first 9 months of 2021 generated $1.5 billion, a 36% increase compared with a year ago period.

That's a pretty impressive increase in one year.

The most recent quarter was a little weak, but certainly respectable. If nothing else, the quarterly numbers suggest that CINF made whatever adjustments it had to make in order to handle its pandemic issues.

Next, let's look at the pros and cons of investing in CINF.

Why You Should Consider Investing In CINF

The main reason to invest in Cincinnati Financial Corporation is its long record of rewarding shareholders like you and me.

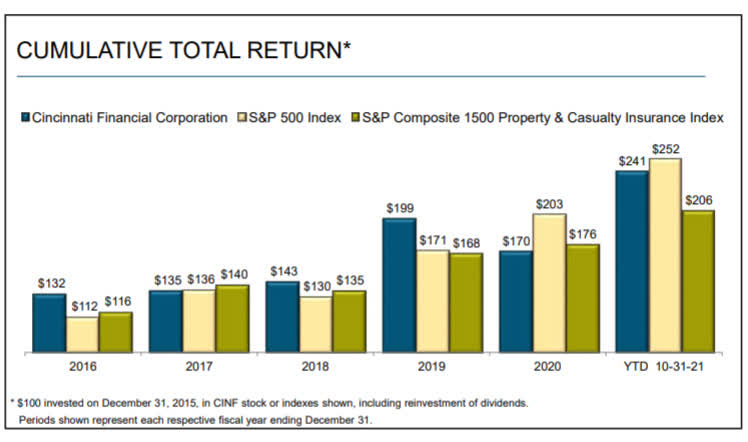

Cincinnati Financial Corporation's total return over the past five years compared to the S&P 500 Index and S&P Composite 1500 Property & Casualty Insurance Index. Source: CINF Investor Handout 11-15-21.

Cincinnati Financial Corporation's total return over the past five years compared to the S&P 500 Index and S&P Composite 1500 Property & Casualty Insurance Index. Source: CINF Investor Handout 11-15-21.

As the above graph shows, CINF has a good record versus the S&P 500 Index in recent years.

Cincinnati Financial Corporation's total return over the past five years compared to the S&P 500 Index and S&P Composite 1500 Property & Casualty Insurance Index. Source: Seeking Alpha.

Cincinnati Financial Corporation's total return over the past five years compared to the S&P 500 Index and S&P Composite 1500 Property & Casualty Insurance Index. Source: Seeking Alpha.

The above chart shows CINF's total return performance versus the S&P 500 Index over the past year. Investors clearly haven't been put off investing in CINF due to the pandemic.

Another reason to consider CINF is its durable dividend. It currently yields 2.15%. That may not seem very impressive, but it looks better when you remember that the S&P 500 Index is yielding a paltry 1.27%.

CINF also has a growing dividend, as mentioned above. However, it's not just raising the dividend by minimal amounts. Its five-year dividend growth rate is 5.56%. That means that the longer you hold the stock, the more your money is working for you.

Cincinnati Financial Corporation's yield on cost over the past decade. Source: Seeking Alpha.

Cincinnati Financial Corporation's yield on cost over the past decade. Source: Seeking Alpha.

As shown in the chart above, your yield on cost would be approaching 10% on your original investment if you had bought CINF a decade ago.

The dividend is amply covered by CINF's cash flow.

Cincinnati Financial Corporation's total return over the past five years compared to the S&P 500 Index and S&P Composite 1500 Property & Casualty Insurance Index. Source: CINF Investor Handout 11-15-21.

Cincinnati Financial Corporation's total return over the past five years compared to the S&P 500 Index and S&P Composite 1500 Property & Casualty Insurance Index. Source: CINF Investor Handout 11-15-21.

The chart above compares CINF's net income and operating income with the ordinary dividends declared. It shows that the dividend is usually covered by a wide margin. The payout ratio is a conservative 42.77%.

Cincinnati Financial Corporation's total return over the past five years compared to the S&P 500 Index and S&P Composite 1500 Property & Casualty Insurance Index. Source: CINF Investor Handout 11-15-21.

Cincinnati Financial Corporation's total return over the past five years compared to the S&P 500 Index and S&P Composite 1500 Property & Casualty Insurance Index. Source: CINF Investor Handout 11-15-21.

As a percentage of net cash flow, CINF's payout ratio has been declining over the past decade. This leaves lots of room for dividend raises and certainly implies that the dividend is safe under current conditions. CINF usually raises its dividend with the March payment, so that's not far away.

As discussed above, CINF is not currently carrying net debt. That means that its Total Debt/Equity (TTM) and Total Debt/Capital (TTM) ratios are both negative numbers. This compares well with industry median averages of 55.02% and 35.62% for those ratios, respectively.

Insurers, of course, are exposed to one extent or another to claims. Thus, it is important that they have a financial cushion to pay those claims. These reserves are a measure of financial health. CINF has been improving its reserves at an accelerating rate over time, always a good and necessary sign.

Cincinnati Financial Corporation's property-casualty reserves. Source: CINF Investor Handout 11-15-21.

Cincinnati Financial Corporation's property-casualty reserves. Source: CINF Investor Handout 11-15-21.

The company has had premium growth that has outpaced the industry. Selling insurance typically requires a lot of face-to-face interactions that were difficult during the height of the pandemic. In my articles about Prudential and Aflac, I showed that those companies experienced issues because of lockdowns. While, as shown below, CINF took a slight hit from 2019 to 2020 in some key metrics most likely due to the pandemic, it continued to beat the industry average and exceed the growth in 2016, 2017, and 2018.

Premiums are the lifeblood of a company like CINF. It's hard for an insurer to grow without strong premium growth. CINF has a good track record in this area.

Cincinnati Financial Corporation's premium growth 2016-2020. Source: CINF Investor Handout 11-15-21.

Cincinnati Financial Corporation's premium growth 2016-2020. Source: CINF Investor Handout 11-15-21.

Premiums are not the only source of income for financial service companies like CINF. Investment income is also extremely important. The trends are in the right direction with CINF. Net investment income was up 7% in the third quarter compared to a year earlier.

Cincinnati Financial Corporation's investment income 2016-2020. Source: CINF Investor Handout 11-15-21.

Cincinnati Financial Corporation's investment income 2016-2020. Source: CINF Investor Handout 11-15-21.

While the third quarter of 2021 was rather mediocre for CINF in some respects, there were more bright spots the deeper you looked under the surface. For instance, CEO Johnston pointed out that key metrics continue to improve:

Our 92.6% third quarter 2021 property casualty combined ratio was 11 percentage points better than last year, with decreased catastrophe losses this year, representing 4.1 points of the improvement. Our current accident year combined ratio before catastrophe loss effects also continued to improve and was 2.5 percentage points better than the first 9 months of 2020.

He further noted that consolidated property casualty net written premiums rose 10%, while net premiums in the personal lines segment rose 7%.

With insurers, you can dive deeper and deeper into the numbers until you get lost like starship Voyager in the Delta Quadrant. Anyone who wants to do that can don the green eyeshades and doesn't need me to help. For everyone else, if you keep it simple and look at the general trends, CINF is in excellent financial health and, despite a stumble in some areas during the third quarter, that health continues to improve.

Cincinnati Financial Corporation's ten-year total return. Source: Seeking Alpha.

Cincinnati Financial Corporation's ten-year total return. Source: Seeking Alpha.

CINF is a stock for the long-term investor who doesn't want to give up performance for the security of investing in a top-rated company. As the chart above shows, CINF's price return over the past decade has more or less matched the S&P 500. In addition to that, you get a growing 2% dividend to live on or reinvest as you choose. As long as you aren't looking for flashy and quick gains, you might want to consider investing in CINF.

Why You Should Be Cautious About CINF

In every article, I explore both sides of the coin. No matter how positive you are about a company, you should appreciate both the bull and the bear case.

As you undoubtedly know, the pandemic is still with us. The new Omicron variant was first identified in South Africa and, as I write this, there is uncertainty about its impact.

Uncertainty creates opportunity. What kind of opportunity depends on how that uncertainty plays out. The Omicron variant won't necessarily "play ball" the way we'd like to think.

What we know so far is that symptoms of the Omicron variant are "extremely mild." Unlike previous variants, this one seems to target adults in the 20-30 age bracket. Why is unclear. Fortunately, this age range tends to be more resistant to disease or at least handle diseases better. Doctors and patients report flu-like symptoms, tiredness, body pains - the usual "ugh, I'm sick" story. Omicron appears to be highly contagious.

The World Health Organization, which has a spotty record in dealing with COVID-19 to date, stated that the global risk from the new variant is "very high." The United States and other nations leaped into action at the first hint of trouble, imposing a travel ban on southern Africa. There is a good chance those bans will expand over time and we'll see more lockdowns. Time will tell.

There are multiple risks to insurers from a renewed pandemic. With governments having been bitten once through a tardy understanding of the virus' deadly nature, now they are showing signs of erring on the side of caution. We may consider that a good thing from a health perspective, which of course is what matters most, but it could negatively impact insurers.

For instance, investment income could suffer. Money could flow toward mitigation efforts and away from the bonds and other assets on which CINF relies. In addition, premium sales could fall for a variety of reasons.

Insurance sales are a highly personal process and face-to-face meetings are essential. Lockdowns and similar preventative measures are not good for the industry. As CINF itself says on its "About" page, "Locally based agents have the relationships in their communities that lead to satisfied, loyal policyholders." Relationships can suffer without personal interactions.

As I wrote in my Prudential article, insurance companies are a unique breed that needs to be valued differently than other businesses. To summarize that discussion, a Columbia Business School article identified several factors that set insurers apart. These include their high leverage ratios and dependence on earning money from the "spread" between return on assets and the cost of liabilities, government regulation that requires insurers to maintain certain capital reserves and impose other limitations, and their careful updating of book value to reflect current market conditions.

So, the impressive financial health of insurers can be misleading. They habitually trade at unusually low price-to-earnings ratios, for instance. That's just how things are and always have been, it's not a sign that they are particularly valuable when the market p/e is around 30.

Inflation is another concern. Since insurers depend on the "spread," this is something that they have to keep a close eye on and make adjustments for constantly. The silver lining is that CINF's management has shown itself to be quite capable of doing this efficiently.

Actuaries are not oblivious to macroeconomic factors. As CEO Johnston said during the call:

Well, I think our actuaries, they look at a variety of methodologies. They use several methods. They look at a lot of different data points. In addition to paid losses, they'll look at case reserves, incurred losses, try to get an estimate for what we're seeing in terms of inflationary factors and set the best estimate that we can every quarter.

He elaborated:

We certainly see the prospects. There's social inflation. There's the inflation of the cost and goods that we use to settle claims for cars, for houses, the supply chain issues, there could be lags in the court system and so forth. We build this all into our models. And as we look at what we see to be loss cost trends, we try to be very prospective and look forward into what we think loss cost will be in the prospective policy period that we will be ensuring and feel comfortable that we're getting rate that is ahead of those loss cost trends in each of our segments.

The critical factor for CINF is that it understands what is happening and, as Johnston said, "stays ahead" of curve. Management would be negligent if it did not do that. I believe history shows that CINF management is not negligent.

Still, there's no guarantee that CINF or any other company can handle virulent inflation any more than governments have shown themselves capable of handling a virulent pandemic. So, this is another uncertainty, and nobody likes to have uncertainties piling up with their investments.

In the broadest sense, inflation is not necessarily bad for stock prices, regardless of how we may feel about it personally when shopping at the grocery store. As noted above, stocks posted good returns in 1979-1980 during peak inflation. CINF kept raising its dividend through those years. Inflation should be manageable as long as management understands what is happening. The long track record established by CINF suggests it knows all about inflation and its effects and knows how to handle it.

Cincinnati Financial Corporation's book value over the past ten years.

Cincinnati Financial Corporation's book value over the past ten years.

As mentioned above, regulators compel insurers like CINF to constantly update their asset/book values. Thus, their book values are a good measure of actual value. CINF's current price to book at best is only about average for the past ten years.

Thus, the best bet is to pick CINF up on a dip should the market stumble some more due to the renewed pandemic. That said, at its current valuation CINF is not pricey, it just isn't the screaming bargain many investors may prefer. There may need to be another market crash toward the lows of 2020 to see that, though, and you might be busy buying other stuff or filling the pantry with scarce toilet paper if that happens.

Another valuation measure that I prefer is to compare a company's yield with its own history.

Cincinnati Financial Corporation's book value over the past ten years. Source: Seeking Alpha.

Cincinnati Financial Corporation's book value over the past ten years. Source: Seeking Alpha.

As you can see in the above chart, CINF's yield currently is hovering around its lows over the past five years. The yield clearly is lower than it has been in the past. This may be a permanent change, and only time will tell, but I doubt it. All else being equal, you like to pick up stocks when they are oversold and thus yielding a little more than usual. That is not the case with CINF right now.

So, there are a lot of uncertainties surrounding CINF, as well as the market as a whole. Everything seems manageable, but it may take some time. If you're looking for the best time to buy CINF, you may want to put it on your watchlist and wait for a market sell-off. I would be enticed by a yield closer to 3% rather than 2%. However, it's not looking too shabby where it is, either.

Conclusion

This is my third article in a row about insurers. It can be hard work learning about these types of companies and winnowing through them to find the real pearls. That is what a successful investor should be willing to do, putting in the time and effort for the ultimate rewards. If you've made it this far through this admittedly dry material, you're one of them. Keep learning, keep thinking, bear down and concentrate on these companies and what makes them tick. It will get you where you want to go.

The insurance sector currently offers a good risk/reward opportunity in an overvalued market. People view a renewed pandemic with apprehension, and rightly so. For some, that initiates caution, for others, it signals possible bargains.

Some individual factors may influence whether you choose CINF over other insurers. Unlike Prudential and Aflac, for instance, CINF does not have a huge presence in Japan. That market with its onerous lockdowns seems to have bedeviled those other two companies over the past year or two. This is one case where having a big geographical footprint may work against a company.

In sum, you aren't going to find many companies with a better long-term track record than Cincinnati Financial Corporation. A Dividend King, CINF has paid down its debt and its core business is growing nicely. This is what many income investors say they want, and CINF delivers. The company's recent ups and downs are related more to transient investment results than issues with selling insurance. The dividend is safe and has been for 61 years. It may not be the most exciting company but Cincinnati Financial Corporation has the reliability and endurance that most income investors should find attractive.